Article Text

Abstract

Background Previous research has outlined transnational tobacco company (TTC) efforts to undermine implementation of the Protocol to Eliminate Illicit Trade in Tobacco Products (Protocol) and evidence of ongoing TTC complicity in the illicit tobacco trade (ITT). However, the industry’s views on the Protocol and role in its development are not well understood.

Methods Systematic searching and analysis of leaked documents—approximately 15 000 from British American Tobacco (BAT) and 35 from Philip Morris International, triangulated via searches of online resources and interviews with five stakeholders across academia, international organisations, governments, civil society and the private sector.

Findings Evidence indicates that after privately viewing the Protocol as a significant threat (2003), BAT worked to influence its content, while publicly signalling support for it (2007–2012), and was largely satisfied with the final text. BAT successfully pushed for a non-prescriptive text which enabled further country-level TTC influence during the Protocol’s implementation phase. The final text also reflected other BAT policy preferences, including preventing outright bans on duty-free sales and intermingling, and making it difficult to sanction and hold tobacco companies accountable for ongoing involvement in the ITT. TTC representatives were present during early Protocol negotiations, despite rules against this, and BAT obtained draft texts before they were public and paid at least one delegate to support its position.

Conclusions BAT’s primary interest in shaping the Protocol was to minimise its financial and legal costs for BAT while maximising potential costs to small competitors. These findings raise concern about the Protocol’s ability to control the ITT, particularly given TTCs’ intention to influence ongoing national implementation. An effective Protocol is vital to controlling both the ITT and ongoing tobacco industry involvement in it and, in turn, governments’ ability to increase tobacco taxes and thereby save lives.

- illegal tobacco products

- tobacco industry documents

- public policy

Data availability statement

The BAT documents analysed in this paper are available at: https://industrydocuments.ucsf.edu/.

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

Introduction

The Protocol to Eliminate Illicit Trade in Tobacco Products (Protocol) was developed under the Framework Convention on Tobacco Control (FCTC) as a coordinated international response to the illicit tobacco trade (ITT). In the 1990s, wide-ranging investigations from media, academic, law enforcement and judicial organisations uncovered overwhelming evidence of transnational tobacco company (TTC) involvement in the ITT, dating back to the 1960s.1–14 This led to guilty verdicts in legal action and agreements between the TTCs and a range of national governments and international organisations as they tackled the ITT.15

The Protocol outlines steps Parties should take to tackle the ITT: these include requirements to establish tracking and tracing (T&T) systems for tobacco products in their own jurisdictions which then combine to form a global T&T regime, which aims to control the tobacco product supply chain.16 17

The Protocol’s policy process began at the first Conference of the Parties (CoP) to the FCTC in 2006 where Parties decided to convene an expert group to prepare a template for a protocol (see table 1 for timeline).18

Protocol and Codentify/Inexto timeline

At the second CoP, in 2007, Parties agreed to establish an Intergovernmental Negotiating Body (INB), open to all FCTC Parties, to draft and negotiate the Protocol. The illicit trade protocol (ITP) was adopted at the fifth CoP in 2012 and entered into force in September 2018 (see table 1).

Previous research shows that after their complicity in the ITT being exposed, and while the Protocol was being developed, the TTCs created their own track and trace (T&T) system and established third parties to promote it (see table 1 for timeline).15 19 20 Simultaneously they purportedly made extensive efforts to ingratiate themselves with authorities tasked with addressing the ITT, funding organisations, conferences, training and research to create a supportive policy environment and to be perceived as a solution to the ITT, rather than the key driver of the problem.15 Evidence also indicates that the majority of product on the ITT continues to originate from TTC supply chains and that the major TTCs may in fact also be responsible for some illicit white products.21–23

However, the industry’s views on the Protocol and role in its negotiation and development have not yet been examined. By analysing previously unreleased leaked internal documents, this paper investigated how British American Tobacco (BAT) attempted to mould the text of the Protocol and to what extent the company was successful in doing so.

