Article Text

Abstract

The prices that smokers pay out-of-pocket for their tobacco products ultimately influence their smoking behaviour. Although cigarette excise taxes are arguably the best and most used policy to increase cigarette prices, taxes are only one component of retail cigarette prices. The persistence of lower-priced products, disproportionately purchased by lower-income smokers, in jurisdictions with high excise taxes is an Achilles heel for tobacco tax policy. When governments raise excise taxes, the tobacco industry responds. The industry reduces tax pass-through to minimise the price increases for lower-priced brands and offers price discounts to retailers and coupons to consumers. In addition, smokers who do not quit after tax increases may downshift brands, purchase in bulk or substitute lower-priced tobacco product types. This may be particularly true for price-sensitive smokers, including those with lower incomes. We propose that raising excise taxes will be more effective in reducing the persistence of lower-priced products and income-based smoking disparities when taxes are designed to raise prices frequently and substantially for all products and are combined with (a) minimum price laws and (b) bans on coupons, discounts and other promotions. In combination, these three complementary policies restrict the tobacco industry’s ability to undermine the impact of higher excise taxes upon consumer prices. Very few jurisdictions have implemented comprehensive three-pronged tobacco price regulation, but doing so would likely address many of the limitations that come with a sole focus on raising excise taxes.

- tobacco industry

- taxation

- advertising and promotion

- disparities

- price

Statistics from Altmetric.com

The persistence of lower-priced products in high-tax environments

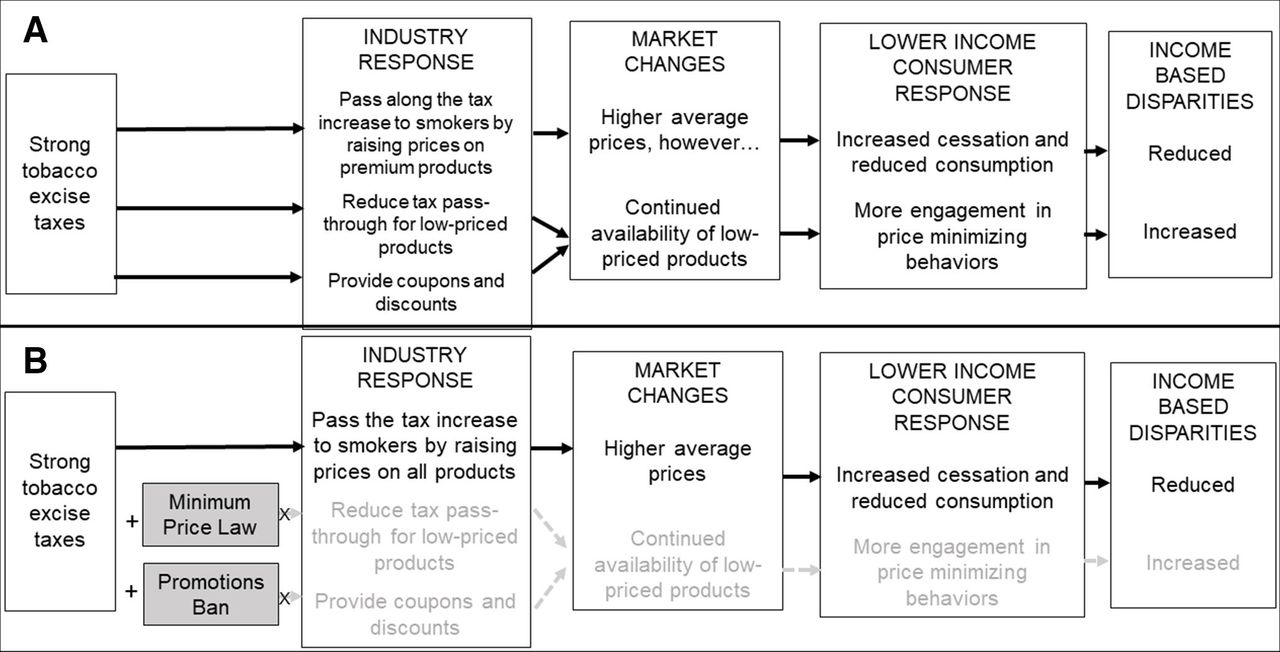

Higher cigarette prices promote smoking cessation, reduce cigarette consumption among those who continue to smoke, prevent former smokers from relapsing and discourage uptake, especially among youth and young adults.1–3 Raising tobacco excise taxes to increase retail product prices is one of the WHO’s six MPOWER measures, an evidence-based policy package to reverse the tobacco epidemic.4 However, the impact of increasing excise taxes can be offset, at least partially, by the tobacco industry’s strategic pricing, which in turn facilitates tobacco users’ behavioural responses, resulting in the continued availability and use of lower-priced products. Industry pricing strategies have important equity implications, as lower-income tobacco users disproportionately buy and consume products from the discount tier, and are more likely to take advantage of coupons and discounts.5–7 Figure 1A illustrates the mechanisms through which excise taxes operate to impact income-based smoking inequities, including ways the industry maintains market segmentation.

