Article Text

Abstract

Objective San Francisco’s comprehensive restriction on flavoured tobacco sales applies to all flavours (including menthol), all products and all retailers (without exemptions). This study evaluates associations of policy implementation with changes in tobacco sales in San Francisco and in two California cities without any sales restriction.

Methods Using weekly retail sales data (July 2015 through December 2019), we computed sales volume in equivalent units within product categories and the proportion of flavoured tobacco. An interrupted time series analysis estimated within-city changes associated with the policy’s effective and enforcement dates, separately by product category for San Francisco and comparison cities, San Jose and San Diego.

Results Predicted average weekly flavoured tobacco sales decreased by 96% from before the policy to after enforcement (p<0.05), and to very low levels across all products, including cigars with concept-flavour names (eg, Jazz). Average weekly flavoured tobacco sales did not change in San Jose and decreased by 10% in San Diego (p<0.05). Total tobacco sales decreased by 25% in San Francisco, 8% in San Jose and 17% in San Diego (each, p<0.05).

Conclusions San Francisco’s comprehensive restriction virtually eliminated flavoured tobacco sales and decreased total tobacco sales in mainstream retailers. Unlike other US flavoured tobacco policy evaluations, there was no evidence of substitution to concept–flavour named products. Results may be attributed to San Francisco Department of Health’s self-education and rigorous retailer education, as well as the law’s rebuttable presumption of a product as flavoured based on manufacturer communication.

- public policy

- economics

- surveillance and monitoring

Data availability statement

Retail scanner data are available from third party vendors and are not publicly available.

Statistics from Altmetric.com

Introduction

Flavoured tobacco product availability is related to youth and young adult initiation, experimentation and regular use of tobacco.1 Among California high school students who are current tobacco users, 86.4% of them use flavoured products.2 In addition, almost half of California high school students believed that people their age would not use tobacco products if they were unflavoured.2 Several recent studies demonstrate youth preference for flavoured tobacco products,3 4 and show that flavoured tobacco products are often perceived as less harmful than unflavoured tobacco products.1

The 2009 US Family Smoking Prevention and Tobacco Control Act gave states and localities the ability to restrict sales of menthol cigarettes and all flavoured non-cigarette tobacco products (including menthol). As of September 2020, 322 localities in the US passed restrictions on the sale of flavoured tobacco products, although approximately two-thirds of these local laws exclude menthol.5 The association between implementation of local sales restrictions and changes in flavoured product sales has been documented in some jurisdictions.6–8 However, these studies suggest that policy effects on sales were blunted by industry counteractions, such as the marketing of concept-named flavoured products, (eg, ‘Jazz’ or ‘Wild Rush’),8 which have proliferated over the past decade and raise challenges for enforcing local sales restrictions.9

In June 2017, the San Francisco (henceforth, ‘SF’) City Council passed a flavoured tobacco sales restriction that applied to all flavours (including menthol), all products and all retailers. It was the first comprehensive policy in a major California city. Although a small number of California counties and municipalities implemented local flavoured tobacco sales restrictions as early as 2014, few included menthol products at the time of the SF law, with others following the SF example, more recently.5 Although the tobacco industry gathered enough signatures to force a public referendum, SF voters upheld the law on 5 June 2018.10 On 21 July 2018, the City/County of SF enacted an amendment to their Health Code under Proposition E, Article 19Q. The law affects all brick-and-mortar retailers and online sales to SF addresses and does not criminalise the use of flavoured tobacco by individuals. California recently became the second state to prohibit the sale of flavoured tobacco (including menthol), with exemptions for hookah, large cigars and pipe tobacco in age-restricted venues. However, challenges from the tobacco industry have delayed implementation pending a voter referendum.11

The implementation of the SF law was spearheaded by the SF Department of Public Health (SFDPH). In addition, enforcement also resides with SFDPH, not with the local police department. SFDPH conducted merchant education activities between September 2018 and January 2019 and conducted penalty-free compliance inspections of tobacco retailers between November 2018 and March 2019. Although SFDPH publicised that enforcement would begin in January 2019, compliance inspections with penalties did not commence until April 2019.12 To date, two evaluations of the SF ordinance documented high compliance in a census of retailer inspections,12 and retrospective reports of decreased use of flavoured non-cigarette tobacco products among consumers living or working in SF.13