This work is the first to examine a TTC’s role in shaping the Protocol and thus provides a unique contribution to the literature. Taxation is the most effective way to reduce smoking prevalence and makes important contributions to national economies, especially in low to middle-income countries (LMIC). Yet governments, particularly in LMICs, are often concerned that increasing taxes would lead to more ITT, an argument widely promoted by the tobacco industry (TI) despite independent literature suggesting otherwise.24 As such, an effective Protocol and T&T system are vital to controlling both the ITT and ongoing TI involvement and, in turn, governments’ ability to increase tobacco taxes and thereby save lives.

Methodology

Searching of TI documents

The authors primarily relied on three sets of internal TI documents:

To understand BAT’s role in shaping the Protocol, the authors (between July and October 2019) searched a set of approximately 15 000 internal BAT documents leaked by Paul Hopkins, a former BAT employee who worked on ITT issues in several parts of Africa and the Middle East for 15 years (2000–2014).25 These include emails, presentations, memos, spreadsheets and other documents Hopkins received or sent during his time working for BAT. These documents are not currently publicly available but the authors are in the process of making them so.

Using a secure document review platform, snowballing based on results from initial search terms led to a total of 26 search terms being used (online supplemental appendix I). Nine hundred and ninety-nine documents were identified, read and reviewed, and 911 were deemed relevant, that is, made reference to either the Protocol directly or international efforts to tackle the ITT. Following the exclusion of duplicates, 140 documents were coded (spanning from 2003 to 2016) using 18 themes, agreed between all authors after preliminary analysis of a small subset of documents (see online supplemental appendix II).

Supplemental material

A second set of three internal BAT documents were read and reviewed in full. They provided important information on the company’s Protocol strategy.

To compare and contrast BAT’s views with those of Philip Morris International (PMI), the authors read and reviewed a third set of 35 internal PMI documents released by Reuters as part of the ‘Philip Morris Files’ investigation26; four of which were deemed relevant and analysed.

Analysis

Qualitative thematic analysis, based on a hermeneutic approach to company document analysis, was applied to all of the document sets with analysis focusing specifically on TI views on the Protocol and company strategies and tactics to influence it.27 28

Triangulation

Data triangulation was a three-step process: first, in order to explore the context at the time, company documents were shared and to properly interpret them, the authors searched online news media, academic literature, non-governmental organisation (NGO) reports, publications from national governments and international organisations (eg, WHO), the Truth Tobacco Industry Documents (online supplemental appendix I), as well as TI websites and other public documents.

Second, we conducted interviews with five stakeholders across academia, international organisations, governments, civil society and the private sector (with no reported financial links to the TI), which provided valuable background information and further contextualisation. Authors selected interviewees based on their experience with the Protocol and its negotiation. Interviewees were provided in advance with a participant information sheet, outlining potential risks of taking part, a standardised questionnaire and a consent form including anonymity options.

Third, we further triangulated findings by reviewing of a range of policy documents including summary records from Protocol negotiations, technical reports, documents from relevant working groups, and other official and NGO documentation on the process leading up to the adoption of the Protocol.

Results

From hostility to public support and lobbying

TTCs initially viewed with concern the developing idea of international regulatory measures against ITT. The year the FCTC was adopted—2003—an internal BAT presentation highlighted concerns about both the ‘reputational’ and ‘regulatory threat’ the company faced following revelations of TTC involvement in the ITT,1–14 stressing that it was ‘VITAL for Big Tobacco to be involved in shaping final regulation’ on the ITT.