{kind=link}

Proposed mechanisms of how tobacco excise taxes influence income-based disparities (A) and the potential impact of a comprehensive three-pronged pricing approach (B).

Tobacco companies have considerable control over the pricing of their products. They can readily offset the impact of excise taxes by using price-reducing strategies and varying tax pass-through based on price segments. The tobacco industry’s price-reducing strategies include coupons, price discounts and other strategies aiming to directly reduce the price that smokers pay out-of-pocket for their tobacco products. Coupons are typically collected by some consumers, whereas the price promotions are managed by the retailer and offered to all customers. In 2019, cigarette manufacturers in the USA spent $5.7 billion on price discounts, representing their largest category (74.7%) of advertising and marketing expenditures.8 Data from the Population Assessment of Tobacco and Health Study9 in the USA showed that 12.4% of non-smokers and 36.2% of adult smokers received a coupon in 2013 and receipt of a coupon predicted progression to regular smoking. Moreover, individuals with incomes lower than 200% of poverty level were more likely to have used coupons. Research in both the USA and the UK documents a high prevalence of price promotions in the retail environment,10 11 and one study found an increase in such promotions following a cigarette excise tax increase.12

Differential tax pass-through between premium brands and discount brands is another way in which the tobacco industry offsets the impact of higher excise taxes. Following a new tax increase, a tobacco company could lower the tax pass-through on discount brands while increasing the tax pass-through on premium brands to maintain profits. As a result, tobacco companies can keep the price of discount brands low and minimise the impact of the tax increase on price-sensitive consumers, including people with lower incomes. Several studies examining retail price data in the UK from 2009 to 2019 found despite regular tax increases, average real prices for the lowest-priced cigarette segments remained steady.13–15

Following a tax increase, many tobacco users reduce their consumption; a study following an Australian tax increase found that 47.5% of smokers cut back or tried to quit smoking.16 However, when lower-priced products remain on the market, rather than quitting or cutting down, some smokers are instead able to keep smoking by engaging in one or more price-minimising behaviours,17 18 such as shopping at lower-priced outlets19 or purchasing lower-priced product types or brands.19 In the Australian study, 11.4% of smokers engaged in these price-minimising behaviours.16 Price-sensitive lower-income smokers are more likely to quit or cut back on their smoking in response to tax increases, but also are more likely to engage in price-minimising behaviours.6

Proposal for a three-pronged price policy

To eliminate the persistence of lower-priced products in the face of tax increases, a more comprehensive approach to pricing policy is warranted. Below we outline a three-pronged approach that combines regular, large increases in specific excise taxes with minimum pricing policies and bans on coupons and promotions. The ways in which these policies limit the industry and consumer responses described above are illustrated in figure 1B. In this paper, we focus on the application of these policies to combustible cigarettes and cigars, as well as roll-your-own (RYO) tobacco. Application of these policies to other tobacco products is certainly possible, but requires additional attention to product definition, package sizing and relative product harm.

Regular large increases in a simple specific excise duty applied equally to all combustible products

The most straightforward way for governments to address the problem of low tobacco prices is to simply increase tobacco excise taxes.20 When excise duty increases, tobacco companies usually increase manufacturer’s prices to maintain profits in anticipation of the expected falls in consumption. Both the increased excise duty and increased manufacturer’s prices increase wholesale prices. Similarly, wholesalers and retailers also seek to increase prices as much as they are able to so as to maintain revenue or at least minimise loss of revenue in a scenario where consumption is expected to fall.21 In some cases, prices go up by more than the magnitude of the tax increase.12 15 21 Consequently, a tobacco tax increase will increase tobacco prices, at least on average, across the tobacco market.

