Article Text

Statistics from Altmetric.com

The European Union (EU) can serve as an example of a successful regional cigarette tax harmonisation and integration regime. This level of integration was motivated by an effort to ensure the proper functioning of the EU internal market, which required a reduction in inter-country variation in tobacco product prices.

Yet, despite the effort to harmonise, the variation in cigarette taxes and prices between the EU member states is greater than, for example, that across states in the USA. The USA is a large internal market, but has little tobacco tax harmonisation and integration. The coefficient of variation (CV) for cigarette prices in the USA is 0.20 versus 0.44 in the EU, in 2010.1 This is likely due to US states being much more homogenous than the EU member states, particularly with respect to incomes. These differences may drive the price strategies of the tobacco industry, which have implications for the affordability of tobacco products.

EU directives on cigarette taxation have two important features:

-

a minimum excise tax burden (percentage share of tax in price)

-

an excise tax floor, measured in Euros per 1000 cigarettes sold.

These two components create different binding constraints for two groups of countries: the EU-15 (Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, The Netherlands, Portugal, Spain, Sweden and the UK) and the EU-12 (Bulgaria, Czech Republic, Cyprus, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Romania, Slovakia and Slovenia). EU-15 countries are all developed, high-income countries, many of which were founding members of the EU. Generally speaking, the countries in this group have higher per capita incomes (which are growing at a slower pace) and higher cigarette taxes and prices. The EU-12 includes both high-income and low- and middle-income countries that joined the EU in 2004 or 2007, some of which have enjoyed rapid economic growth after the EU accession. Even though there is a lot of economic variation and dynamism in the EU, integrated multi-prong tax policy has been successful in increasing the real price and decreasing the affordability of cigarettes in many member states.2

The EU Directives (in effect as of 1 July 2006) specify that member states must meet a minimum excise tax burden of 57% of the most popular price category with an exemption for countries where the total value of the excise tax exceeds €101 per 1000 cigarettes. Additionally, all EU-12 countries (except Cyprus and Malta) were granted derogations to postpone the application of the minimum excise duties until 31 December 2009.3 Countries must also use a mixed tax system applying both ad valorem and specific excise taxes. From 1 January 2011, the price benchmark has been changed from the most popular price category to the weighted average price.

