Article Text

Abstract

Background A significant tobacco tax increase has long been advocated to reduce Indonesia’s high smoking prevalence. However, implementing such a policy remains challenging due to the tobacco industry’s argument that it would negatively impact the economy.

Objective This study aims to provide a comprehensive estimate of the net impact of tobacco taxation on Indonesia’s economy.

Method The impact of the tax hike on the economy is simulated through a change in cigarette demand and reallocation of household’s budget and allocation government spending from additional tobacco tax revenue. Input-output analysis is employed to estimate the net effect of the tobacco tax rise on the total economic output, income and employment in Indonesia.

Finding Increasing the tobacco tax would generate a net positive impact on the economy as it would increase economic output, household income and employment. The positive impact is mainly driven by government spending from additional revenue from increased tobacco taxes. Spending tax revenue using the current structure of government spending has the potential to generate the optimal economic effect. Increasing tobacco tax by 45% from the 2019 tax level would increase economic output, household income and employment by Rp84.2 trillion, Rp24.1 trillion and 400.3 thousand jobs, respectively.

- Taxation

- Economics

- Low/Middle income country

Data availability statement

Data may be obtained from a third party and are not publicly available.

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

WHAT IS ALREADY KNOWN ON THIS TOPIC

Few studies have estimated the partial impact of tobacco taxation in Indonesia, which typically quantify its effect on tobacco consumption, tax revenue or employment in the tobacco-related industries. However, a comprehensive estimate of the overall impact of tobacco taxation on the economy is limited.

WHAT THIS STUDY ADDS

This study attempts to provide a comprehensive estimate of the net impact of tobacco taxation on Indonesia’s economy.

Input-output analysis is employed to estimate how changes in final demand due to raising tobacco taxes affect the aggregate economic output, employment and household income.

In addition to simulating the effect of raising the tobacco taxes on cigarette demand and a shift in household consumption, this study also determines the optimal spending allocation in which the government spending from the additional tobacco tax revenue generates the highest multiplier impact.

HOW THIS STUDY MIGHT AFFECT RESEARCH, PRACTICE OR POLICY

This study finds that raising tobacco taxes generates a net positive effect on Indonesia’s economy, which supports for a stronger tobacco control policy through taxation.

Introduction

With an estimated 31% of the adult population smoking tobacco daily in 2019, Indonesia has one of the highest smoking prevalence in the world.1 Smoking prevalence is substantially higher among adult males at 58.3%. It is also concerning that youth smoking prevalence is very high at 19.2% in 2019.2 This significant prevalence of tobacco use has imposed adverse health problems and economic burdens on the country.3 4

High smoking prevalence in Indonesia could be attributed to affordable cigarette prices, which is one of the lowest among Asia Pacific countries.5 While taxes have increased periodically, cigarette affordability only decreased by 10.2% from 2010 to 2017.6 Furthermore, Indonesia’s complex tax structure allows smaller manufacturers to be taxed at a relatively lower rate. For example, between 2010 and 2017, cigarette excise taxes for larger manufacturers increased between 35% and 46% in real terms, while taxes for smaller firms only increased by 15%–24%.7

Studies have shown that tax measures are effective in reducing tobacco consumption both in developed and developing countries.8–13 Furthermore, tax increases have been associated with a decrease in the prevalence of smoking-related diseases, smoking-attributable hospitalisation rates and the number of premature deaths.13–15 In addition to the impact on health, higher cigarette taxes would have a direct impact on increasing government revenues which would stimulate economic activity.10 11 16–18 Previous studies have explored the potential positive effects of cigarette tax increases on economic output and employment due to increased government revenues and increased consumer spending in non-cigarette sectors.7 19

Despite the evidence, a significant tax increase remains a challenge due to the pervasiveness of the tobacco industry’s argument that it would negatively impact the economy. This study uses the input-output (IO) analysis to estimate the macroeconomic impacts of cigarette taxes in Indonesia to test these claims. We simulate the economic impact of cigarette taxes by taking into account (1) the impact on the tobacco sector, (2) the reallocation of household spending to non-tobacco sectors and (3) the allocation of additional government revenues to public spending.

By including the effects of government spending, this study provides, to the authors’ knowledge, the first complete picture of the economic impact of cigarette taxes. We analyse the impact of cigarette taxes on the economy under different government spending structures. As each economic sector has a different multiplier effect, different spending options may have a different impact on the economy. As the cigarette sector in Indonesia is disaggregated into kretek and white cigarettes, we analyse them separately to obtain a more precise estimate.