To maximise effectiveness of tax increases, it is necessary to ensure increases in the prices of lower-priced, as well as more expensive, tobacco products. Three design features are important. First, tax levels should be based on the quantity of tobacco (ie, specific excise taxes) rather than the value of the tobacco product (ie, ad valorem taxes).22 By design, ad valorem taxes will be lower on lower-priced products than on more expensive ones, whereas specific excise taxes are designed to be the same for all products of a particular type. Second, excise taxes should comprise at least 70% of the final retail price, as recommended by the WHO.4 In 2020, 52 countries reported having a specific-only excise tax on tobacco, but only 30 met the Framework Convention on Tobacco Control criteria of having excise taxes that comprised 70% of the final price.23 Finally, regular tax increases ensure that taxes continue to make up a substantial portion of price and meaningfully influence behaviour, even under circumstances of high inflation and/or increased consumer wage growth. Substantial, repeated tax increases have been shown to have reduced tobacco use in many low/middle-income countries, including Brazil,24 Turkey25 and the Philippines.26 Large unannounced increases may have even larger effects, denying tobacco companies the opportunity to prepare for the increases.27

In Australia and New Zealand, taxes are simple in structure and the specific excise duty has been increased annually for 8 consecutive years: by 12.5% each year in Australia on top of adjustments for wage growth and by 10% each year in New Zealand in real terms,28 29 taking taxes in these countries to the highest in the world.23 Tax increases have been associated with falls in prevalence in both countries30 31 The volume of tobacco products cleared by tax authorities for home consumption was approximately 32% lower per capita in Australia in 2019/2020 than it was in 201329 and has also fallen markedly in New Zealand.32

Minimum pricing established through minimum price laws and/or minimum excise taxes

Minimum price laws (MPLs) set a legislated price below which a specific tobacco product cannot be sold. In the USA, MPLs originated as an outgrowth of minimum mark-up laws, established in the USA in the mid-1900s to prevent large retailers from selling cigarettes below cost in order to price small retailers out of the market. These minimum mark-up laws require mark-ups on the base cost of a product.33 34 Base costs are derived from wholesaler and retailer invoices, which vary, so these policies do not result in a single statutorily set minimum, but rather vary based on the actual wholesale price. Given that some stores sell hundreds of brands and brand variants, each with their own wholesale price and therefore with mark-ups and final prices of varying dollar value, minimum mark-up laws can be difficult to implement and enforce. More recently, some jurisdictions—rather than imposing a minimum mark-up—have instead established a single floor price, not tied to a base cost, below which no products can be retailed.

MPLs designed with floor prices limit the tobacco industry’s ability to maintain lower-priced products by reducing tax pass-through, as each product on the market cannot be sold below the legislated minimum. When a floor price is set high enough, MPLs could eliminate the sale of discount brands altogether, while potentially leaving prices of premium, expensive products relatively unchanged. Smokers who are particularly price sensitive, including those with limited incomes, might therefore be particularly responsive to MPLs. Alcohol research provides some support for this hypothesis; following the 2018 introduction of minimum unit alcohol pricing, alcohol prices increased in Scotland and consumption decreased the most in lower-income households.35

Real-world evidence in support of tobacco MPLs, however, is limited. Although hypothetical and simulation studies suggest smokers, including lower-income consumers, would reduce consumption following the implementation of an MPL set above the average market price,36–39 only a few implemented MPLs have been evaluated. Two studies of US mark-up laws found little support that they were associated with higher average cigarette prices, except when price promotions were also banned,34 40 although a third found evidence to suggest mark-up laws were associated with higher prices for lower-priced products.41 Malaysia adopted a minimum floor price of 6.40 ringgit (US$1.88) in 2010; in 2011, this was raised to 7.00 ringgit (US$2.31). A small reduction in licit sales below the legislated minimum followed, and there was also a small increase in average prices for those sales. However, more than 96% of licit sales were already above the minimum before implementation.42 In 2014, New York City established a $10.50 minimum price for a pack of 20 cigarettes. An audit study documented very high policy compliance for a premium cigarette brand,43 but, similarly, this is unsurprising since the floor price was set 70 cents below the average price pre-policy.44 In 2018, as part of a suite of tobacco control policies, New York City raised the cigarette floor price to $13.00 and established floor prices for six other tobacco products44; the effects of these new and increased floor prices have not yet been formally evaluated.

