Article Text

Abstract

Background Recent tax increases in Mexico differed in structure and provided an opportunity to better understand tobacco industry pricing strategies, as well as smokers’ responses to any resulting price changes.

Objectives To assess if taxes were passed onto consumers of different cigarette brands, the extent of brand switching and predictors of preference for cheaper national brands.

Methods Using data from three waves of the Mexican administration of the International Tobacco Control Survey, we analysed self-reported brand and price paid at last cigarette purchase. Generalised estimating equations were used to determine predictors of price and preference for national brands.

Results The average price of premium/international brands increased each year from 2008 to 2011; however, the price for discount/national brands increased only from 2010 to 2011. The percentage of smokers who smoked national brands remained stable between 2008 and 2010 but dropped in 2011. Factors related to smoking national brands as opposed to international brands included being male and having relatively older age, lower education, lower income and higher consumption.

Conclusions Tobacco industry pricing strategies in the wake of ad valorem taxes implemented in Mexico prior to 2011 had the impact of segmenting the market into discount national brands and premium international brands. The specific tax increase implemented in 2011 reduced the price gap between these two segments by raising the price of the national brands relative to the international brands. Evidence for trading up was found after the 2011 tax increase. These results provide further evidence for the relevance of tax policy as a tobacco control strategy; in particular, they illustrate the importance of how specific rather than ad valorem taxes can reduce the potential for downward brand switching in the face of decreasing cigarette affordability.

- Taxation

- Price

- Low/Middle Income Country

- Economics

Statistics from Altmetric.com

Background

Increasing the price of cigarettes through taxation reduces prevalence, the level of consumption for those who continue smoking and smoking initiation.1–4 Previous research, however, also suggests that smokers may change their purchasing behaviour to minimise the effect of tax increases by switching to cheaper brands. For example, Tsai et al5 found that 17.4% of Taiwanese male smokers switched to lower-priced brands after a tax increase implemented in 2002. Also, based on information from 20 communities in the USA, Cummings et al6 found that the proportion of smokers who used discount brands increased from 6.2% in 1988 to 23.4% in 1993 as taxes and prices increased over this period. In contrast, a previous study for Mexico did not find evidence of this strategy as switching from international brands to cheaper national brands was as common as the opposite after the 2007 cigarette tax increase.7 Smokers may also switch to cigarettes higher in tar and nicotine as Evan and Farrelly found out using US data for 1979 and 1987.8

The effectiveness of tax increases can also be reduced by tobacco industry pricing strategies, such as absorbing part of these tax increases instead of passing them onto consumers. For example, one recent study shows that the tobacco industry has differently shifted taxes between price segments in the UK; while the price of high-priced brands has increased gradually, the price of low-priced brands has remained fixed between 2006 and 2009, which is associated with a large increase in the market share of the latter.9

Recent excise tax increases in Mexico have included taxes with and without a specific component. Each type of tax may produce a different tobacco industry pricing strategy, which in turn, can impact smokers’ responses to this pricing; however, these topics have been understudied in low-income and middle-income countries. Specific taxes are monetary values per quantity (eg, pesos per cigarette), while ad valorem taxes are set as a percentage of the value of the products (eg, as a percentage of the price to the retailer or as a percentage of the price to the wholesaler). The main advantage of ad valorem taxes is that their real value is preserved as prices increase; the main disadvantages are that they require strong tax administration and are susceptible to undervaluation, which can exacerbate price differentials and brand switching. Specific taxes, on the other hand, entail low administrative requirements and are not subject to undervaluation but need to be periodically adjusted in order to keep their real value from being eroded by inflation.10

The cigarette excise tax (Special Production and Services Tax (SPST)) has been progressively increased in Mexico in recent years, from 110% of the price to the retailer in 2006 to 140% in 2007, 150% in 2008 and 160% in 2009. In addition, a specific component of MX$0.04 (US$0.003) per cigarette was added to the SPST in 2010, which was increased to MX$0.35 (US$0.03) in 2011.11 The STPS (both the ad valorem and specific component), together with the value-added tax (VAT) of 16% of the final price, accounted for 54.2% of the price to the public in 2006, 58.9% in 2007, 60.2% in 2008, 61.4% in 2009, 62.7% in 2010 and 68.8% in 2011.12