Cigarette sector and taxation of cigarettes in Indonesia

The cigarette industry in Indonesia has maintained high production levels and enjoyed relatively stable profits despite gradual tax increases and a declining global trend in cigarette consumption.20 Between 2010 and 2019, cigarette sales in Indonesia were between 255 and 315 billion sticks per year (figure 1). This trend indicates that the aggregate cigarette consumption in Indonesia has yet to show any substantial cutback despite the tax and price increase.

Cigarette sales in Indonesia 2010–2019 (billion sticks). Source: GlobalData (2019).

Cigarette consumption in Indonesia is subject to cigarette excise, the subnational government (SNG) cigarette tax and the value-added tax (VAT). Since 2009, Indonesia has been imposing only a specific tobacco excise, which is levied per cigarette stick. The cigarette excise and the recommended minimum selling price (Harga Jual Eceran, HJE) are typically updated annually by the Ministry of Finance (MoF). Meanwhile, the SNG cigarette tax is charged at 10% of the cigarette excise, and the VAT for cigarettes was increased in 2022 to 9.9% of the HJE from 9.1% in 2017–2019 and 8.7% before 2017.

Indonesia has a complex tobacco tax structure that applies different tax rates depending on production volume, production technique (ie, machine rolled vs hand rolled), flavour (ie, with clove or kreteks vs white cigarettes) and retail prices (see table 1).21 In 2020, the structure of cigarette excise was simplified from 12 to 10 tiers, and it was further streamlined in 2022 into eight tiers. Nevertheless, it remains far from the ideal two-tax-tier structure recommended by the WHO.22 This complex taxation system reduces the effectiveness of the tobacco tax policy in curbing tobacco consumption in Indonesia, as it provides incentives to consumers to switch to cheaper brands of cigarettes.

Cigarette excise tax structure in Indonesia

Data and methodology

The IO structure of the cigarette sector in Indonesia

This study employs the 2010 IO tables published by Statistics Indonesia (Badan Pusat Statistik, BPS), which we updated using 2019 data to reflect the more recent economic structure of the country.23 In order to be able to update the IO table to the 2019 values using the sectoral Gross Domestic Product, which consists of 51 industries, we aggregated the IO table from 185 to 51 economic sectors. In addition, the cigarette sector is disaggregated into three subsectors (ie, kretek cigarettes, white cigarettes and others) to better reflect the specific structure of Indonesia’s cigarette market. The disaggregation of the cigarette sector is based on the industrial manufacturing statistics from BPS. Moreover, the insurance sector is disaggregated into two subsectors—the National Health Insurance (JKN) and other insurances. Thus, the final IO 2019 tables consist of 55 by 55 matrix, providing information about the linkages between 55 sectors of the economy.

While it would have been more accurate to further disaggregate the kretek market segment to machine rolled and hand rolled, given their market shares, we were not able to do so since the BPS data do not provide information that would help us make such a distinction. Assuming that hand rolled cigarette consumption is relatively more responsive than machine rolled to a price change, we acknowledge that our analysis may be underestimating the overall impact on consumption. However, as the hand rolled cigarette segment represents less than a quarter of all kretek consumption, we do not expect that this limitation significantly impacts our overall results.

According to the updated 2019 IO table, the total value of the cigarette sector output was Rp238.1 trillion, for which the sector used the value of Rp75.9 trillion of intermediate inputs from agriculture (Rp14.3 trillion), industry (Rp39.5 trillion) and services (Rp22.0 trillion) (see table 2). The produced value added of the cigarette sector was Rp136.5 trillion. Wages and salaries in the cigarette sector represented 18.6% of its total output in 2019, which is more than the average for the whole economy (16.7%). The share of the household demand for cigarettes in total final household demand was 2.6%.

Input-output structure of the cigarette sector (Rp trillion), 2019

Analytical framework

The IO analysis describes the intersectoral relationships within an economy where it shows how the outputs of one sector are used as inputs in other sectors. The analysis is based on economic multipliers that estimate the effects of an exogenous change, such as a tax increase, on economic output, household income, employment, etc. At least two major types of multipliers can be distinguished—the simple multiplier (type I) and the total multiplier (type II). While the type I multiplier includes only the production-induced effects, the type II multiplier also includes the consumption-induced effects (ie, the changes resulting from changes in household consumption). The timeframe of this analysis is short term to medium term, where the multiplier impact of direct consumption may be generated in the short run, while the effect of some public spending may need a longer time to be materialised.