The type of MPL implemented in Malaysia and New York City raises concerns among some tobacco control advocates because they may increase profits for retailers or tobacco companies. In some countries, the tobacco industry has actively supported minimum pricing policies, perhaps as a strategy to keep lower-priced competitors out of the market.42 45 Similarly, MPLs can be viewed by lawmakers as stifling competition, and therefore not politically or legally feasible.46

One proposed alternative method of setting a price minimum, currently implemented by nearly 50 countries,4 is a minimum excise tax (MET), which ensures a minimum amount of taxation on each product, regardless of its wholesale price. The UK implemented this approach in 2017, adding a MET to its existing specific and ad valorem taxes on factory-made cigarettes47 and complementing its ban on all promotions of tobacco products that was put in place in 2003.48 This means that, in 2021, cigarettes in the UK generally attract duty of £244.78 per 1000 cigarettes, plus 16.5% of final retail price. However, if the duty on a pack of cigarettes under that formula would work out to be less than £320.90 per 1000 cigarettes in total, then the higher duty level (ie, £320.90 per 1000 cigarettes) applies. In the period following the implementation of the MET, prices on the lowest price factory-made cigarettes increased significantly.47

Because MPLs and METs can effectively increase prices at the lower end of the market, which policy a government opts to implement may be a political or logistical decision. METs may be a good alternative to MPLs in places where MPLs are not legally feasible, in places with concerns about generating revenues for retailers or tobacco companies, and in places where tax levels already comprise a significant component of the overall product price. METs, however, require a strong, well-designed, well-implemented and well-enforced excise tax system, because the implementation of minimum excise taxes tends to be more administratively complex, particularly in places with multi-tiered mixed tobacco tax systems. In addition, METs may potentially exacerbate the price differentials between products with similar risks, if products with similar risk profiles are taxed at different rates. MPLs may therefore be a more straightforward, administratively simpler approach that reduces unintended substitution between different products, especially in places where taxation is politically unpopular or tobacco tax systems are complex or poorly designed.

Ban on coupons and promotions

Coupons and price promotions can substantially reduce the price of tobacco products. Policies to restrict price promotions typically outlaw the distribution or redemption of coupons that lower the price of tobacco products or prohibit the offering of one or more free packs when selling a pack at full price.

As of 31 December 2018, the WHO Report shows that 113 countries4 out of 195 had banned promotional discounts. Many of these countries are banning promotional discounts as part of a broader ban on all tobacco product advertising. In the USA, states are not allowed to ban manufacturers from offering coupons, but they can ban the redemption of coupons at retailers in their jurisdiction.49 Coupon restrictions may also be used in conjunction with minimum pricing such that regulations49 50 prohibit the retailer from accepting coupons that lower the price below the MPL floor price or MET.

Point-of-sale tobacco advertising and product displays are banned in Australia, but price boards listing the names and prices of available products are allowed in most states. Over time, the boards have become more common and are less often being organised alphabetically and more often organised by price, with value brands listed first.51 This suggests that price boards could be a potential loophole to marketing restrictions and should be curtailed. Policymakers may also want to consider banning contracts and agreements between tobacco companies and retailers52 to prevent companies from manipulating product placement or promoting lower-priced products. After a display ban in Scotland, tobacco retailers received incentives for prime product placement behind the display flap, including placing lower-priced products near more expensive ones so that consumers see them when the flap is briefly opened to retrieve the product.53

Implementation of the three-pronged approach: challenges and opportunities

Lower-priced tobacco products remain on the market, even in countries where excise taxes are very high. The three-pronged comprehensive pricing policy approach outlined above combines the advantages of each of three different policies, while at the same time offsetting each policy’s limitations related to the maintenance of a lower-priced product market (table 1). We note a few of these in table 1, focusing on strengths and weaknesses related to market segmentation and recognising that our goal is not to maximise revenue for governments or necessarily to reduce profit for tobacco companies but rather to address the problems posed by widespread availability of lower-priced products. Unfortunately, no country has yet implemented such an approach, so real-world evaluations will be needed to ascertain whether the combined policies can achieve this goal. To enhance potential effectiveness, we offer several potential issues for consideration should jurisdictions explore this three-pronged approach.

Advantages of tobacco control policies that raise cigarette prices

The need for harmonisation of policies across all products

Even with multiple pricing policies, product switching will continue to be a problem unless policies are applied to all tobacco products. In Australia, price discounting is still allowed and there are no MPLs, but couponing and most other forms of promotion are banned,54 and the excise duty increased by 135% in the period 2013–2020.28 Nevertheless, the price of a pack of the leading brand of cigarettes in 2020 was only 57% higher than the price of a pack of the leading brand in 2013.55 Furthermore, many products—including small pouches of RYO tobacco and super-value cigarette products—remain affordable to most consumers. The percentage of adult current smokers using any RYO rose from 32.3% in 2010 to 44.8% in 2019.56 While prevalence of daily smoking fell from 15.9% (±0.6%) of adults in 2010 to 11.6% (±0.6) in 2019,56 harmonising tax policies to ensure similar levels of excise duty were payable on RYO products as on the equivalent number of manufactured cigarettes would likely have resulted in greater reductions in tobacco use.57 58