By the time Protocol negotiations began in 2008, the TTCs had already begun to rebrand themselves as part of the solution, rather than perpetrators of the ITT.29 30 In 2007, BAT started to frame the concept of a Protocol as a potential opportunity, stating publicly that it ‘strongly supports the need for [it]’ and ‘look forward to partnering with governments in the development, negotiation and implementation of an effective (…) protocol’.31 In response, the Framework Convention Alliance (a civil society alliance which aims to strengthen the FCTC and support its implementation) wrote: ‘As it has recently become clear to BAT that it is unlikely to succeed in preventing the development of a protocol on illicit trade, [BAT] now wants to maximize its chances of influencing the content of the protocol.’32

Attempts to influence the protocol

Initially, despite FCTC Rules of Procedures, Article 5.3, and its guidelines to guard against industry interference, multiple TTC representatives attended the third Protocol negotiation (INB3) (June to July 2009—table 1).33 34 The NGO observer, Corporate Accountability (CA—then called Corporate Accountability International), found that 23 of 28 people willing to identify themselves to CA in the public gallery overlooking the main floor of the convention hall were from the TI, including 12 from BAT.33 This was part of a larger number of ‘Activities to Manage Risks—WHO Protocol’, described in a BAT internal strategy document shortly before INB3 (Figure 1).35 Delegates then decided to exclude the general public (with the exception of NGOs) mid-way through INB3.33

Future Activities to Manage Risks—WHO Protocol. Source: BAT, April 2009.35 AIT, Anti-Illicit Trade, BAT, British American Tobacco; INB, Intergovernmental Negotiating Body; NGOs, non-governmental organisations; T&T, tracking and tracing; REG Regulatory Engagement Group, WTO, World Trade Organization.

This did little to dissuade TTCs from interfering, however. As documented at the time by CA, tactics deployed went beyond attending INB proceedings and included ‘developing close ties with governments, securing representation on government delegations to the negotiations, and using duty-free trade associations to lobby against key provisions’.33

Internal BAT documents show the company had a clear advocacy strategy to influence the Protocol text36 and collaborated on this with other TTCs.37

The documents do not detail exact outcomes from such efforts. However, it is clear that BAT was able to obtain draft texts before they were made public38 and paid at least one government representative to support the company during the negotiations.25 39–41

BAT’s broad aims for the Protocol

Documents suggest BAT had three broad aims for the Protocol, namely that it should not be too prescriptive and allow for flexibility at the national level, should target competition—in particular from smaller tobacco companies, and should lead to a T&T system with limited impact on the company’s productivity and efficiency.

Not too prescriptive a text

A core component of BAT’s engagement strategy on the Protocol was to ensure that the final text would not be too prescriptive, instead allowing countries to interpret recommendations, thus enabling them to shape implementation at the national level.42 For example, BAT wanted ‘Provisions that […] allow flexibility for governments to adopt [T&T] technologies that meet their own national circumstances’.35

Internal documents suggest that BAT was again generally pleased with the outcome, noting for example, that on due diligence, the text from the informal working group was ‘Much less prescriptive than versions considered in INB4, and less prescriptive than the cooperation agreements entered into with the EU and government of Canada’.43 This is particularly telling given BAT saw the legally binding agreement with the European Union (EU), signed on 15 July 2010 as a result of legal proceedings against the company over smuggling allegations,30 36 44 45 as ‘voluntary’ and beneficial to the company.46 Academic analysis has also noted the inefficiency and potential counterproductive effects of the EU’s agreements with BAT and other TTCs.30

Targeting competition

BAT saw in the Protocol an opportunity to ‘create a level playing field whereby all manufacturers and others involved in the distribution of tobacco products would be bound internationally by the strict controls that the Protocol could introduce’, an interviewee told the authors.47 This is reflected in an internal BAT document from 2009 which argues:

The Protocol provisions need to apply to ALL manufacturers—there should be no exemption for small to medium size enterprises. Illicit product is illicit regardless of the size of the company that manufactured it.48