The current evaluation is the first to study changes in tobacco retail sales associated with the implementation of a comprehensive local policy that applies to all flavours (including menthol), all products and all retailers without exemption. The primary aim was to evaluate the degree to which SF’s comprehensive policy achieved its stated purpose: to eliminate flavoured tobacco sales. Similar to other evaluations of local flavour restrictions,6–8 we measured changes in tobacco product sales with proprietary data collected at the point of sale. Using a single-group interrupted time-series design,14 we assessed the association between SF policy implementation and changes in retail sales of flavoured tobacco products in SF (population 864 263). We also assessed changes in sales in two comparison cities, San Jose (SJ, population 1 023 031) and San Diego (SD, population 1 390 966). Neither comparison city restricts sales of flavoured tobacco, and both cities share California’s tobacco control history and statewide policy environment with SF.15 Additionally, SJ is 50 miles from SF, and the largest city in the Bay Area media market, where advertisements for and against the ballot referendum in SF could have influenced tobacco sales in SJ. SD (500 miles from SF) was selected as a distal comparison city, sharing with SF the influence of a statewide media campaign about flavoured tobacco, but had no sales restrictions in the city or nearby.

We hypothesised that implementation of the SF policy would be associated with declines in flavoured tobacco product sales in SF (consistent with the intent of the local law), while comparable changes would not be seen in the comparison cities. Changes in tobacco sales in these two comparison cities contextualise whether changes in tobacco sales in SF are associated with SF policy implementation or other non-policy related factors shared with the comparison cities. Secondarily, we aimed to assess changes in sales by tobacco product and flavour categories in SF and comparison cities that could indicate unintended consequences of the SF policy implementation, such as increased sales of non-restricted flavours.

Methods

Study design

We used an interrupted time-series design to observe and estimate changes in tobacco retail scanner sales data by tobacco product and flavour category in SF and two comparison cities (SJ and SD), before and after the implementation periods of the SF policy. Weekly sales data facilitated the investigation of changes in sales from the pre-policy period to the policy effective period and from the policy effective period to the enforcement period.

Data source

We licensed weekly tobacco sales data from The Nielsen Company (‘Nielsen’) for SF, SJ and SD to assess retail sales from 1 week ending 27 June 2015 through 1 week ending 28 December 2019. Nielsen used reported sales from a constant panel of retailers to project sales for all similar stores for each city over the study period. Data were assessed for cigarettes, cigars, smokeless tobacco (SLT), electronic nicotine delivery systems (ENDS) and roll-your-own (RYO)/pipe tobacco. Sales were estimated from point-of-sale scanner data obtained from the combined store types: food, drug, mass merchandiser (eg, Walmart); warehouse (eg, Sam’s Club); and convenience stores. The data set provides information on weekly unit sales of tobacco products in advance of and following the enactment (ie, effective date) and enforcement periods of the SF flavoured tobacco sales restriction.

Analysis

Using established methods,7–9 we coded the data to identify and categorise tobacco product subtypes from the main tobacco product categories. SLT subtypes included moist snuff, chewing tobacco, snus, dry snuff and other. Cigar subtypes included large cigars, cigarillos and little cigars. ENDS subtypes included disposable systems, rechargeable systems, prefilled cartridges, e-liquid bottles and accessories. Finally, RYO/pipe tobacco subtypes included RYO tobacco, pipe tobacco and shisha. We created standardised units by product subtype and then aggregated back to the main product level to measure changes in volume by the quantity in which products are most frequently purchased (eg, cigarillos are most frequently purchased as a single pack of two sticks). Based on these data, standardised unit sales for cigarettes are equivalent to one pack of 20 sticks and for cigars, are equivalent to either one large cigar, two cigarillos or 12 little cigars. For smokeless tobacco, a standard unit equals either 1.2 ounces or 1 count of loose moist snuff, 0.82 ounces or 5 count of pouched moist snuff, 3 ounces or 1 count of chewing tobacco, 0.53 ounces or 1 count of snus or 0.21 ounces or 20 count of other (which includes nicotine pouches, dissolvables and dry snuff). For ENDS, a standard unit equals either a 2 count or 2.99 mL of prefilled cartridges, 1 count or 14.99 mL of e-liquid bottles or one disposable device. Raw units were used for assessing sales of ENDS rechargeable systems and accessories due to varying numbers of components included. For RYO/pipe tobacco, a standard unit equals either 0.65 ounces or one count of RYO/pipe tobacco or 8.8 ounces of shisha tobacco. Total tobacco sales include the combined standardised units of cigarettes, cigars, SLT, ENDS and RYO/pipe tobacco. On average, sales of RYO/pipe tobacco made up 0.25% of total tobacco sales in SF over the study period and are only reported in the total tobacco sales outcomes.