The need for cooperation across jurisdictions

Even with strong price policies, retailers and consumers can engage in policy avoidance, especially if lower price markets are nearby. For example, New York City currently bans the redemption of coupons or other price promotions, has a minimum price law for cigarettes and multiple other tobacco products, and has a specific excise tax that, while modest by some international standards, is among the highest in the USA.44 Although adult smoking prevalence dropped substantially in New York City over the last two decades, 11.9% of adults still smoked in 2020, and socioeconomic and other disparities remain.59 New York City is geographically small, and is within easy driving distance of places with substantially lower taxes and no additional pricing policies. As a result, cross-border purchasing and smuggling produces an illicit market for lower-priced products.60 61 In other places, in the absence of harmonised policies, consumers are able to travel outside of their jurisdiction with less restrictive price policies or to discount outlets where bulk purchasing is available to maintain lower prices.7 Lopez-Nicolas and Branston have recently suggested that European Union (EU) minimum tax laws be set to a minimum percentage of the average price across all EU countries. This would increase prices in countries where taxes and prices are currently low, reducing consumption in those countries, reducing incentives for cross-border shopping and generating revenues that could be used for public health.58

The need to support lower-income smokers

Although our focus is on reducing lower-priced market segments, the three-pronged approach may help counter other concerns about individual price policies. One critique of non-tax price policies, for example, is that by not generating revenue for governments, they may not support the funding of cessation or other public health efforts. This is less of an issue when a non-tax price policy is paired with an excise tax increase making additional government revenue available for cessation services. Such support is particularly critical for low-income countries, which may rely on tobacco taxes for funding other tobacco control efforts, and for lower-income smokers, who may face financial hardship in light of increasing tobacco prices if they continue to smoke.62 Although tobacco tax increases are sometimes criticised as regressive,63 64 in fact they can be progressive if they result in higher proportions of low-income smokers quitting smoking.65 Because they discourage a shift to the lower-priced products, minimum tax or pricing laws and bans on price promotion most likely would increase the progressive effects of tax increases in encouraging low-income smokers to quit. In addition, a large proportion of those smokers who do not quit will likely reduce the number of cigarettes they smoke per day. While this is unlikely to reduce their risks of disease, it may well increase their probability of success for future quit attempts.

The need for enforcement

Although the three-pronged price policy guards against the drawbacks of an excise tax increase in isolation, it may be more difficult to introduce in a jurisdiction where there are high levels of use of illicit tobacco or in jurisdictions that have weaker tax administration systems. Nevertheless, raising excise taxes creates new revenue streams that can be earmarked to increase staffing and expand systems for tax administration.

Conclusion

Governments around the globe have made great strides in tobacco control over the past five decades, in large part due to strong tobacco tax policies that have increased the price of cigarettes. However, lower-income smokers around the world continue to face a high tobacco burden with continued availability of lower-priced tobacco products. Strengthening excise tax policies to ensure they are applied equally to all combustible products, that they account for a significant portion of product prices and that they are supplemented with laws that minimise the availability of lower-priced products holds great promise for reducing socioeconomic disparities. Intentionally implemented together, these measures could go beyond a simple three-pronged approach, to become a troika of tobacco pricing policy—working together to synergistically turbo-charge tobacco control towards the endgame.

What this paper adds

Although tobacco excise taxes increase prices and reduce consumption, the tobacco industry may overshift the tax to more expensive products and offer coupons and price discounts to ensure lower-priced products remain available.

Tobacco industry tactics allow price-sensitive consumers, including lower-income smokers, to practise price-minimising behaviours that undercut the impact of a tobacco excise tax increase.

A three-pronged approach, whereby substantial specific excise tax increases are paired with minimum price laws and bans on coupons and price promotions, has the potential to reduce disparities in smoking rates between lower-income and higher-income groups.

Few jurisdictions currently implement this three-pronged approach, but lessons can be learnt from places implementing it.

Ethics statements

Patient consent for publication

Ethics approval

This study does not involve human participants.

References

Footnotes

Twitter @KurtRibisl, @JidongHuang

Contributors KMR conceived of the idea. All authors contributed by drafting sections, editing and approving the final version.

Funding Research reported in this publication was supported by the National Cancer Institute of the National Institutes of Health under Award number P01 CA225597 (KMR and SDG).

Disclaimer The funders had no involvement in the writing or interpretation.

Competing interests MS’s work for the Centre for Behavioural Research in Cancer is supported by funding from the Cancer Council Victoria. KMR is a paid expert consultant in litigation against tobacco companies.

Provenance and peer review Commissioned; externally peer reviewed.