Similarly, PMI pointed out in a 2010 document that ‘given the nature of the illicit trade in tobacco products today, the exclusion of small and medium-sized businesses would seriously undermine the effectiveness of the Protocol’.49 The ITT has evolved over the years, with an increasing role played by smaller tobacco companies many of whom, it appears, learnt from the practices of the TTCs.21 50 51 Thus, the Protocol applying to all manufacturers—as is the case in the final version—is positive. However, such language—not specifically focusing on TTCs and their complicity in the ITT—provides an opportunity for TTCs to target competitors, consolidate their already predominant market positions and divert attention from their continued role in the ITT.15

Setting up low-cost, low-impact T&T

An interviewee noted: ‘As the idea of an Protocol transitioned into a formal process many of the TTCs saw little merit in a [T&T] system and rather saw it as a complete waste of money.’47 BAT in fact began by arguing against a global T&T regime altogether.36 52

As the idea of a T&T system became entrenched, BAT shifted to shaping requirements on T&T. BAT initially opposed pack-level T&T, arguing for master-case T&T instead claiming that ‘Smugglers of large volume principally deal in master-cases and cartons’ and noting that ‘they were developing a T&T system accordingly’.31 An interviewee pointed out BAT’s primary concern on that issue was in fact financial: pack-level T&T would cost them more money.47 A system not targeting packs would also have created further opportunities for ‘ant-smuggling’ (illicit trade in a vast number of small consignments), which the industry has been complicit in.1 A 2010 PMI document suggests that the company was more open to the idea of pack-level T&T, given that their technology was more advanced.49 The final text of the Protocol applies to all package units (Article 8).17

Both BAT and PMI argued against proprietary systems, as is consistent with the final text.31 49 BAT also fought against a T&T system entirely controlled and operated by governments or designated third-party solution providers.31 The final text, by requiring specific information which can only be obtained with input from the manufacturer, ensures they retain a significant role in the system—a positive outcome for BAT.53 An interviewee suggested the industry has pushed for this requirement for this very reason.53

Finally, BAT stressed the importance of a low-cost, low-impact system that would have little effect on its productivity.31 BAT’s focus here appears to have been on avoiding paper tax stamps, which they perceived as a ‘threat’.36 According to an interviewee, there are multiple reasons why BAT and other TTCs are adamantly opposed to paper-based tax stamps and in favour of digital-only solutions. These include that: tax stamps are ‘more secure and harder to circumvent’ making it harder for TTCs to divert products to the ITT; TTCs consider putting tax stamps on packs an additional ‘burden’; they are ‘more expensive than cheap security infrastructure’; and tax stamps require a third party to monitor TTCs’ activities.53–55 In an internal email in April 2012, one BAT executive wrote that revenue authorities in central and eastern Africa ‘would all prefer a supplier/integrator who can supply both Digital Tax Verification and paper stamps so there is a contingency during change over and in the event of system failure due to the Continents current lack of infrastructure compared with Europe or the Americas’.54 Crucially, tax stamps are not controlled by the TI, in contrast with the main digital-only system available: Codentify, now Inexto.

By 2009 the industry indeed had its own digital T&T system it was hoping to promote. In April 2009, the Codentify patent was granted in Europe.56 PMI then licensed Codentify to BAT and other TTCs in November 2010.57 In this context, a September 2009 BAT document on the INB3 draft (from 5 July 2009) suggested including the word ‘digital’ in the text on the stamping and marking regime.48 In preparation for CoP5 (when the Protocol was adopted) a 2011 internal document noted: ‘Stamping and coding should be digital (Codentify)’.58 The Protocol now encompasses paper and digital solutions,17 which though it enabled governments to put in place tax stamps, also paved the way for the roll-out of the TI’s flawed T&T system, Codentify (online supplemental appendix III).