Data from Mexico support evidence regarding the effectiveness of cigarette taxes in reducing consumption,7 ,12 ,13 while suggesting that the two tobacco companies (PMI and BAT) that control 98% of the Mexican market have segmented the market into low-cost ‘discount’ cigarettes, mostly comprising national brands, and significantly higher-cost ‘premium’ brands, mostly comprising international brands.7 This process of market segmentation appears to have accompanied the ad valorem taxes that were implemented in the years prior to 2010. The specific tax should narrow the gaps between prices across brand types and thereby impede further segmentation of the market.

The objectives of this study were to assess if (1) cigarette tax increases were passed onto consumers and specially to test for differential effects for national–international brands, (2) the extent of brand switching and (3) predictors of preference for national brands.

Methods

Study sample

Data were analysed from adult smokers who participated in the last three waves (wave 3 (2008), wave 4 (2010) and wave 5 (2011)) of the Mexican administration of the International Tobacco Control (ITC) Survey. The ITC Mexico Survey is a longitudinal survey designed to evaluate the effects of tobacco control policies promoted by the WHO Framework Convention on Tobacco Control (FCTC).14–16 Data collected in six cities at all the three waves were analysed in this study (Guadalajara, Mérida, Mexico City, Monterrey, Puebla and Tijuana). Stratified multistage sampling was used within the urban areas of each city, wherein census tracts and then block groups were selected with probability proportional to the number of households. Households were selected at random and visited up to four times to identify eligible adult smokers (18 years or older, who smoked at least once a week and had smoked at least 100 cigarettes in their lifetime). Up to one woman and one man were interviewed per household.

Sampling weights account for the probability of household selection and are adjusted for the number of smokers within the household; thus, weighted estimates are representative of the population in the urban areas sampled. Data from the last three waves of the ITC Mexico Survey were collected between November and December 2008 (n=1760), January and February 2010 (n=1840) and March and April 2011 (n=1845). Of the 1760 participants interviewed in 2008, 74% (n=1309) were successfully followed up in 2010; of the 1840 participants interviewed in 2010, 83% were followed up in 2011 (n=1519). To maintain sample size across waves, 531 new participants were recruited in 2010 and 326 in 2011 in order to replenish the sample. Replenishment involved the same protocol in randomly selected block groups within the originally selected census tracts that had experienced the greatest loss to follow-up.

The analytic sample for this study consisted of participants in six cities who reported being current smokers at each wave (n=1644 at wave 3, n=1572 at wave 4 and n=1505 at wave 5), including those who were not followed up (n=603 from waves 3–4 and n=393 from waves 4–5) and those who were added to replenish the sample (n=857). Cases with missing values in any of the study variables were excluded from the analyses, so the person-wave observations were 4601 in total.

The ethics review board at the Mexican National Institute of Public Health approved the ITC Mexico Survey protocol, and all participants provided written informed consent before they were interviewed.

Measures

Prices per cigarette at last purchase were calculated using responses to the questions, The last time you bought cigarettes for yourself, did you buy them by the carton, the pack or as single cigarettes, and How much did you pay for that (pack/ single cigarette/carton)? To adjust for different pack sizes, responses to the question When you bought the new pack, how many cigarettes did it contain? were used; if this information was missing or if values below 14 or above 25 were reported,17 it was assumed that packs contained 20 sticks of cigarettes (ie, the most common pack size). Price data from smokers who reported buying cartons were excluded since only few observations were available (n=37). Prices were adjusted for inflation using the general price index from the Bank of Mexico; all price figures are reported in Mexican pesos (MX$) of April 2012. The exchange rate in April 2012 was MX$12.99 per US dollar (US$).

