Article Text

Abstract

Background Increases in tobacco taxes are effective in reducing tobacco consumption, but because of the addictive nature of cigarettes, smokers often seek out less expensive sources of cigarettes. The objective of this study is to estimate the prevalence of cigarette packs that are untaxed by the state in which the participant resides in a sample of US smokers at two time points.

Methods Data for this study were taken from the 2009 and 2010 waves of the International Tobacco Control United States Survey. Members of this nationally representative cohort of smokers were invited to send us an unopened pack of their usual brand of cigarettes.

Results In 2009, 318 packs were received from 401 eligible participants (79%). In 2010, 366 packs were received from 491 eligible participants (75%). In total, 20% of the packs in 2009 and 21% in 2010 were classified as untaxed by the participant's state of residence. The prevalence of untaxed cigarettes was higher in states with higher-excise taxes. Smokers who do not have a plan to quit were significantly more likely to have sent back a pack that was classified as untaxed by the participant's state of residence.

Conclusions One in five packs were untaxed with rates higher in states with higher-excise taxes. It is unclear whether these estimates differ from the actual prevalence of cigarettes that are untaxed by a smoker's state of residence. Harmonisation of excise tax rates across all 50 US states might be one method of reducing or eliminating the incentive to avoid or evade these taxes.

- Taxation

- Economics

- Price

Statistics from Altmetric.com

Introduction

In a recent review of research on the public health benefits of tobacco taxation, Chaloupka et al1 found that increases in taxes on tobacco products are effective in reducing tobacco consumption, especially among the young and the poor. When taxes increase and prices reflect that increase, there are two major behavioural effects. First, smoking prevalence decreases, both because there is an increase in quitting among smokers and because there are fewer non-smokers (almost entirely among youth and young adults) who become smokers. Second, there is a decrease in consumption among those who remain smokers.2–9 Further, the effect of high tobacco taxes on public health is amplified when a portion of the tax revenue is used to fund additional tobacco control and public health programmes.10–12

However, not all of the effects of a tax/price increase on behaviour result in positive health benefits. Some smokers may respond by switching to a less expensive brand or changing the source of cigarettes so as to lower out-of-pocket expenses. That is, smokers may seek to reduce the impact of the tax increase by seeking cheaper sources of cigarettes through a variety of legal and illicit channels.5 ,13–15 Recent studies suggest that the availability of lower-cost cigarettes may blunt the public health impact of high prices and/or taxes on smoking prevalence. Licht and colleagues found that smokers who engaged in price or tax avoidance behaviours were less likely to report cessation, and that over the long term, the use of low and untaxed cigarette sources was associated with low rates of cessation.16 ,17

Measuring the prevalence of various price-minimising strategies can be difficult. While brand switching can be assessed using survey items, more furtive behaviours like purchasing untaxed cigarettes can be harder to measure.

Previous studies have collected discarded cigarette packs in order to estimate the prevalence of untaxed or ‘contraband’ tobacco products. A recent study examining littered packs in the South Bronx area of New York City found that 42% of packs examined did not have any tax stamp and 15.8% had tax stamps from a state other than New York affixed to the packs.18 Another study that relied upon a collection of discarded cigarette packs to estimate the prevalence of foreign tobacco in New Zealand found that 3.2% of packs examined were from outside of the country, which translates to approximately $36 million in lost tax revenue for the New Zealand government.19 However, the relatively narrow geographic areas where the cigarette packs are collected limit the generalisability of such studies. Additionally, estimates based on littered packs can be problematic given that in the USA tax stamps are affixed to the outer cellophane, which can be lost or discarded rather than the actual package. Further, estimates based on discarded packs could be a reflection of commuting and tourism patterns rather than tax avoidance or evasion. Examining unopened packs would avoid this problem, but since these are typically not discarded, they would need to be provided by smokers for examination, the feasibility of which is unknown.

This article reports on a supplementary study conducted during the 2009 and 2010 waves of the International Tobacco Control United States (ITC US) survey. The nationally representative sample of adult smokers in the ITC US cohort were invited to send us an unopened pack of their usual brand of cigarettes, purchased from the outlet where they normally purchase their cigarettes.