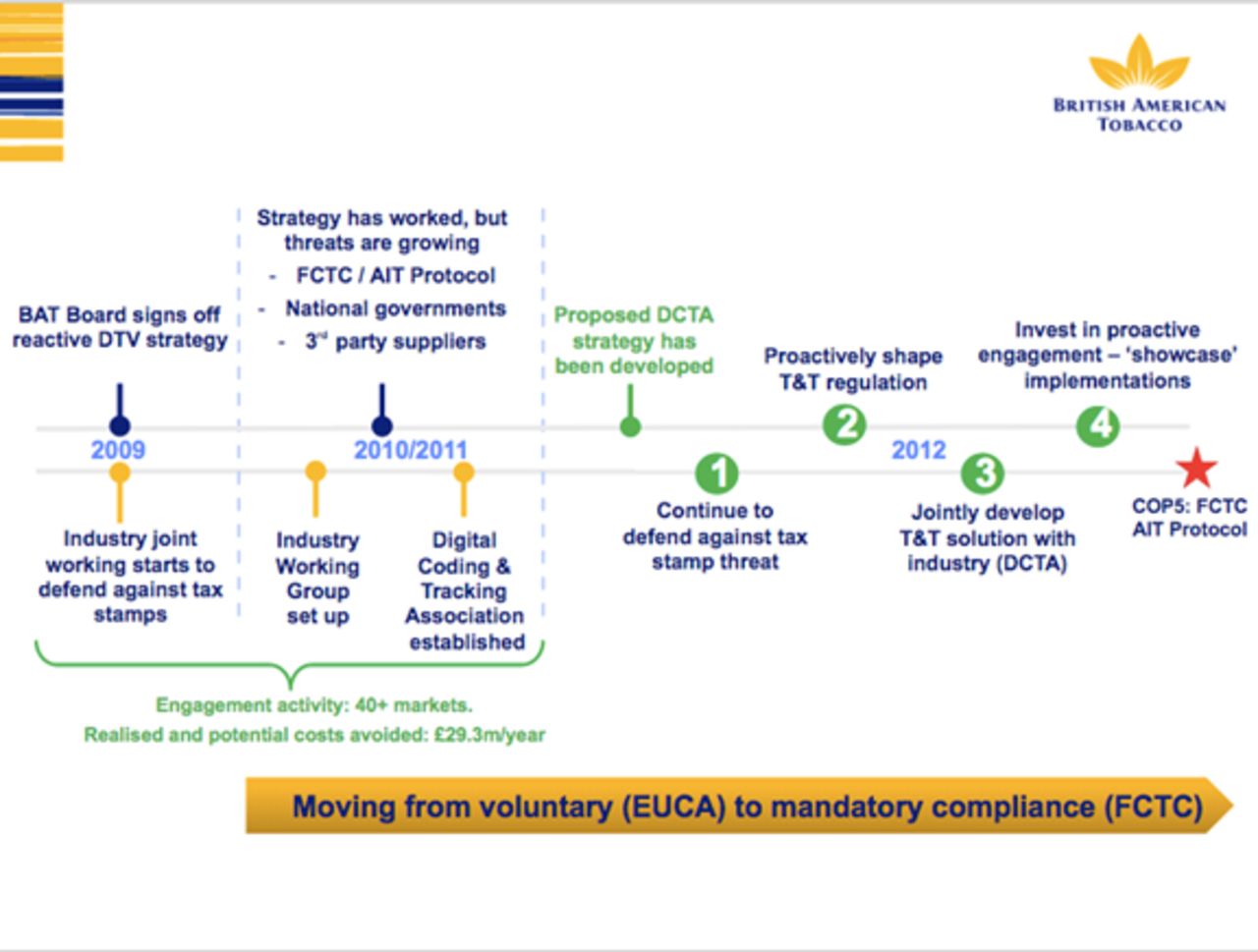

In parallel to their efforts to shape the text of the Protocol on T&T and in anticipation of its implementation, BAT aimed to ‘proactively shape regulation to drive the introduction of effective, low-cost and low-impact [T&T] solutions’36 at the national level (Figure 2), for governments to implement Codentify. Previous research documents how ‘TTCs are engaged in an elaborate campaign to control the global T&T system the Protocol envisages’ via promotion of Codentify as the 'T&T system of choice'.15

{kind=link}

{kind=link}

‘Progress & Strategy’. Source: BAT, October 2012.36 AIT, Anti-Illicit TradeBAT; British American Tobacco; COP, Conference of the Parties; DCTA, Digital Coding and Tracking Association; DTV, Digital Tax Verification; EUCA, European Union Co-operation Agreement; FCTC, Framework Convention on Tobacco Control; T&T, tracking and tracing.