Participants reported the cigarette brands last purchased. We confirmed that data from 2008 (wave 3) were consistent with previously reported 2006 (wave 1) and 2007 (wave 2) data,7 showing that the average price of each of the most popular international brands (Marlboro, Camel, Benson) was higher than the average price of each of the most popular national brands (Montana, Delicados, Boots, Raleigh); therefore, the binary classification of international versus national was used as an equivalent of the premium versus discount classification of brands. Less than 3% (n=8 in 2008, n=12 in 2010 and n=33 in 2011) of the smokers reported having bought contraband brands at their last purchase; these cases were excluded from the brand analysis. Contraband brands were defined as those that were not included in the official list of cigarette brands with a permit to be sold in Mexico in each survey year.18

Standard sociodemographic variables such as age, sex, highest level of education and monthly household income were used as control variables. The seven response options for education were recoded to four (primary school or less, secondary school, high school and graduate or more), as were the seven options for monthly household income (MX$0 to MX$3000, MX$3001 to MX$5000, more than MX$5000 and don't know). The number of surveys to which participants had responded was also included as a control variable in order to adjust for any confounding effects due to prior survey participation.

Analyses

Sample characteristics across waves were compared using simple χ2 tests. Rescaled weights were used to calculate point estimates of average self-reported prices of cigarettes and the proportion of smokers who purchased national brands at last purchase; comparisons of these estimates over time were conducted taking 2010 data as reference and adjusting the p values with Bonferroni's method.19 Additionally, a population-averaged panel model using generalised estimating equations (GEE) was estimated (normal or Gaussian distribution, identity link function, exchangeable correlation structure),20–22 regressing self-reported prices per cigarette at last purchase on type of brand (national or international), format of purchase (pack of cigarettes or single cigarettes), survey wave (dummy coded with 2010 as the reference group) and interactions between time and brand type in order to test whether changes in cigarette prices across waves significantly differed for national brands compared with international brands.

To assess predictors of smoking national/discount brands, a GEE model was also estimated (binomial distribution, logit link function, exchangeable correlation structure), regressing self-reported purchase of national brands at last purchase on sociodemographic covariates and survey wave variables. The distribution of the dependent variables of both GEE models was checked to verify the specifications were adequate.

The statistical software Stata V.11.2 was used for all the analyses.

Results

Sample characteristics

Table 1 shows the characteristics of the sample in each survey wave. Similar demographic characteristics were observed across waves except for education and income level; participants of wave 4 (2010) and wave 5 (2011) were more likely to be less educated and to have a higher household income than participants of wave 3 (2008). Only one-third of the respondents smoked more than five cigarettes per day, and most of them reported buying packs (76%–82%) and international brands (78%–82%) at their last purchase. The percentage of people who purchased singles at last purchase increased over time (17%–23%).

Demographic characteristics and smoking behaviour of sample, ITC Mexico Survey 2008, 2010, 2011 (unweighted means and proportions)