The main objective of this study was to estimate the prevalence of cigarette packs that are untaxed by the participant's state of residence in a sample of US smokers at two time points. An additional objective was to examine the characteristics of participants who sent cigarette packs that were untaxed by the participant's state of residence.

Methods

The data sources for this study are the 2009 and 2010 ITC US surveys. The ITC US survey began in 2002 and has been conducted approximately annually, in conjunction with ITC surveys in Canada, UK and Australia. It includes questions to assess smoking behaviour, attempts at cessation and attitudes and beliefs about tobacco products, as well as questions pertaining to each of the demand reduction policies of the WHO Framework Convention on Tobacco Control and a set of important psychosocial mediators and moderators of tobacco use and of cessation. The ITC US survey use random digit dialling to recruit a sample of randomly selected adult (≥18 years) smokers. Cohort members who are lost to follow-up are replaced with newly recruited participants from the same sampling frame to preserve the overall sample size from wave to wave. A primary objective of each ITC survey is to evaluate the psychosocial and behavioural effects of national-level and sub-national tobacco control policies.20

This article reports data from US participants in two versions of the ITC survey. The 2009 survey was conducted between November 2009 and January 2010 of the existing cohort at the previous wave of the ITC US survey (Wave 7, which had been conducted between October 2008 and July 2009). The 2010 survey was conducted between July 2010 and January 2011. Further details of the sampling design used in the ITC survey can be found at http://www.itcproject.org/.

The total eligible sample size for the 2009 survey was 912 participants who at the preceding wave of the ITC US survey (Wave 7) reported being a daily smoker of 10 or more cigarettes per day, reported that they regularly smoked a particular variety of factory-made cigarettes and provided the type of location where they usually purchase their cigarettes. For the 2010 survey, the total eligible sample size was 1144 smokers. Daily smokers who reported in the telephone survey that they smoked five or more cigarettes per day and reported that they smoked factory-made or mostly factory-made cigarettes were eligible for the pack collection component of the study.

The eligibility criteria differed between the two data collections because the first wave of data collection was done as a feasibility study. These criteria were used because we hypothesised that daily smokers of at least 10 cigarettes per day would be more likely to have a pack of cigarettes readily available to send back to us. Given the positive response to the first wave of data collection, we opened the second wave to a wider array of current smokers, using >5 cigarettes per day as the eligibility criteria.

Those who agreed to send in a pack of their usual brand of cigarettes were mailed a data collection kit, which included an information sheet, cover letter, instructions asking them for an unopened pack of their usual brand of cigarettes, a short questionnaire, a plastic zip-top bag for their cigarette pack and a postage-paid return envelope. Participants received US$25 in order to compensate them for their time and effort.

When cigarette packs were received, they were subject to a thorough visual inspection. Characteristics of each pack including brand, descriptive term, length, pack colour and type of tax stamp were recorded. All of the data collection methods were reviewed and approved by the Roswell Park Cancer Institute Institutional Review Board and the University of Waterloo Human Research Ethics Committee.

The behaviours measured in this study are broadly categorised as tax avoidance or tax evasion. Tax avoidance is operationally defined as any form of direct purchase that seeks to reduce the overall cost of cigarettes through legal means such as purchasing from an Indian Reservation, cross-border outlet, duty-free shop or via the internet. Tax evasion is defined as any form of purchase that seeks to avoid paying taxes on a pack of cigarettes by purchasing through illicit means such as street vendors or legitimate outlets that sell packs of cigarettes with the inappropriate or no tax stamp.

Quantifying such behaviour can present challenges, as smokers may be reluctant to report engaging in these behaviours and/or may not be aware that their behaviours constitute tax avoidance or tax evasion at all. The approach to measuring such behaviours reported in this manuscript yields an estimate based on a combination of tax avoidance and tax-evasive behaviours. Because we did not ask participants to send a receipt or otherwise verify the state in which they purchased the cigarettes sent for evaluation, it was not possible to measure the two behaviours separately. Despite this limitation, this approach allows for an objective assessment of cigarette tax status.