Using Nielsen’s provided flavour descriptor, which is based on product packaging text, we categorised flavours as either tobacco/unflavoured, menthol/mint, other explicit flavour (eg, cherry, rum) or concept-named flavour (taste or aroma are unknown based on the flavour description) (eg, magic puff). We analysed sales by flavour category, categorising sales as either flavoured (menthol/mint, explicit, concept) or unflavoured (tobacco/unflavoured). This aligns with the SF law that prohibits the sale of tobacco with constituents that impart a characterising flavour, defined as one that includes tastes or aromas related to fruit, chocolate, vanilla, honey, candy, cocoa, dessert, alcoholic beverage, menthol, mint, wintergreen, herb or spice.16

We graphed trends in sales by tobacco product and flavour category for SF and comparison cities. We used single-group interrupted time series analysis (ITSA) models to estimate within-city changes associated with both the effective and enforcement dates of the SF flavour tobacco restriction for each outcome and each city separately. These models estimate a regression line for each period (pre-policy, between the effective and enforcement dates and after the enforcement date). The week ending 21 July 2018 was used as the policy effective interruption period, and the week ending 5 January 2019 was used as the policy enforcement interruption period. The parameters of the regressions indicate the shift in the level of sales at each policy date as well as the change in slope of the regression lines from period to period. Models assessed weekly sales over the pre-policy period (week ending 27 June 2015 to week ending 14 July 2018), the effective period (week ending 21 July 2018 to week ending 29 December 2018) and the enforcement period (week ending 5 January 2019 to week ending 28 December 2019). We used Stata’s ITSA command for regression analysis to estimate the effect of policy implementation on the weekly time-series of various outcome measures (eg, standardised unit sales of menthol cigarettes) for each study city.14 All models controlled for autocorrelation and heteroscedasticity. Additional control variables in the regression models were quarterly indicators for seasonality and an indicator for the US$2 increase in California’s cigarette excise tax on 1 April 2017.17 18 Our regression model is specified in online supplemental tables 1 and 2.

Supplemental material

Supplemental material

Using the regression estimates, we predicted average weekly sales for each study city and each outcome for the pre-policy period, the effective period and the enforcement period. We used Stata ‘margins’ to estimate predicted average weekly sales and Stata ‘margins contrasts’ to test the differences in average weekly sales across the pre-policy, effective and enforcement periods. All analyses were conducted using Stata V.16.19