BAT’s desired outcomes on specific items

The documents demonstrate that BAT attempted to influence multiple specific details of the text in order to turn the Protocol from a threat to an opportunity. This section explores its desired outcomes on these, showing how the final Protocol text largely met BAT’s aims.

Duty-free sales

During Protocol negotiations, a ban on duty-free products was suggested as a way to reduce tax avoidance.59 BAT and PMI documents show that both companies opposed this, arguing instead that all Protocol provisions should apply to duty-free sales as well.49 Article 13 of the final Protocol text noted: ‘Each Party shall implement effective measures to subject any duty free sales to all relevant provisions of this Protocol,’ and included no ban on duty-free sales, which, BAT noted internally, ‘satisfied our position’.43

Free-trade zones

The World Bank defines free-trade zones (FTZs) as ‘fenced-in, duty-free areas, offering warehousing, storage, and distribution facilities for trade, trans-shipment, and re-export operations’.60 From the beginning of the Protocol negotiations, BAT publicly called for greater oversight and enforcement of FTZs.61 62 The final text of the Protocol includes an article on ‘Free Zones and International Transit’ (Article 12), in conformity with this.17

The company’s stance is perhaps surprising given the TTCs’ historic reliance on FTZs as part of their smuggling activities63 64 but it appears BAT’s primary interest was to use the Protocol as an opportunity to reduce manufacturing by smaller competitors in FTZs, not TTC product diversion through these zones.65 In November 2011, a BAT senior official asked BAT anti-illicit trade managers to provide data on cigarettes manufactured in the Jebel Ali Free Zone (Jafza)66 in the United Arab Emirates (UAE) and shipped to their respective markets.67 This was part of engagement efforts with UAE officials to shape the Protocol.68 The internal discussions and figures shared only addressed competitor manufacturing in Jafza, not products—including BAT products—transiting through.69 70 That same month (January 2012), BAT continued to use the FTZ as a transit hub to reach regional markets, including Somaliland.71 72

Intermingling

Tackling intermingling (the practice of transporting tobacco products with other non-tobacco products in the same container or similar transportation unit) as a way to reduce the ITT was the subject of much debate at INB4. A representative from Singapore notably asked: ‘if intermingling was such a serious problem, why was it prohibited in the protocol only in respect of tobacco products passing through free zones?’73 BAT argued against a complete ban on intermingling: ‘it is inevitable that tobacco and non-tobacco goods are mixed at various stages of any supply chain’ and that intermingling was ‘standard practice in the shipping industry’,48—a view which PMI also held.61 A total ban on intermingling was omitted from the final Protocol text (which only prohibits intermingling at the time of removal from an FTZ), an outcome BAT again stated ‘satisfies our position’.43

Accountability and seizure payments

BAT noted with concern in September 2009 a proposed article on seizure payments and manufacturer liability ‘appears to seek to impose absolute liability on a producer, manufacturer, importer or exporter without regard to whether the party was at fault’.48 Internal BAT documents suggested changes to the draft text which would have made it very difficult to sanction any tobacco company. For example, by requiring that fines can only be applied to companies ‘proven to have failed to take due and proper care’, ‘found to have been intentionally and directly complicit’48 or ‘who do not take commercially reasonable steps to prevent their products being smuggled’.52 Although these specific changes are not included in the final text, Article 17 on seizure payments is more highly caveated than the previous version (box 1) which can be seen as a satisfactory outcome for BAT.