Observational data from a visual inspection of the state tax stamp on the cigarette packs were used to determine whether a pack was classified as untaxed or taxed by the participant's state of residence. Taxed packs were defined as packs that carried a tax stamp matching the participant's state of residence. If there was no stamp or the stamp did not match the participant's state of residence, the pack was classified as untaxed. Three states (NC, ND and SC) do not use tax stamps. So, packs received from participants in these states (n=18 packs from participants in the 2009 study; n=18 packs from participants in the 2010 study) were excluded from the analyses (total sample size of 300 packs in 2009 and 348 in 2010). We had no basis for classifying these as untaxed or taxed at the state level based on our operational definition.

Bivariate χ2 test statistics were used to examine the relationship between residence in a high excise tax state compared with a low excise tax state (defined as state excise taxes above or below the federal tax rate of $1.01 per pack), various demographic measures (age, gender, race, income, education and heaviness of smoking index) and purchasing cigarettes that were classified as untaxed by the participant's state of residence. Gamma tests were used to assess the strength of association between packs that were not taxed by the participant's state of residence and the ordinal variables. In addition, self-reported brand and pack Universal Product Code (UPC) obtained during the telephone interview was compared with the brand family and UPC printed on the pack sent for analysis. The UPC is a specific bar code used for tracking merchandise sold to consumers. Each variety of cigarettes is assigned a unique UPC. All analyses were conducted using SPSS 16.0 (Chicago, Illinois, USA).

Results

In 2009, of the 678 smokers who completed the telephone interview, 401 were invited to send in cigarette packs and 318 cigarette packs were received (318/401=79%). In 2010, 1146 smokers completed the telephone survey, 491 were invited to send in cigarette packs and 366 cigarette packs were received (366/491=75%). Combined, we received 686 packs of cigarettes from participants at both collection periods, and of these, 166 (24.0%) came from the same individuals in both the 2009 and 2010 survey waves. Because of the different eligibility criteria between the two surveys, we elected to analyse the data from each survey as two independent cross sections, and in addition performed a cohort analysis among the 166 smokers who participated in both waves.

In 2009, cigarette packs representing 64 different brand varieties were received. A cross tabulation of a usual cigarette brand as self-reported by smokers during the telephone interview and a cigarette brand sent by participants in the cigarette pack collection revealed 97.2% agreement between the participant's self-reported brand as indicated in the telephone survey and the pack received. In 2010, cigarette packs representing 70 different brand varieties were sent by study participants for analysis. Of the 366 packs received, 92.6% matched the brand family self-reported by participants during the telephone interview.

In an additional analysis, the self-reported UPC from the participant's usual brand was compared to assess any differences between the UPC reported during the telephone interview and the UPC recorded from the pack that was sent for analysis. In 2009, 286 participants reported a UPC during the telephone interview. Of these, 59.1% matched the UPC on the pack sent for analysis. In 2010, 67.3% of 303 UPCs reported during the telephone interview matched the UPC on the pack sent for analysis. A more in-depth analysis comparing the UPC as reported during the telephone interview and the UPC as recorded directly from the pack sent by participants indicates that the majority of the mismatched UPCs were a result of the participant's failure to report a prefix or suffix digit. Among the participants who provided a UPC during the 2009 telephone interview, 86.0% either matched directly or were missing a prefix or suffix digit. In 2010, among the participants who provided a UPC during their telephone interview, 82.3% either matched directly or were missing a prefix or suffix digit.

2009 study results

Looking at the 300 packs from states use tax stamps, approximately 6% lacked a tax stamp. Approximately 20% (n=59) of packs did not bear a tax stamp that matched the participant's state of residence. Of these, 24 packs were from a state bordering the participant's state of residence, 19 carried no stamp, 11 carried a tribal stamp and 5 carried some other type of stamp or mark.

Characteristics of participants who sent packs that were untaxed by the participant's state of residence were compared with those who sent packs that carried a tax stamp for the state in which they reside. Relatively few demographic differences were observed. Though not statistically significant, when compared to non-whites, white participants were more likely to have sent a cigarette pack classified as untaxed by the participant's state of residence (5.3% vs 20.8%; p=0.100). Participants with a higher level of education (30.6%) were more likely than those with a moderate level (19.3%) and a low level of education (14.7%) to have sent a pack classified as untaxed by the participant's state of residence (γ=−0.028; p=0.035). No statistically significant differences were observed with respect to age, gender or income. Participants who indicated that they had made a special effort to buy cheaper cigarettes in the 12 months prior to being interviewed were significantly more likely to have sent a pack classified as untaxed by the participant's state of residence than those participants who indicated that they had not made a special effort to buy cheaper cigarettes (31.9% vs 17.4%; γ=0.195; p=0.021). In addition, those with no plans to quit were more likely (29.7% vs 15.0%; γ=0.296; p=0.003) to have sent a pack classified as untaxed by the participant's state of residence than those participants who indicated a plan to quit.