Price changes over time

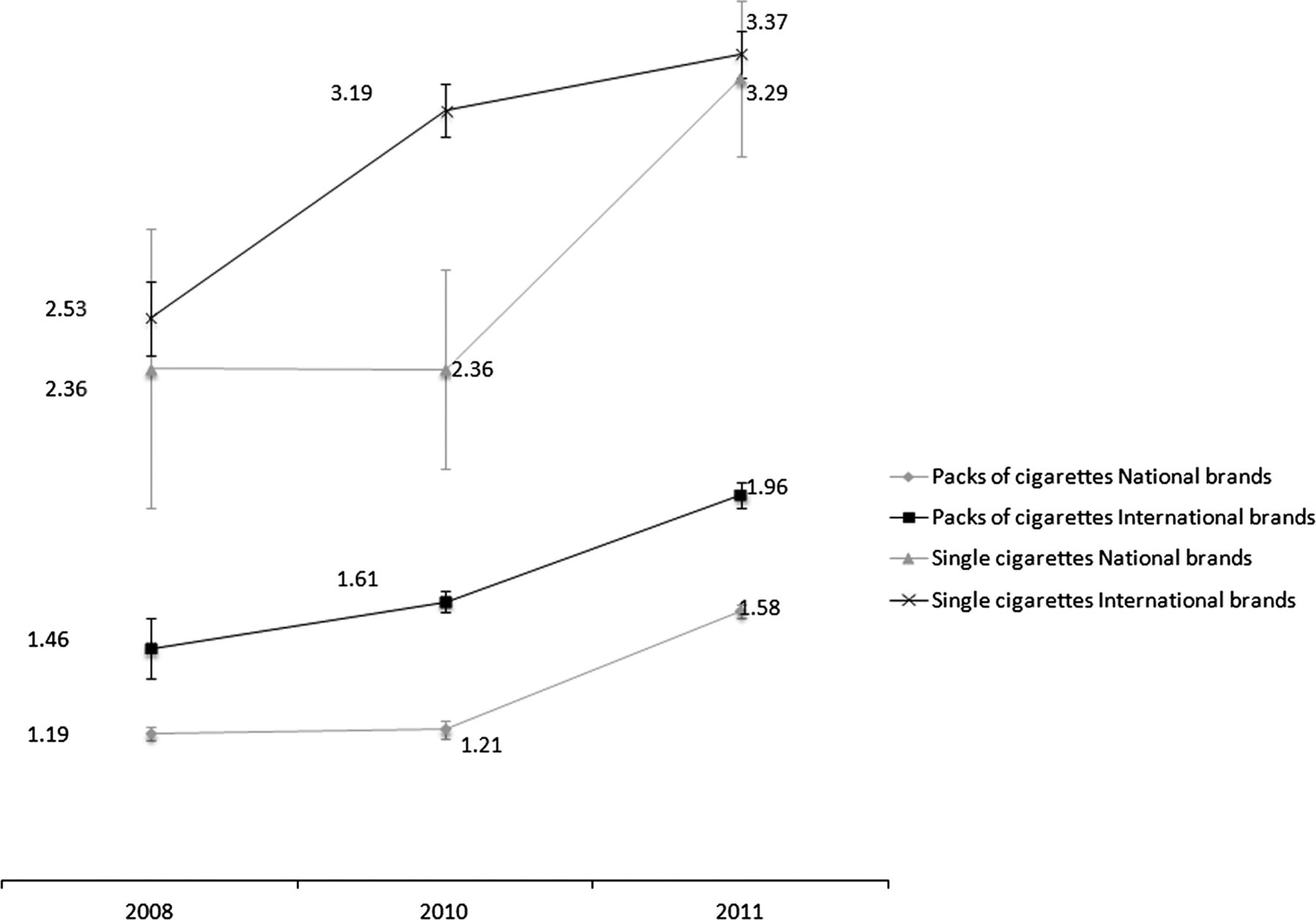

The average price of cigarettes increased from MX$1.60 (95% CI 1.55 to 1.65) per cigarette in 2008 to MX$1.83 (95% CI 1.78 to 1.88) in 2010 and MX$2.19 (95% CI 2.14 to 2.25) in 2011. The average price for international brands increased each year, whether purchased as a pack (MX$1.46 per cigarette in 2008, MX$1.61 in 2010 and MX$1.96 in 2011; p<0.01) or as singles (MX$2.53, MX$3.19 and MX$3.37 per cigarette at each wave; p<0.01) (figure 1). The increase in price for national brands was statistically significant only from 2010 to 2011 (p<0.01 for both packs and singles).

{kind=link}

Self-reported price per cigarette at last purchase, ITC Mexico Survey 2008, 2010 and 2011 (Mexican pesos of April 2012).

Unlike prices of cigarettes sold in packs, prices of single cigarettes of international and national brands were similar in 2008 and in 2011 (MX$2.53 and MX$2.36 in 2008, MX$3.37 and MX$3.29 in 2011, respectively; p>0.01) (figure 1), that is, no price differentials across brands were observed in those years for singles.

The results from the GEE price model are consistent with the results described above (table 2): (1) price was lower in 2008 than in 2010 (B=−0.26, p<0.01) and higher in 2011 than in 2010 (B=0.31, p<0.01)); (2) prices for national brands were lower than prices for international brands (B=−0.48, p<0.01); (3) prices of national brands in 2010 were similar to prices of national brands in 2008 (ie, the coefficient for the interaction between national and 2008 was 0.24, which almost completely offsets the main effect for the overall price difference between 2008 and 2010, B=−0.26, as described above); (4) prices of national brands increased from 2010 to 2011 (the coefficient of the interaction national and 2011 was 0.16; p<0.01); and (5) prices per unit of cigarettes sold in packs were lower than prices of single cigarettes (B=−1.35; p<0.01).