This study models tax increase which is converted to a price increase (table 3). As we do not have information on the retail price, we refer to the minimum selling price (HJE) set by the MoF, which is inclusive of producer price and all taxes imposed on cigarettes, such as cigarette excise, SNG cigarette tax and the VAT. This study assumes the change only in the cigarette excise tax, while SNG cigarette tax and VAT rates remain unchanged.

Estimated impact on consumption and tax revenue by tax increase scenario

As the industry’s response to a tax increase is subject to their business strategy and cannot be easily predicted, for the purpose of this analysis, we assume that the tax is fully shifted onto the consumers. This full tax pass-through assumption is in line with other studies modelling the impact of a tobacco tax increase on consumption.24–26 While a previous study estimates that from 2005 to 2017 Indonesia’s tobacco industry undershifted the tax,21 our analysis of the trend in HJE by year and by cigarette segment shows that the tax pass-through fluctuated year to year (provided in the online supplemental material). For example, the percentage increase of HJE in 2020, as stated by MoF’s regulation, was higher than that of the tax increase, suggesting a tax overshift. On the other hand, since the Indonesian legislation allows the tobacco industry to set the retail price at least 85% of HJE, assuming a full tax pass-through on to HJE may effectively mean undershifting on the retail price. Acknowledging this discrepancy, we also provide the results using overshifting or undershifting assumptions in the online supplemental material.

Supplemental material

Three scenarios of a tax increase are assumed (table 3). Firstly, we assumed a tax increase similar to that in 2020 (S1), where the weighted average tax increased by 23.8% and 27.2% for kretek and white cigarettes, respectively. Assuming a full tax pass-through, the resulting estimated price increase would be 20.8% for kreteks and 23.5% for white cigarettes. Two additional scenarios are assumed—a 30% (S2) and 45% (S3) tax increase for all cigarettes from the 2019 tax level. The weighted average tax and price are estimated based on the reported cigarette sales and share of sales by tax tier in total sales. Based on the GlobalData, 291 billion sticks of kretek cigarettes and 14 billion sticks of white cigarettes were sold in 2019.

To estimate the resulting change in consumption, the following price elasticities are assumed: own-price elasticity of −0.80 for kreteks and −0.33 for white cigarettes, and cross-price elasticity between kreteks and whites of 0.16. As published price elasticity estimates by cigarette segment in Indonesia are very limited, we had to make assumptions based on the available estimates. For kretek cigarettes, the last published price elasticity estimate is the World Bank’s estimate (−0.51) based on the 1980–1995 data,27 which is relatively outdated, while our estimate based on the 2017–2019 National Socioeconomic Survey (SUSENAS) data is −1.02,23 which is on a higher side in comparison to an estimate used by the WHO in their tax model. For that reason, we assume that the own-price elasticity of kretek is −0.80, which is a midpoint between the two estimates. This estimate is in line with a recent study estimating the overall cigarette price elasticity of −0.67.28

On the other hand, we estimate the own-price elasticity for white cigarettes (−0.13) and cross-price elasticity between kreteks and whites (0.16) using 2017–2019 SUSENAS.23 To confirm the consistency of our results, we conducted a robustness check by assuming two additional sets of own-price elasticities. For the lower bound, we assume −0.23 for kretek and −0.30 for white cigarettes,29 while for the upper bound we assume −0.84 for kretek and −0.97 for white cigarettes (results provided in the online supplemental material). In order to isolate the impact of a tax and price change on consumption, we assume no change in income. Finally, we assume no change in the size of the illicit market of cigarettes.

Given the complexity of the Indonesian tobacco tax system, it would have been ideal to have own-price and cross-price elasticities by tax tier. However, since such estimates are not available and are challenging to estimate. Therefore, we do not make a specific assumption regarding downward substitution to cheaper brands within the same segment. While not being able to account for a downward substitution may not significantly impact the estimated change in quantity demanded, as the own-price elasticity is estimated for the entire segment (and not by tier), it may overestimate the revenues.

Under these assumptions, the estimated reduction in the total number of cigarettes sold is between 12.4% and 19.9%, depending on the tax increase (table 3). Meanwhile, due to inelastic demand, the aggregate spending for cigarettes (in monetary terms) after the tax raise is increased by 5.9%–6.5%. In addition, the government tax revenue is estimated to increase between 8.2% and 14.6%, depending on the rate of tobacco tax increase.