2010 study results

Examining the 348 packs from states using tax stamps, approximately 8% did not bear a tax stamp. Approximately 21% (n=73) of packs did not bear a tax stamp that matched the participant's state of residence and were classified as untaxed by the participant's state of residence. Of these, 25 packs were from a state bordering the participant's state of residence, 27 carried no stamp, 15 carried a tribal stamp and 6 carried some other type of stamp or mark.

Characteristics of participants who sent packs that were untaxed by the participant's state of residence were compared with those who sent packs that carried a tax stamp for the state in which they reside. Relatively few demographic differences were observed. When compared with younger participants (ages 18–39), older participants (ages 40 and older) were significantly more likely to have sent a cigarette pack classified as untaxed by the participant's state of residence (8.7% vs 23.0%; γ=0.516; p=0.016). No statistically significant differences were observed with respect to gender, race, education or income. Participants who indicated that they had made a special effort to buy cheaper cigarettes in the 12 months prior to being interviewed were significantly more likely to have sent a pack classified as untaxed by the participant's state of residence than those participants who indicated that they had not made a special effort to buy cheaper cigarettes (36.8% vs 17.3%; γ=−0.471; p=0.001). In addition, those with no plans to quit were more likely (26.2% vs 17.3%; γ=0.259 p=0.043) to have sent a pack classified as untaxed by the participant's state of residence than those participants who indicated a plan to quit.

State tax rate versus state tax stamp presence

We next examined whether participants residing in higher-tax states were more likely to return packs untaxed by the participant's state of residence. To facilitate analysis, we dichotomised states as to whether the state tax was greater than the federal excise tax ($1.01/pack) or less. In 2009, 28.4% of packs from higher-tax states were untaxed by the participant's state of residence, compared with 12.0% of lower-tax states (p<0.001). In 2010, the corresponding numbers were 31.8% in higher-tax states versus 9.9% in lower-tax states (p<0.001).