Notable changes in Article 17 text over time

INB3 version:

‘For the purpose of eliminating illicit trade in tobacco products, the Parties [may] / [should] [consider adopting] / [shall adopt] such legislative and other measures as may be necessary to authorize competent authorities to levy an amount equivalent to lost taxes and duties from the producer, manufacturer, importer or exporter of seized tobacco, [genuine] tobacco products or equipment used in the production of tobacco products [, if the violation has occurred within the rules provided in the Protocol.]’ [emphasis in bold as per the INB3 draft]

Final Protocol text:

‘Parties should, in accordance with their domestic law, consider adopting such legislative and other measures as may be necessary to authorize competent authorities to levy an amount proportionate to lost taxes and duties from the producer, manufacturer, distributor, importer or exporter of seized tobacco, tobacco products and/or manufacturing equipment.’ [underlined emphasis added by the authors]17 123

At INB5, the Brazilian Chief Delegate asked ‘where the language of Article 17 had come from and specifically whether it had come from agreements between the industry and some countries’, noting that ‘The language was weak and contained so many conditionalities that Parties would be able to avoid implementing it’, and argued that the article should therefore be deleted.73 Following a discussion with other delegates, Chairperson Ian Walton-George ‘replied that the procedure to be followed would be determined by the country concerned; Article 17 merely asked Parties to consider adopting necessary legislative and other measures’.73 In the context of the company’s wish to push decision-making at the national level, this can again be seen as a satisfactory outcome for BAT.

Discussion

BAT successfully influenced the Protocol on key items, namely preventing an outright ban on duty-free sales and intermingling, preventing manufacturing in FTZs and ensuring that the text applies to manufacturers of all sizes, and is sufficiently non-prescriptive in nature. Rather than putting in place the most effective system for tackling the ITT, BAT’s primary interests appear to have been to minimise potential costs to and controls on the company, while undermining small competitors, and to maximise its ability to influence national implementation. Internal documents indicate that BAT was satisfied with many aspects of the final text which also appears broadly favourable to BAT’s stated positions. This suggests that BAT’s strategy to influence the Protocol succeeded, much like ongoing TTC efforts to influence its implementation.15

Limitations and strengths

This paper represents the most comprehensive analysis to date of a TTC successfully shaping the Protocol, and benefits from a unique set of internal documents. Extensive searches were conducted of a large volume of documents. However, the authors note that those documents may not give the full picture of BAT’s strategy on the Protocol as their major source was a single ex-BAT official. Despite his senior regional role, expertise on the ITT and frequent access to leading officials and strategic documents, he was not necessarily privy to all relevant communications.

Additionally, most of the documents are from 2010 to 2012, a key period for Protocol drafting and negotiation, but fewer are available for the earlier Protocol development stage. Also, the documents primarily outline TTC objectives, but provide a limited account of how TTCs worked to achieve these. Nevertheless, the broadly industry-favourable outcomes indicate that the industry was relatively successful in this respect.

Policy implications

This paper’s findings suggest that TTCs may have successfully shaped the Protocol in a manner which makes continued TTC complicity in the ITT possible while also weakening competition from smaller competitors. As such, the Protocol may not be as effective as hoped. Our findings appear to justify earlier concerns of potential undermining of the FCTC and Article 5.3 in particular.74–76

In many parts of the world, the TI cooperates closely with governments in attempting to combat the ITT.77 This cooperation poses risks for the Protocol as well as tobacco control more broadly, particularly if relationships and norms of cooperation spill over into other areas of FCTC implementation.75

For the Protocol to be successful, strong national implementation is therefore crucial. This includes ensuring that the industry’s involvement and complicity in the ITT and its incapacity to control its own supply chains are effectively monitored and sanctioned. In accordance with Article 5.3 of the FCTC and Article 8.12 of the Protocol, it also means guarding against the TI’s interference from participating in the design, negotiation and implementation of legislation to tackle the ITT—including via front groups and third parties.15 78 Without a successful Protocol, there is a risk that the ITT increases, in part due to TI involvement in it and in shaping national policies to tackle it, thereby undermining tobacco control and public health.