We estimate the impact on economic output, household income and employment through three different channels. First, increased cigarette spending would increase the final demand for cigarettes. Second, we assume that increased tobacco spending would proportionately crowd out spending for other commodities since we assume no change in household income, as mentioned above. Third, we assume that the additional government revenues from increased tobacco tax are spent business as usual, (ie, 2% of excise tax revenues must be allocated to the tobacco-producing provinces and must be used for the development of tobacco-related industry (Law No 39/2007), while the rest (98%) of excise tax revenues and all of the tobacco VAT revenues are allocated to the general budget). The business-as-usual spending also allocates revenues from tobacco SNG cigarette tax to the so-called mandated sectors, in the following way: tobacco control law enforcement (50%), JKN-related public health services (37.5%) and non-JKN public health services (12.5%).

In addition to the reallocation of household spending and the business-as-usual allocation of the tax revenues (Sim A), simulations B, C and D assume increased allocation of government spending to selected sectors (table 4). Sim B and Sim C assume that an additional 20% and 98% of excise tax revenues, respectively, are allocated to JKN, public health services, public education services, the pharmaceutical industry and the telecommunication industry for tobacco control campaigns. Sim D is similar to Sim C, except that additional revenues are also allocated to the social assistance programmes.

Simulation scenarios for allocation of additional government revenues

Results

Multipliers

Output multipliers

An output multiplier for the cigarette sector represents the total value of production in all sectors of the economy needed for Rp1.0 worth of final demand for the output of the cigarette sector. As table 5 shows, the cigarette sector used Rp0.37 worth of intermediate inputs to produce an output of Rp1.0. In other words, for every Rp1.0 billion reduction in the demand for the cigarette sector output, the demand for inputs from other sectors decreases by Rp0.37 billion. The indirect effect represents the effect on the sectors which are the suppliers to the input-supplying sectors of the cigarette sector. The estimated indirect effect is 0.26. The resulting simple multiplier is 1.63, implying that Rp1.0 billion reduction in demand for cigarettes decreases the economy’s output by Rp1.63 billion. The estimated total multiplier of 2.31 implies that an overall impact of an Rp1.0 billion reduction in demand for cigarettes reduces the economy by Rp2.31 billion, which includes the reduction of demand by households. In comparison to some other sectors of the economy, the total multiplier for the cigarette sector is below the average (2.48), with the multiplier magnitude for the top five sectors ranging from 3.33 to 3.65, and for the bottom five between 1.57 and 1.88.

Output, income and employment multipliers for the cigarettes sector in Indonesia

Income multipliers

An income multiplier represents the change in the value of income from wages and salaries in the total economy resulting from an Rp1.0 change in the demand for cigarettes. Specifically, the simple and total income multipliers for the cigarette sector are 0.29 and 0.40, respectively (table 5). In other words, an Rp1.0 billion worth of reduction in demand for cigarettes would result in wage and salary reduction in the cigarette sector and its input-supplying sectors in the amount of Rp0.29 billion. The resulting reduction in consumption expenditures from this reduction in income would lead to an additional decline in income of Rp0.11 billion.

Employment multipliers

An employment multiplier measures the change in the number of jobs resulting from an Rp1.0 change in the demand for cigarettes. Table 6 shows that the employment coefficient in the cigarette sector is 3, which is on the lower side in comparison to the coefficient in the top five sectors as well as the average for the economy. The employment effect shows that if the output value of the cigarette sector decreases by Rp1.0 billion, the employment in this sector would reduce by three people. As cigarette sector is not labour intensive, it is not surprising to see such a low employment effect. The total multiplier (table 5) shows that a reduction in demand for cigarettes of Rp1.0 billion would reduce overall employment in the economy by nine persons.

Employment coefficients in selected industry

Macroeconomic impacts

The estimates show that even though the consumption of cigarettes would decline between 12.4% and 19.9%, depending on the tax increase, the increased cigarette tax and price would lead to an increase in households’ spending on cigarettes between 5.9% and 6.5%. As the cigarette excise and VAT revenues from tobacco would increase between 8.2% and 14.6%, depending on the cigarette tax increase, a reallocation of these revenues back to the economy would have a positive net income. The simulation shows that the highest net impact on output, income and employment (table 7) would be achieved with the current scheme of spending allocation (Sim A).