2009 and 2010 purchase locations

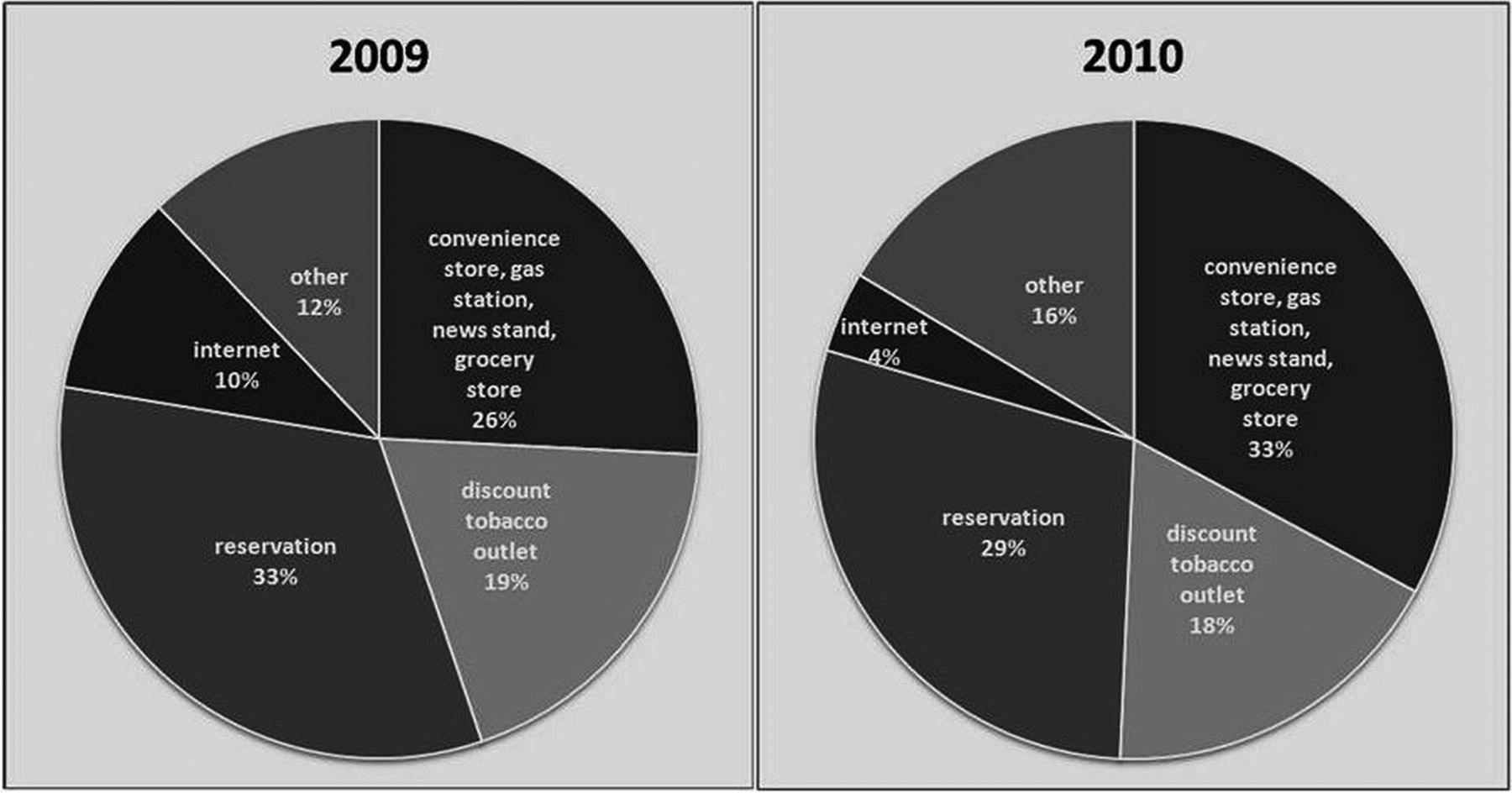

Nearly all of the participants (97.8% in 2009 and 97.5% in 2010) indicated that the pack sent for consideration was purchased from the outlet where they usually purchase their cigarettes. Figure 1 presents the distribution of cigarette packs classified as untaxed by the participant's state of residence by the type of outlet. The sources of the cigarette packs classified as untaxed by the participant's state of residence remained relatively consistent across both data collections.

{kind=link}

Distribution of packs classified as untaxed by the participant's state of residence by outlet type.

Of the 166 participants who sent packs during both the 2009 and 2010 collections, 16.1% sent packs classified as untaxed by the participant's state of residence both times and 7.7% were classified as untaxed by the participant's state of residence during one collection but not the other. The majority (76.1%) of packs sent by participants in both collections were classified as taxed at the state level both times. Most (85.4%) reported purchasing their cigarettes from the same type of outlet at both waves. Of those who reported purchasing their cigarettes from a convenience store, gas station, news stand or grocery store, 91.5% did so at both waves. Similar percentages were observed among those who reported purchasing their cigarettes on an Indian Reservation (84.6%) and those who reported purchasing their cigarettes at a discount tobacco outlet (83.3%).

Discussion

In 2009 and 2010, approximately one in five cigarette packs sent by smokers in this study were classified as untaxed by the participant's state of residence as measured by the presence or absence of a tax stamp from the state in which they reside.

Few consistent patterns were observed with respect to the distribution of non-matching states of residence and tax stamps. Of note, however, is the number of cigarette packs sent by New York State residents that carried no tax stamp or the stamp of a state other than New York (n=14 of 17 packs in 2009; n=11 of 14 packs in 2010). In New York State, tax-free cigarettes can be purchased on Indian Reservations. A 2004 study found that 32% of smokers in New York State purchased cigarettes from an Indian Reservation at least once, while 25% of smokers frequently purchased cigarettes at an Indian Reservation.21 More broadly, those in higher-excise tax states (defined as a state tax higher than the federal rate of $1.01/pack) were significantly more likely to return packs not taxed in the participant's state of residence. This validates the general observation that higher tax rates create incentives to seek out lower prices. An important caveat is that this analysis does not factor in county-level and city-level taxes. For example, states like Illinois have state taxes below the federal rate, but a resident of Chicago would additionally be liable for Cook County and City of Chicago taxes, which would bring the total tax due higher than the federal rate.