Results

Descriptive results

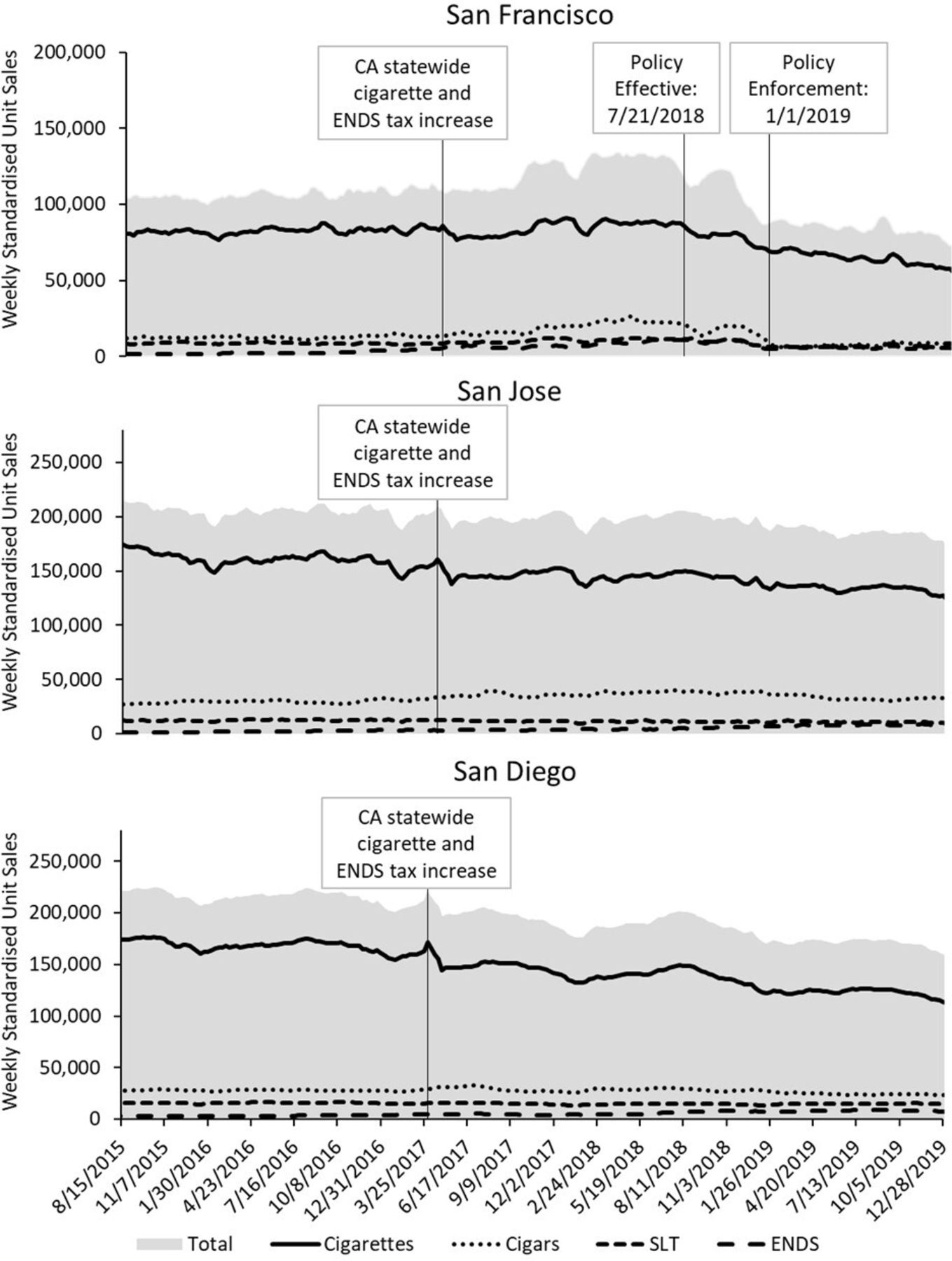

Sales of flavoured tobacco in SF decreased following the effective date and then decreased again, to near zero units per week, following the enforcement date (figure 1). While flavoured cigar and flavoured ENDS sales were initially increasing, by the end of the study period weekly sales of all flavoured tobacco products in SF were near zero units. Flavoured tobacco sales in SJ and SD remained relatively stable, aside from a decrease in cigarette sales occurring around the effective date of the statewide cigarette tax increase and an increase in flavoured ENDS sales through 2018 and 2019. Online supplemental figures 1‒3 show trends in unit sales by flavour category for cigarettes, cigars, SLT and ENDS in SF, SJ and SD, respectively. These trends illustrate the variability by product type and flavour over the study period.

Supplemental material

Flavoured tobacco standardised unit sales (weekly 4-week moving averages), San Francisco, San Jose and San Diego, July 2015–December 2019. Note: Weekly values shown represent the 4-week moving average (eg, the units for the week ending 28 December 2019 are the average weekly units of this week and the three prior weeks). CA, California; ENDS, electronic nicotine delivery systems; SLT, smokeless tobacco.

Total tobacco sales in SF were approximately 106 000 units per week during 2015 and 2016, increased from mid-2017 to mid-2018 in line with increased cigar and ENDS sales, and rapidly decreased in the weeks leading up to the enforcement date of the policy, remaining at a new lower level through 2019 of approximately 85 000 units per week (figure 2). Total cigarette sales steadily trended downward following the effective date, and cigar, SLT and ENDS unit sales decreased between the effective and enforcement dates and then levelled out. In SJ, total tobacco sales were relatively stable throughout the study period, with decreased sales of cigarettes but increased sales of cigars and ENDS. Total tobacco sales in SD trended downward throughout the study period, driven by decreased cigarette sales; cigar and SLT sales remained relatively constant while ENDS sales increased.