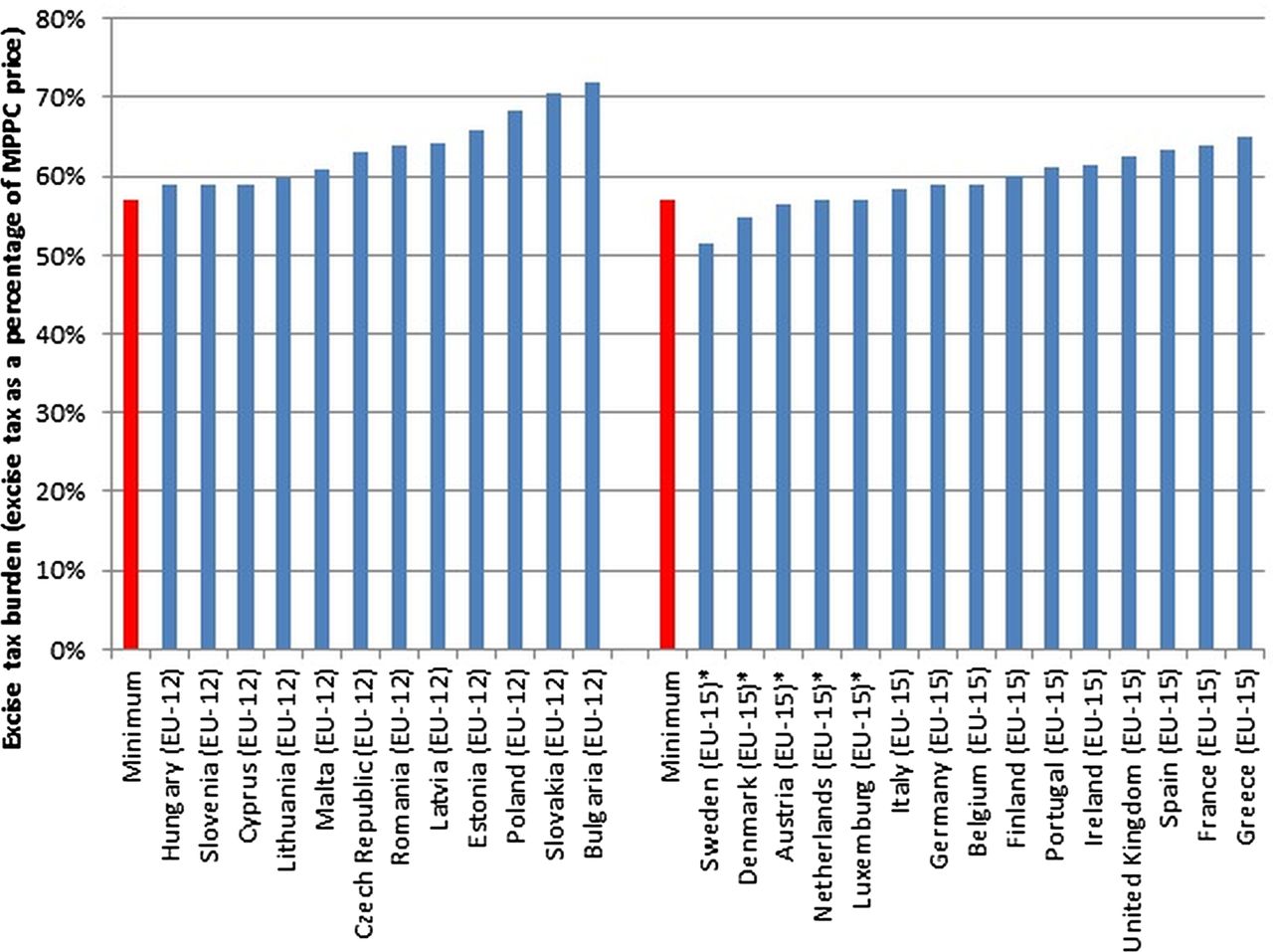

As of 2010, all EU-12 countries easily met the minimum tax burden requirement, with the actual excise tax burden ranging from 59% to 72% (mean 64%, CV 0.07). In the same year, the excise tax burden ranged from 52% to 65% (mean 59%, CV 0.06) in the EU-15 countries. Five EU-15 countries invoked the exemption from the EU Directives since their excise tax exceeded €101 per 1000 cigarettes (figure 1).

Excise tax burden in EU-15 and EU-12 member states, 2010. Note: *indicates countries that invoked the exemption from the EU Directives since their excise tax exceeded €101 per 1000 cigarettes. EU, European Union; MPPC, most popular price category.