Of the stamps classified as untaxed by the participant's state of residence, approximately one-third (32.2% in 2009 and 36.9% in 2010) did not have any tax stamp affixed to the outside of the pack. This suggests the need for all states to use tax stamps to indicate that state tax has been paid on each pack of cigarettes sold within each state. This would allow for a more complete estimate of the prevalence of tax avoidance and/or evasion. However, the presence of tax stamps on all packs cannot reduce rates of tax evasion and avoidance as long as there continues to be disparities in tax rates between states. For example, New York State currently levies the highest excise tax rate on cigarettes at $4.35 per pack, while Virginia's cigarette excise tax, at $0.30 per pack, is the lowest.22 Perhaps requiring all tax collections and tax stamps to be applied at the point of manufacture (ie, federal, state and local) would eliminate opportunities for tax evasion. Adopting policies geared towards limiting price differentials across jurisdictions might be another method of disincentivising smokers to avoid or evade taxes in their state of residence.

Few demographic differences were observed between participants who sent a pack that was classified as state tax paid and those who sent a pack that was untaxed by the participant's state of residence. Those with a higher education level were more likely to have sent a pack bearing a tax stamp that did not match their state of residence relative to those with lower levels of education in 2009. Those aged 40 and older were more likely to have sent a pack bearing the stamp of a state other than their state of residence relative to those aged 18–39 years in 2010. At both waves, smokers who reported that they made a special effort to purchase less expensive cigarettes and those who do not have a plan to quit smoking were significantly more likely to have sent a pack that was classified as untaxed by the participant's state of residence. This suggests that some smokers (with means to do so) could be seeking out lower-cost products in response to higher prices rather than quitting smoking.

The analysis examining the relationship between a self-reported brand and UPC information and the brand family and UPC printed on the pack sent for analysis was done in order to address concerns over whether a participant might report smoking a more expensive brand and send us a less expensive brand, but yielded some interesting results.

The high rate of agreement between the usual brand reported at the time of the telephone interview and the brand family of the pack sent for analysis suggests that the majority of participants did indeed send the variety that they usually smoke. However, the low rate of agreement between the self-reported UPC and the UPC printed on the pack might suggest otherwise. The reasons for this discrepancy are unclear. It is possible that some participants were inaccurate in their self-report of the UPC or smokers in this study might have switched to a different variety within the same brand family during the time between the telephone interview and when they sent the pack for analysis. A third possibility is that the participant deliberately deceived us by sending a pack different from their self-reported variety and/or purchased from a different location.

A strength of this study is that the prevalence estimates are based on cigarette packs sent from a sample of US smokers participating in a nationally representative survey at two different time points. The prevalence estimates appear steady across two surveys. The majority of the participants who initially agreed to take part in the pack collections sent a pack for analysis. These high rates of participation and replication of findings suggest that this type of data collection is feasible and relatively cost-effective given the $25 compensation for time and effort.

Conceptually, obtaining this estimate directly from unopened cigarette packs sent by smokers should be a more accurate method than other previously attempted approaches using tax stamps on discarded packs to measure tax avoidance and/or tax evasion. However, the study has several significant limitations that could be refined for use in future data collections of this type. First, the sample size was small and there were differences in the distribution of cigarette packs collected in each state. We received no packs from smokers in Alaska, Delaware, Hawaii, Idaho, Maine, Rhode Island, South Dakota and Vermont in 2009 and no packs from Hawaii, Rhode Island and Vermont in 2010. Because of this, the ability to generalise these results as representative of the population of smokers at large is limited.