Total tobacco standardised unit sales (weekly 4-week moving averages), San Francisco, San Jose and San Diego, July 2015–December 2019. Note: Weekly values shown represent the 4-week moving average (eg, the units for the week ending 28 December 2019 are the average weekly units of this week and the three prior weeks). CA, California; ENDS, electronic nicotine delivery systems; SLT, smokeless tobacco.

Regression results

Flavoured tobacco sales

The estimated level of flavoured tobacco unit sales in SF did not significantly change in the week that the flavour restriction went into effect (July 2018), while the effective period trend (July–December 2018) resulted in 1546 fewer flavoured tobacco units sold per week, on average, relative to the pre-policy trend (p<0.05) (online supplemental table 1). In the week that enforcement began (week ending 5 January 2019), the level of flavoured tobacco sales decreased by 15 838 units (p<0.05), while the post-enforcement trend became flat (ie, it was not significantly different from zero). Table 1 summarises the regression results using predicted average weekly flavoured unit sales for SF and each comparison city, by the pre-policy period (July 2015–July 2018), the effective period (July–December 2018) and the enforcement period (January–December 2019). Predicted average weekly flavoured tobacco sales in SF decreased 96% from 39 350 units sold per week in the pre-policy period to 1546 units sold per week in the enforcement period (p<0.05). Meanwhile, average weekly flavoured tobacco sales did not significantly change in SJ and decreased 10% in SD (75 017 units to 67 202 units) (p<0.05) over the same period.

Predicted* estimates of average weekly flavoured tobacco standardised unit sales, San Francisco and comparison cities, July 2015–December 2019

For menthol cigarettes, predicted average weekly sales in SF decreased 96% between the pre-policy and enforcement periods (p<0.05) (table 1). Predicted average weekly sales of menthol cigarettes also decreased in the comparison cities (11% in SJ and 20% in SD; each p<0.05), but remained at levels substantially higher than in SF. For flavoured cigars, predicted average weekly sales decreased 96% in SF (p<0.05), did not significantly change in SJ and decreased 13% in SD (p<0.05). For flavoured SLT, predicted average weekly sales from the pre-policy period to the enforcement period decreased 97% in SF, 3% in SJ and increased 3% in SD (each, p<0.05). For flavoured ENDS in SF, predicted average weekly sales increased in the effective period before decreasing in the enforcement period, while sales in SJ and SD increased consistently over the study period. From pre-policy to enforcement, predicted average weekly flavoured ENDS sales in SF decreased 100%, while sales in SJ and SD significantly increased by 195% and 118%, respectively (each, p<0.05).

Total tobacco sales

The change in the trend of total unit sales for tobacco in SF during the effective period relative to the pre-policy period resulted in 1355 fewer units sold per week, on average (p<0.05). The change in trend during the enforcement period relative to the effective period resulted in an additional 1019 units sold per week (p<0.05). These significant changes in trend resulted in a post-enforcement trend of -162 tobacco units sold per week, on average (p<0.05) (online supplemental table 2).

Table 2 summarises the predicted average weekly total unit sales for each study period by product category. Predicted average weekly total tobacco sales in SF decreased 25% from pre-policy to enforcement (p<0.05), and by 8% and 17% in SJ and SD, respectively (each, p<0.05). Predicted average weekly sales in SF from pre-policy to enforcement were significantly lower across all tobacco products except ENDS. In SF, total cigarette sales decreased by 23%, total cigar sales decreased by 51% and total SLT sales decreased by 37% (each, p<0.05). Decreases in total tobacco sales were predicted in SJ and SD also, but not by the same magnitude as in SF. Predicted average weekly ENDS sales were 44% higher in SF during the enforcement period compared with the pre-policy period and were 171% higher in SJ and 98% higher in SD (each, p<0.05).

Predicted* estimates of average weekly total tobacco standardised unit sales, San Francisco and comparison cities, July 2015–December 2019

From the pre-policy period to the enforcement period, the proportion of sales for tobacco-flavoured products in SF increased 32.8% points from 65.4% to 98.2% of total tobacco sales, while the proportion of tobacco-flavoured sales decreased in SJ and SD (each, p<0.05) (figure 3). The proportion of explicit and menthol/mint sales significantly decreased in SF (6.9%–0.3% and 26.5%–1.1%, respectively) but significantly increased in SJ and SD (each, p<0.05). The proportion of concept-named flavour product sales decreased for SF and SJ from the pre-policy to enforcement periods (each, p<0.05) and was unchanged for SD.