Weighted GEE model for self-reported price per cigarette at last purchase

Predictors of preference for national/discount brands

The percentage of smokers who purchased national brands appeared stable between 2008 (wave 3, 21.7%) and 2010 (wave 4, 22.2%) but dropped in 2011 (wave 5, 19.2%; p<0.05), which likely reflects the impact of the significant specific tax increase that raised the price of national brands relative to the price of international brands in that year.

Among those followed up, the percentage of smokers who switched from international brands to national brands was similar to the percentage of smokers who switched from national brands to international brands (6.2% and 7.7% from 2008 to 2010, respectively, and 4.4% and 6.3% from 2010 to 2011, respectively; p>0.01).

When estimating models to determine factors related to smoking national brands as opposed to international brands, statistically significant correlates included being male and being relatively older, having lower education and lower income, and smoking more heavily (table 3).

Predictors of purchasing national brands, weighted GEE model (dependent variable=1 if brand of last purchase was national)

Discussion

The study provides further evidence of the effectiveness of excise taxes to increase cigarette prices. After cigarette excise taxes were increased in Mexico, prices went up by 14.0% between 2008 and 2010 and by 20.1% in 2011. However, prices did not increase in equal proportions for all brands. In 2008, the relative price of national brands compared with international brands was 0.81 (MX$1.19/MX$1.46) if purchased as a pack or 0.94 (MX$2.36/MX$2.53) if purchased as singles, but decreased to approximately 0.75 (MX$1.21/MX$1.61 for packs, MX$2.36/MX$3.19 for singles) in 2010. Therefore, in response to the low tax increases of 2009 and 2010, the tobacco industry kept prices of cheaper national brands low, while setting higher prices for consumers of relatively higher-priced international brands. It was not until 2011 when the specific tax was significantly increased that the price of national brands was increased by a higher proportion than the price of international brands (between 31.3% and 39.6% vs 21.2% to 5.7%, depending on the form of purchase), which resulted in a relative price of national brands above the 2008 value (0.81=MX$1.58/MX$1.96 for packs, 0.98=MX$3.29/MX$3.37 for singles).

Despite the reduction in the relative price of national brands in 2010, the percentage of smokers who purchased national brands remained stable in that year. This result is consistent with a previous study for Mexico that found no evidence of switching from international brands to national brands after the 2007 tax increase that was also passed onto consumers of international brands to a greater extent.7 The increase in the relative price of national brands in 2011, however, led to trading up to international brands, showing that continuing Mexican cigarette smokers seem to have a preference for international brands. Marlboro dominates the Mexican cigarette market with a market share of nearly 50%.

Little is known about pricing of single cigarettes in Mexico. According to the findings of this study, retailers seem to have followed the pricing strategy of the industry as the prices of single cigarettes and packs exhibited a similar pattern. However, while recent taxes were effective in increasing the price of both, single cigarettes may become more widely available, thereby undermining tobacco control by facilitating youth access and cueing smoking behaviour among adults, including those who are trying to quit.23 ,24 The sale of single cigarettes is prohibited in Mexico since 1999, which is in line with article 16 of the FCTC,14 but compliance and enforcement is poor. For example, in a sample of stores in Mexico City, 58% sold single cigarettes.25 More recent studies carried out in points of sale around schools indicate that sales of single cigarettes are widespread.26 ,27 Data from this study indicate that between 18% and 22% of the smokers purchase single cigarettes (18.2% in 2008 (wave 3), 20.0% in 2010 (wave 4) and 21.9% in 2011 (wave 5)). If the increase in purchase of singles has been accompanied by greater availability of singles, then tobacco taxes should be accompanied by comprehensive enforcement of other tobacco control policies.