Additional limitations related to the sampling strategy employed here may also lead to inaccurate prevalence estimates. It could also be argued that the study eligibility criteria could create a significant bias, as individuals who are smoking 10 or more cigarettes per day may have a greater incentive to seek out less costly cigarettes. Previous studies have shown that individuals who have higher daily cigarette consumption are more likely to engage in tax avoidance behaviours.7 ,8 ,16 However, both the populations under consideration and the estimates of tax avoidance and/or evasion were similar at two time points using more restrictive and less restrictive eligibility criteria. Further, smokers who are knowingly avoiding taxes by purchasing cigarettes from unlicensed tobacco outlets might be less likely to answer a survey or send a cigarette pack for inspection. The prevalence of packs that did not show evidence of tax avoidance or evasion was higher among those who sent a pack during both data collections when compared with the overall sample averages in both 2009 and 2010, lending some support to this hypothesis. Future data collections of this type might consider refining the study methods to be more inclusive of individuals who smoke fewer than 10 cigarettes per day and those who consciously evade cigarette taxes to better reflect the overall population of smokers.

Previously published literature has suggested links between a combination of high tobacco prices and the convenient availability of lower-cost alternatives.8 ,16 Another study published in 2010 used data from a random sample of littered cigarette packs in the city of Chicago to estimate tax avoidance. Nearly three quarters of the packs collected did not contain a local tax stamp. Further, as the distance between the collection site and the border of the state of Indiana increased, the probability of the pack bearing a local tax stamp also increased.23 In this study, we were unable to measure the distance between a participant's residence and the tobacco outlet from which the cigarette pack sent for inspection was purchased. Because of this, we were unable to measure proximity and access to lower-priced sources as factors. Future research might consider methods of obtaining information related to the purchase location in order to better evaluate the association between tax avoidance and/or evasion and the ease of obtaining cigarettes at a lower cost.

The prevalence estimates of tax avoidance and/or tax evasion at the state level were taken from packs of cigarettes sent by a sample of US smokers, participating in a nationally representative survey. What is unclear is whether these estimates are lower than the actual prevalence of sales of cigarettes that are untaxed by a smoker's state of residence. The use of state tax stamps by all 50 US states could be a step towards a more accurate prevalence estimate. In terms of policy, harmonising tax rates across all US states could be a step towards reducing or eliminating incentives to seek out lower-cost cigarettes. Future research should consider a focus on how the proximity to lower-tax or lower-cost sources of cigarettes influences tax avoidance and/or evasion.

What this paper adds

-

The paper provides a prevalence estimate of tax avoidance and/or tax evasion obtained from packs of cigarettes sent by a sample of US smokers participating in a nationally representative survey.

-

Using a pack collection method we found that one in five packs were untaxed with rates higher in states with higher-excise taxes. What is unclear is whether these estimates differ from the actual prevalence of sales of cigarettes that are untaxed by the participant's state of residence. In terms of policy, harmonisation of excise tax rates across all 50 US states might be one method of reducing or eliminating the incentive to avoid or evade these taxes.

References

Supplementary materials

Chinese Version

Files in this Data Supplement:

- Chinese version - BMJ Publishing Group Limited takes no responsibility for the accuracy of the translation from the published English original and is not liable for any errors which may occur.

Footnotes

-

Contributors RJO, GTF, KMC, AH: conception and survey design. BVF: data analysis. BVF, RJO, FJC, GTF, KMC, AH, ASL: drafting the manuscript and revising it critically for important intellectual content. All authors read and approved the final manuscript.

-

Funding This research was funded by grants from the National Cancer Institute of the United States (R01 CA 100362, P50 CA111236 (Roswell Park Transdisciplinary Tobacco Use Research Center), P01 CA138389, and R25 CA113951), Canadian Institutes of Health Research (79551 and 115016). Geoffrey T Fong was supported by a Senior Investigator Award from the Ontario Institute for Cancer Research (OICR) and a Prevention Scientist Award from the Canadian Cancer Society Research Institute.

-

Competing interests KMC has served in the past and continues to serve as a paid expert witness for plaintiffs in litigation against the tobacco industry.

-

Patient consent Obtained.

-

Ethics approval All of the data collection methods were reviewed and approved by the Roswell Park Cancer Institute Institutional Review Board and the University of Waterloo Human Research Ethics Committee.

-

Provenance and peer review Not commissioned; externally peer reviewed.

-

Data sharing statement In order for research teams outside the ITC Project to gain access to any of the data, the successful completion and approval of an ITC Data Usage Application is required. Both ITC principal investigators and research teams outside the ITC Project who have received approval to use the data are required to sign an ITC Data Usage Agreement. More information is available at http://www.itcproject.org.