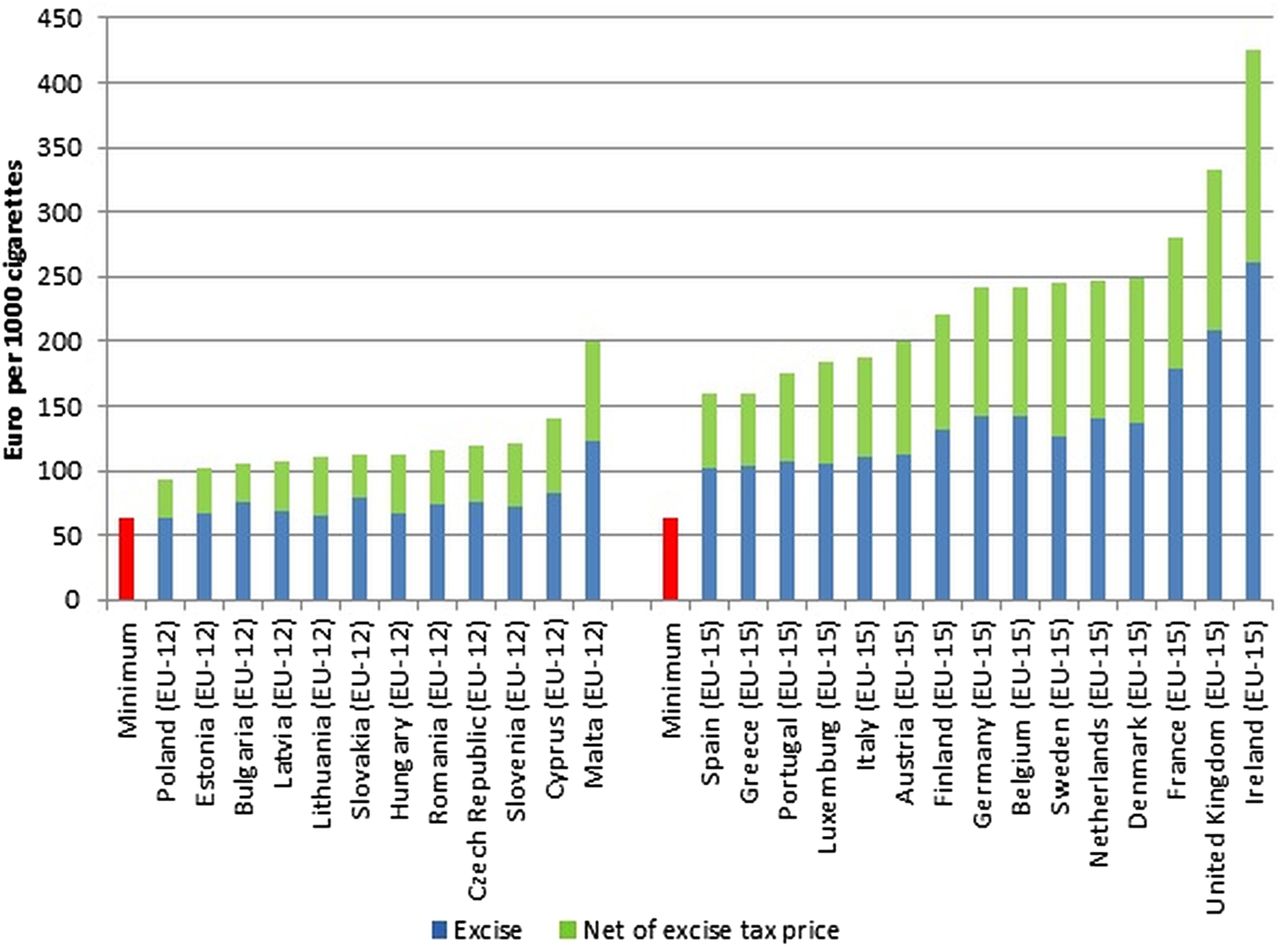

The second feature of the EU tobacco tax system, the excise tax floor of €64 per 1000 cigarettes, is analysed in figure 2. EU-15 states meet the excise tax floor easily with the value of excise tax per 1000 cigarettes ranging from €101.40 to €260.98 (mean 140.57, CV 0.32). On the other hand, EU-12 states struggle with this requirement: their excise tax per 1000 cigarettes ranges from €64.00 to €122.00 (mean 76.18, CV 0.21). The two rules create different binding constraints on the two groups of countries, with the EU-15 states focusing on the excise tax burden rule (or the higher excise tax floor), because they easily meet the tax floor due to higher cigarette prices. EU-12 states struggle to meet the excise tax floor, but have little difficulty meeting the excise tax burden due to lower prices. While a lot of positive attention has focused on the excise tax burden rule, it is only relevant for EU-15 countries. The most effective mechanism for reducing the price differential between EU-12 and EU-15 states is not the excise tax burden rule, but rather the excise tax floor.

{kind=link}

{kind=link}

Excise tax and most popular price category price per 1000 cigarettes in European Union (EU) member states, 2010.

In 2010, the EU strengthened the tax requirements for member states, raising the excise tax burden to 60% and raising the excise tax floor by 41% to €90 per 1000 cigarettes. The 60% tax burden will not apply to countries whose excise tax exceeds €115 per 1000 cigarettes. While implementation of the new tax regime began immediately, countries have until 1 January 2014 (or 1 January 2018 for Bulgaria, Estonia, Greece, Latvia, Lithuania, Hungary, Poland and Lithuania) to comply with the new policy.4 Nine of the EU-12 states have already met the higher excise tax burden (and the remaining three are within 1 percentage point of the target), while all EU-15 states have already met the future excise tax floor. Both groups of countries will need to make adjustments to comply with the new directives. However, the impact will be more dramatic in EU-12 countries (due to the 41% increase in the excise tax floor). This will reduce price differentials within the EU thereby reducing incentives for tax avoidance and evasion, and reduce cigarette affordability, particularly in EU-12 member states where affordability has been sustained or increased by the economic growth and/or tobacco industry price strategy.2

The harmonised tax regime also applies to other tobacco products: cigars/cigarillos, fine-cut tobacco intended for roll-your-own (RYO) cigarettes and other smoking tobaccos. Each group is subject to separate excise tax burden and excise tax floor requirements. However, unlike cigarettes which have to meet both the excise tax burden and floor, it is sufficient for the non-cigarette products to meet either of the two standards.

RYO tobacco is important since it is generally a cheaper substitute for cigarettes. As of 2010 the EU minimum excise tax burden on RYO tobacco was 36% of the retail price and the excise tax floor was €32 per kilogram. In 2010, the average excise tax burden was 52% and 43% in EU-15 and EU-12 states (CV 0.16 and 0.43), respectively, and the average value of excise tax per kilogram was €85 and €47 in EU-15 and EU-12 states, respectively (CV 0.60 and 0.37).5 Countries should meet either of the requirements by 2020; however, 12 EU-15 and five EU-12 countries already meet the requirement. The required excise tax burden and floor are lower on RYO tobacco than cigarettes and result in greater variation in RYO tobacco taxes than in cigarettes.

The EU provides an important blueprint for tax harmonisation and integration in other regions. It shows that in diverse regions one may simply not be able to harmonise taxes on one measure (ie, tax burden) but may require a number of interconnected measures to reduce variation in cigarette prices. Additionally, recent steps taken by the EU will result in reduced variation in prices.

What this paper adds

-

While many tobacco control advocates credit the European Union's (EU's) minimum excise tax burden (percentage share of tax in price) for increasing cigarette taxes and prices, we show that the EU excise tax policy has been effective because it is more nuanced with an excise tax floor that acts as a binding constraint on member states with lower prices. Additionally, we show that recent reforms will likely have a greater impact on taxes in the newer EU member states than older member states.

Acknowledgments

We would like to acknowledge Alex Liber and Deborah Abrams for assistance with the preparation of the data.

Footnotes

-

Contributors All authors contributed to the entire manuscript.

-

Competing interests None.

-

Provenance and peer review Not commissioned; externally peer reviewed.