{kind=link}

{kind=link}

{kind=link}

Average weekly standardised unit sales of all tobacco products by flavour category before and after the San Francisco restriction on flavoured tobacco sales, San Francisco and comparison cities, 2015–2019. Note: Average weekly tobacco unit sales and proportions of sales by flavour category are derived from predicted estimates. Bolded values denote significant differences in the proportion of sales from pre-policy to post-policy, within study cities and flavour category (p<0.05).

Discussion

This study measured changes in tobacco sales with respect to implementation of SF’s comprehensive flavoured tobacco sales restriction. Results revealed that sales of tobacco products declined in ways that were intended by the local law and were not comparable to estimated changes in comparison cities without local sales restrictions. Sales of all flavoured tobacco products, including menthol, decreased by 96% in SF from the period before to the period after implementation of the flavoured tobacco policy, from 34.5% of total tobacco product sales to less than 2% over a 7-month period. Although flavoured tobacco sales, except ENDS (and SLT in SD), decreased in comparison cities, the decline was not as dramatic and did not reach the very low levels seen in SF. A decrease in total flavoured sales in SD was relatively small and driven by the decrease in menthol cigarette sales in that city. Increased sales of flavoured ENDS in SJ and SD parallel national trends during the study period20 21 while implementation of the comprehensive sales restriction might have suppressed this secular trend in SF.

A reduction in total tobacco sales in SF suggests there was not a one-to-one substitution of tobacco/unflavoured products for flavoured products. Although flavoured tobacco sales decreased during the effective period, flavoured product sales in SF did not reach or remain at very low levels until after the enforcement period began. These findings are consistent with data showing that SF retailer compliance with the policy increased from 17% in December 2018 to an average of 80% throughout 2019, when enforcement was in effect.12 Unlike the findings from other evaluations of flavoured tobacco sales restrictions,7 8 22 SF sales of concept-named flavoured tobacco products, such as Jazz cigarillos, also declined substantially following implementation, as intended by the law. The reduction in flavoured tobacco sales, including among concept-named flavours, could be attributed to efforts by the SFDPH and affiliated volunteers to educate themselves about ambiguously named products and conduct rigorous retailer education prior to enforcement,12 and an ordinance provision that states, ‘There shall be a rebuttable presumption that a Tobacco Product […] is a Flavoured Tobacco Product if a Manufacturer or any of the Manufacturer’s agents or employees […] has made a statement or claim directed to consumers or to the public that the Tobacco Product has or produces a Characterizing Flavour, including, but not limited to, text, color, and/or images on the product’s Labeling or Packaging that are used to explicitly or implicitly communicate that the Tobacco Product has a Characterizing Flavour’.16 Future research could disentangle the relationship between retailer education, compliance and sales, including any specific effect of locus of enforcement authority (eg, efficiencies with SFDPH leading implementation and enforcement efforts, rather than a traditional law enforcement agency). These results indicate that local public health departments can successfully enforce flavoured tobacco sales restriction and may be well-positioned to do so with an emphasis on retailer education.12 23

The current study suggests that a comprehensive local law can have the intended effect of nearly eliminating flavoured tobacco product sales in the jurisdiction. However, the downstream impact of the SF policy on consumer behaviour (eg, prevalence of use, quitting, product substitution, cross-border purchasing) warrants additional investigation. In a retrospective study of a convenience sample of young- adult flavoured/menthol tobacco users living or working in SF, self-reported prevalence of any flavoured tobacco product use dropped post-policy but respondents who smoked menthol cigarettes or used flavoured e-cigarettes, exclusively, reported still using these products.13 Moreover, 15% of users reported purchasing flavoured tobacco online, 12% reported purchasing these products outside of SF and 10% reported having purchased products illegally.13 Thus, despite the significant associations between SF policy implementation and the decline in retail sales revealed in the current study, comprehensive state and/or federal laws seem necessary to eliminate opportunities to evade local laws.