As expected, our results indicate that heavier smokers with lower socioeconomic level are more likely to smoke cheaper national brands. Other studies have found similar results. For example, a study for Canada showed that discount brands and native brands were more popular among youth smokers with relatively less spending money and higher cigarette consumption.28 Another study found that the use of discount cigarettes among adults from the USA was associated with lower household income and higher daily consumption.6 In our study, lower education appears more strongly associated with smoking national brands than lower income. Hence, smoking international brands appears to reflect social distinctions and prestige that are above and beyond affordability concerns. These results are important for guiding tobacco control policy oriented towards specific population groups.

Besides national brands, contraband cigarettes constitute an option of cheaper cigarettes for Mexican smokers. According to data used in this study, a low percentage of smokers reported purchasing contraband brands (less than 3%). It was not possible, however, to identify purchases of contraband cigarettes of brands that are legally sold in Mexico (eg, Marlboro or Camel) or other forms of contraband cigarettes such as counterfeit cigarettes. Additional research is required to better understand illicit trade penetration and the characteristics of the smokers who use these types of products.

The study has some limitations. Differences in the sample level of education and income were found across waves. However, the difference for education was not particularly strong, with the biggest difference being between wave 3 (2008) and wave 4 (2010) regarding lower education (26.9% vs 30.8%). On the other hand, the difference for income may reflect increases in income levels over time, mostly moving people from the lowest to the middle category. Decreases in ‘don't know’ responses for income (from 11.9% in wave 3 (2008) to 7.2% in wave 4 (2010) and 6.6% in wave 5 (2011)) may be due to rapport between interviewer and participant, and trust building over time.

Conclusions

Tobacco taxes in Mexico were generally accompanied by price increases; however, the relatively low tax increases in 2009 and 2010 appear to have been passed onto consumers who smoked premium/international brands and not to those who smoked national/discount brands, as had been found for a prior assessment of price changes in response to higher ad valorem taxes implemented in 2007.7 The 2011 specific tax increase appears to have helped disrupt this market segmentation process, resulting in greater price increases for national brands. Evidence for trading up, from national brands to international brands, was found after the large increase in the specific tax in 2011 that narrowed the price gaps.

These results provide further evidence for the importance of tax policy as a tobacco control strategy, including strategies that produce price structures that do not encourage smokers to offset tax increases by switching to cheaper brands. In particular, these results illustrate the importance of using specific taxes rather than ad valorem taxes.

It is necessary, however, to adjust the specific tax for inflation in future to avoid decreases in the tax relative to cigarette price.3 Also, considering cigarette taxes in the context of other tobacco control policies should help governments better tackle the tobacco epidemic.

What this paper adds

-

The results of this study provide further evidence of tobacco industry pricing strategies in response to tax increases and changes in tax structure, as well as smokers’ responses to resulting price changes.

-

The relatively low tax increases implemented in 2009 and 2010 in Mexico resulted in price increases for premium/international brands. The 2011 tax increase, however, which was a specific tax increase instead of ad valorem as had been the case till 2009 and was much higher than the specific tax increase of 2010, resulted in greater increases in prices of national brands versus international brands. This illustrates the relevance of using specific taxes instead of ad valorem taxes.

References

Supplementary materials

Chinese Version

Files in this Data Supplement:

- Chinese version - BMJ Publishing Group Limited takes no responsibility for the accuracy of the translation from the published English original and is not liable for any errors which may occur.

Footnotes

-

Contributors BSdeMJ contributed to the conception and design by proposing research questions and methods to address those questions. She also conducted the data analysis and participated in the drafting. She is responsible for the overall content as guarantor. JFT contributed to the conception and design of the article by proposing research questions and methods. He also participated in the analyses and interpretation of the data, as well as in the drafting. LMRS, MHÁ and FJC participated in the analysis and interpretation of the data. They also revised the article critically. All authors provided approval of the version submitted to Tobacco Control. No one else contributed substantially to the conception, design, analysis, interpretation, drafting and revision of the article.

-

Funding Funding for data collection came from the Mexican Consejo Nacional de Ciencia y Tecnología (Salud-2007-C01-70032), with additional funding for analysis provided by the National Cancer Institute at the National Institutes of Health (P01 CA138389).

-

Competing interests None.

-

Patient consent Obtained.

-

Ethics approval Ethics Review Board at the Mexican National Institute of Public Health.

-

Provenance and peer review Not commissioned; externally peer reviewed.