Independent and effective T&T implementation by Parties to the Protocol, with the support of the Meeting of the Parties (MoP), is of particular importance. Parties concerned with potential TI interference should participate in MoP2 and help produce specific guidance for all concerned. There is ongoing evidence that TTCs are committed to securing influence at the national level via T&T27 79–81 with, for example, Inexto recently being selected to provide Pakistan’s T&T technology, although this decision was later overruled in a court ruling.82

This paper’s findings also raise the difficulty of effectively excluding the industry from the policy making process and of measuring the industry’s influence over such processes. BAT was able to gain access to documents throughout the Protocol negotiations which were not publicly available and to influence at least one delegate present at some of the negotiations. Yet, even with access to internal industry documents, the full extent of the industry’s influence over the Protocol is still concealed.

The industry’s efforts to influence the Protocol follow in the footsteps of the strategies used by TTCs to influence the FCTC, such as PMI’s attempts to secure WHO accreditation for industry-aligned NGOs so that industry positions could be represented at FCTC negotiations,83 and the efforts of several TTCs to cultivate relationships with governments perceived as being more tobacco friendly such as Japan and Malawi.84 85

These challenges emphasise the need for governments and academics and NGOs to prevent TI policy influence by continuing to monitor and expose its practices. This can be achieved via effective TI monitoring (including of potential allies and front groups) and alerting governments and their officials to the risks posed by collaborating with the industry.

More broadly, this paper indicates the need for stronger provisions in future protocols to the FCTC and for relevant treaties in other sectors (eg, alcohol). For example, more prescriptive provisions, which provide less room for the industry to interfere with country-level implementation, may be preferable.

What this paper adds

What is already known on this subject

The Framework Convention on Tobacco Control’s Protocol to Eliminate Illicit Trade in Tobacco Products (Protocol) is a legally binding instrument developed as a coordinated international response to the global illicit tobacco trade (ITT) and overwhelming evidence of tobacco industry involvement.

There is growing evidence indicating that transnational tobacco companies (TTCs) continue to be the key drivers of contemporary ITT.

Given the industry’s continued role in the ITT, it has sought to control and undermine measures to address it, most notably the implementation of the global tracking and tracing regime envisioned by the Protocol.

What this paper adds

This is the first paper to examine TTC influence on the Protocol, focusing primarily on British American Tobacco (BAT). BAT initially viewed the Protocol as a threat but subsequently executed a strategy to influence its development and turn it into an opportunity.

BAT desired to prevent a ban on duty-free sales and intermingling, support greater enforcement of free-trade zones, provisions making it harder to hold companies accountable for involvement in the ITT, and an industry-friendly track and trace system. This appears to have been to minimise its own costs and risks while maximising those for its competitors.

BAT appeared to be satisfied with the final text which provided for most of its desired outcomes from the Protocol negotiations.

Data availability statement

The BAT documents analysed in this paper are available at: https://industrydocuments.ucsf.edu/.

Ethics statements

Patient consent for publication

Ethics approval

This project has been given a favourable opinion by the University of Bath, Research Ethics Approval Committee for Health (REACH) (reference: EP 18/19 077).

References

Supplementary materials

Supplementary Data

This web only file has been produced by the BMJ Publishing Group from an electronic file supplied by the author(s) and has not been edited for content.

Footnotes

Twitter @benoitgomis, @AllenGallagher_, @BathTR, @BathTR

Contributors ABG, AWAG and AR conceived the idea for the study. BG collected and analysed the data and wrote drafts of the methodology and results sections. AWAG, ABG and AR provided substantial comments and edits. AWAG wrote the abstract, introduction, discussion and ‘What this paper adds’ section with support from BG, ABG and AR. All authors read and approved the final manuscript.

Competing interests None declared.

Provenance and peer review Not commissioned; externally peer reviewed.