This is the first study to assess the impact of a comprehensive local sales restriction of flavoured tobacco products, and inclusion of two within-state comparisons is a strength. While the use of retail scanner data provides strengths—including providing time-series information on product sales in a geography with unparalleled product-level granularity—these proprietary data have known limitations. Representation is limited to the types of stores from which Nielsen collects and estimates sales, therefore online sales and sales from small local retailers, such as small grocery stores, vape shops and specialty tobacco shops that do not use scanner technology, are unknown. Some of these smaller, specialty stores may sell a wider variety of flavoured tobacco products. Options for comparison cities were limited by availability of local-level data from Nielsen. We cannot verify sales estimates as Nielsen’s methods for data collection and weighting are proprietary. Nonetheless, these data are widely used in tobacco surveillance and policy evaluation7–9 20 21 24–26 especially in the USA, where government agencies do not require tobacco manufacturers to report on product sales to wholesalers and retailers as is the case in other countries.27 Although the study period coincided with the June 2019 passage of the SF ordinance banning ENDS sales, the ENDS law did not take effect until January 2020, and its impact might not have been realised until implementation, as seen in the current study and in similar policy evaluations.7 8

The comprehensive SF law virtually eliminated the sales of flavoured tobacco products and decreased total tobacco sales in the city. Contrary to evaluations in New York City and Providence, Rhode Island and other US cities, there was no evidence that consumers shifted their retail purchases to flavoured products with ambiguous (concept-named) labelling.7 8 In addition, increased sales of unflavoured products in assessed retail channels did not make up for the reduction in flavoured product sales, suggesting there was not a one-to-one substitution of unflavoured products for flavoured products. The extent to which SF consumers of flavoured tobacco products quit smoking, reduced consumption or accessed preferred products from cross-border purchases, online vendors or illegal markets is not well documented. Given the gaps in Nielsen coverage of tobacco sales in vape/smoke shops and other small retailers, observational studies of compliance in these under-represented store types are warranted. Studies of how the retail environment and consumer behaviour changed with respect to SF’s comprehensive law, using observational studies and population surveys, are needed to expand the evidence base for local sales restrictions on flavoured tobacco and to offer practical insights for tobacco control researchers, policymakers, advocates and enforcement agencies.

What this paper adds

Hundreds of localities in the USA have implemented sales restrictions on flavoured tobacco, but most local laws contain exemptions for menthol, or for specific products, such as e-cigarettes, or for retailers, such as adult-only venues.

San Francisco is the first major US city to implement a comprehensive sales restriction on flavoured tobacco, without exemptions. The law became effective on 21 July 2018, had a publicised enforcement date of 1 January 2019 and compliance inspections commenced during April 2019.

This study of the San Francisco law is the first to evaluate the impact of a comprehensive flavoured tobacco restriction on tobacco product sales in the USA.

Implementation was associated with significant declines in sales of flavoured tobacco products, which fell to very low levels, and total tobacco sales significantly decreased from pre-policy to post-policy, suggesting there was not widespread substitution to unflavoured tobacco products.

Data availability statement

Retail scanner data are available from third party vendors and are not publicly available.

Ethics statements

Patient consent for publication

Supplementary materials

Supplementary Data

This web only file has been produced by the BMJ Publishing Group from an electronic file supplied by the author(s) and has not been edited for content.

Footnotes

Contributors TR, DGG, LH and EA-R conceptualised and designed the study; DGG and JG conducted data analyses; DGG, JG, TR and AF drafted the article; all authors contributed to writing and editing, and approved the final version of the article.

Funding Funding for this study was provided by the Centers for Disease Control and Prevention Grant #5 NU58DP005969-04-00 and the California Department of Public Health under contract from Stanford Prevention Research Center to RTI International (Contract #17-10041). Additional support for LH and TOJ was provided by the National Institutes of Health/National Cancer Institute, grant #1P01CA225597.

Competing interests The California Department of Public Health was involved in the study design, data collection, analysis, interpretation and writing. CDPH reviewed the text prior to submission and did not influence whether and where to submit for publication.

Provenance and peer review Not commissioned; externally peer reviewed.

Supplemental material This content has been supplied by the author(s). It has not been vetted by BMJ Publishing Group Limited (BMJ) and may not have been peer-reviewed. Any opinions or recommendations discussed are solely those of the author(s) and are not endorsed by BMJ. BMJ disclaims all liability and responsibility arising from any reliance placed on the content. Where the content includes any translated material, BMJ does not warrant the accuracy and reliability of the translations (including but not limited to local regulations, clinical guidelines, terminology, drug names and drug dosages), and is not responsible for any error and/or omissions arising from translation and adaptation or otherwise.