Estimated net impact

It may seem counterintuitive that the current allocation of government spending has a higher estimated net impact than increased spending on healthcare, education or telecommunication. However, this reflects the limitation of the IO method, which does not take into account the long-term effects of this type of spending. For example, greater spending on health or education could result in a healthier and more productive population and with better skills, which would increase their future earnings and support the economic development of Indonesia. However, while this impact cannot be captured by the IO analysis, it is still reassuring that even with the current government spending allocation, increasing the tobacco tax would have a positive net macroeconomic impact.

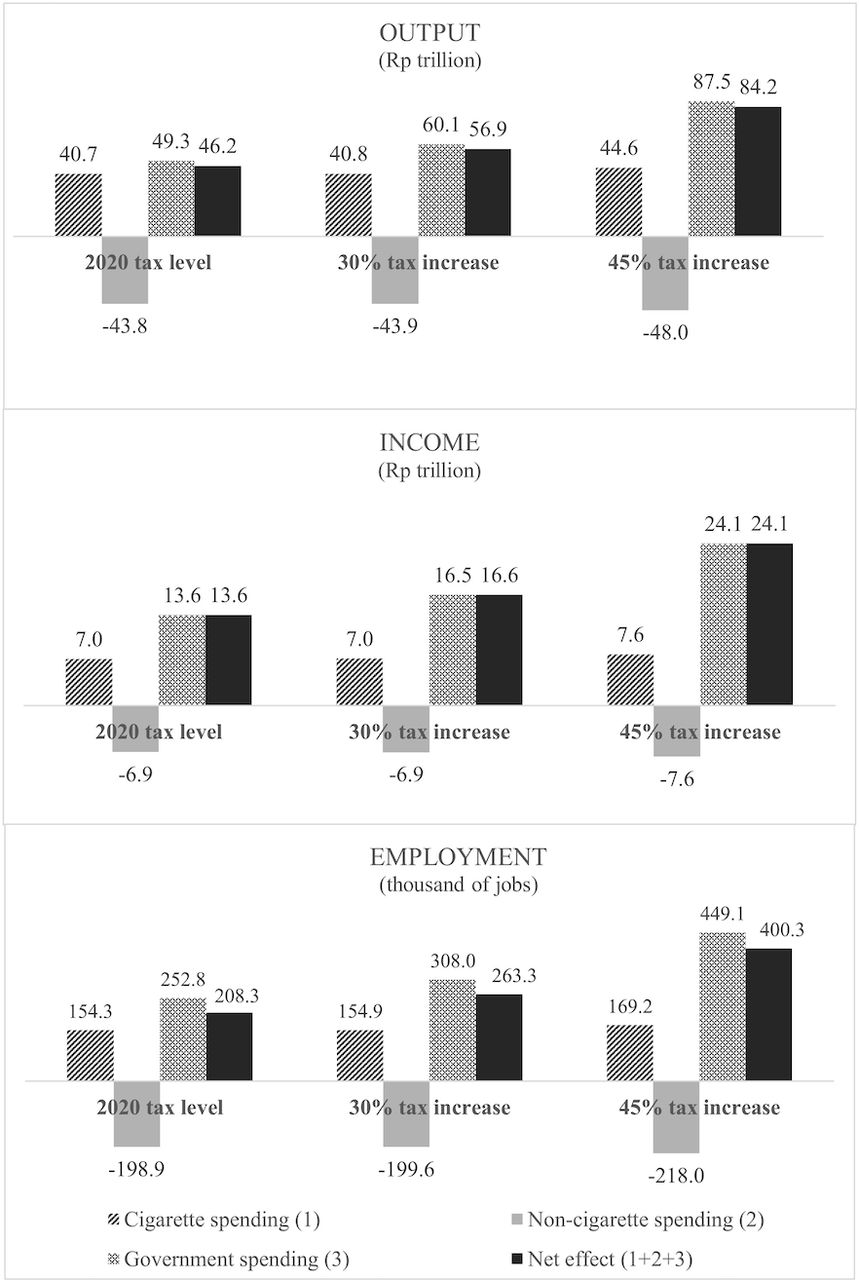

Figure 2 presents the composition of the net effect on total output, income and employment under the current government spending scenario (Sim A). While the impact of increased spending on cigarettes and reduced non-cigarette spending almost cancel each other, increased spending due to the allocation of new tax revenues drives the positive net impact on the economy. The results show that a tax increase by 45% from the 2019 tax would increase economic output, household income and employment by Rp84.2 trillion, Rp24.1 trillion and 400.3 thousand of jobs, respectively.

{kind=link}

{kind=link}

Impact of a tobacco tax increase on the economy (Sim A).

Discussion and conclusion

The study reveals important insights about the macroeconomic impacts of tobacco taxation in Indonesia, which shows that a cigarette tax increase would result in a net positive impact in terms of aggregate economic output, employment and household income. This finding adds to the previous literature, which suggests that raising tobacco taxes in Indonesia would reduce gross employment in the tobacco manufacturing sector by less than 0.5%, and the expected loss in household income would be far less than the potential increase in tax revenue.7 By modelling the inter-relation of industries in the economy, this study provides a more comprehensive estimate which simulates the impact of a tax hike on tobacco consumption and the tobacco industry and its effect on other sectors driven by the reallocation of household spending and public spending from additional tax revenues.

The analysis shows that the net effect of the tobacco tax hike is largely contributed by the government spending as effects from changes in cigarette consumption and household spending reallocation merely offset each other. This highlights the pivotal role of fiscal policy in tobacco control to reduce cigarette consumption through tax measures and to stimulate the economy and redistribute the resources through public spending. Keeping in mind the limitations of the IO analysis as a static model and our inability to disaggregate kretek cigarette segment into machine rolled and hand rolled, this study also finds that the current government spending allocation has been optimal in generating the largest aggregate economic impacts compared with the other proposed spending scenarios. Therefore, public spending from tobacco tax revenues should be spent in a manner that optimises public pay-off, particularly to address for the negative externalities of smoking and to compensate the most adversely impacted sector by the tobacco tax hike.

The results of this study reinforce a long-standing body of evidence of the effectiveness of tax measures in reducing cigarette consumption. The simulation suggests that a significant tax hike that increases cigarette prices would substantially reduce cigarette consumption. Therefore, considering that smoking prevalence in Indonesia is among the highest in the world and consumers in the country enjoy relatively affordable cigarettes, the Indonesian government should adopt and implement the long-standing consensus to ‘go big, go fast’ in increasing cigarette taxes to reduce cigarette smoking.

Increasing cigarette taxes is effective in influencing smokers’ behaviour and beneficial to the economy. This study builds the case for supporting a cigarette tax hike, as it would generate a net positive impact on Indonesia’s economy. Therefore, this evidence also serves as credible evidence as a counternarrative for the tobacco industry’s argument on the negative economic impact of tobacco taxation.

Data availability statement

Data may be obtained from a third party and are not publicly available.

Ethics statements

Patient consent for publication

Acknowledgments

The authors would like to thank Professor Frank Chaloupka (University of Illinois Chicago) and Wasim Saleem (Social Policy and Development Centre, Pakistan) for their valuable inputs and suggestions for improving the article.

References

Supplementary materials

Supplementary Data

This web only file has been produced by the BMJ Publishing Group from an electronic file supplied by the author(s) and has not been edited for content.

Footnotes

Twitter @v_vulovic

Contributors TD is responsible for the overall content and is the guarantor of this paper. AB, DN, YM, UU, and TD conceived and developed the research design. AB, AS, VV, DN and UU conducted the data analysis. AS and VV wrote the manuscript. All authors approved the final manuscript as submitted and agree to be accountable for all aspects of the work.

Funding The Center for Indonesia’s Strategic Development Initiatives (CISDI) is funded by the Institute for Health Research and Policy at the University of Illinois Chicago (UIC) to conduct economic research on tobacco taxation in Indonesia. UIC is a partner of the Bloomberg Initiative to Reduce Tobacco Use.

Disclaimer The views expressed in this document cannot be attributed to, nor do they represent, the views of the Institute for Health Research and Policy, UIC or Bloomberg Philanthropies.

Competing interests None declared.

Provenance and peer review Not commissioned; externally peer reviewed.

Supplemental material This content has been supplied by the author(s). It has not been vetted by BMJ Publishing Group Limited (BMJ) and may not have been peer-reviewed. Any opinions or recommendations discussed are solely those of the author(s) and are not endorsed by BMJ. BMJ disclaims all liability and responsibility arising from any reliance placed on the content. Where the content includes any translated material, BMJ does not warrant the accuracy and reliability of the translations (including but not limited to local regulations, clinical guidelines, terminology, drug names and drug dosages), and is not responsible for any error and/or omissions arising from translation and adaptation or otherwise.