Article Text

Abstract

Objectives To investigate the appropriateness of tax incidence (the percentage of the retail price occupied by taxes) benchmarking in low-income and-middle-income countries (LMICs) with rapidly growing economies and to explore the viability of an alternative tax policy rule based on the affordability of cigarettes.

Design The paper outlines criticisms of tax incidence benchmarking, particularly in the context of LMICs. It then considers an affordability-based benchmark using relative income price (RIP) as a measure of affordability. The RIP measures the percentage of annual per capita GDP required to purchase 100 packs of cigarettes. Using South Africa as a case study of an LMIC, future consumption is simulated using both tax incidence benchmarks and affordability benchmarks.

Results I show that a tax incidence benchmark is not an optimal policy tool in South Africa and that an affordability benchmark could be a more effective means of reducing tobacco consumption in the future.

Conclusions Although a tax incidence benchmark was successful in increasing prices and reducing tobacco consumption in South Africa in the past, this approach has drawbacks, particularly in the context of a rapidly growing LMIC economy. An affordability benchmark represents an appropriate alternative that would be more effective in reducing future cigarette consumption.

- Economics

- taxation and price

Statistics from Altmetric.com

Introduction

This paper outlines two approaches to tobacco taxation policy—tax incidence benchmarking and affordability benchmarking. First, it outlines problems with tax incidence benchmarking, identifying particular issues in the context of low-income and middle-income countries (LMICs) that have shown rapid economic growth, particularly where growth in real income exceeds the growth in real prices. It then proposes an alternative policy benchmarking the affordability of cigarettes, exploring some methodological issues surrounding the measurement of affordability and the construction of an affordability policy rule. Finally, it uses South Africa as a case study of an LMIC to explore the two approaches using simulations of the impact of both benchmarks.

Background—approaches to tobacco taxation

Tobacco control advocates have long promoted higher excise taxes on cigarettes as a means of reducing cigarette consumption. This proposal has been supported by a large body of research that has cemented the negative relation between cigarette prices and consumption. Governments are motivated to increase taxes since they are able to raise significant revenue and because lower consumption has important public health benefits. South Africa is a good example of this: between 1993 and 2007 real excise taxes rose by 357% resulting in real retail prices increasing by 146%. As a result per capita consumption of cigarettes fell by 48% and real excise revenue increased by 215% (Van Walbeek, unpublished, 2005).

Since the World Bank publication, Curbing the Epidemic, tobacco control advocates have promoted benchmarking the percentage of the retail price occupied by tax.1 Based on tax rates used in countries with comprehensive tobacco control policies the World Bank recommended that excise tax account for two-thirds to four-fifths of the retail price of cigarettes.1 Sometimes also referred to as the tax burden or tax incidence, it can refer to excise and sales taxes combined (the total tax incidence), or just excise taxes (the excise tax incidence). This approach has created an easy to understand method by which countries can ‘benchmark’ their tax incidence against global best practice.

A number of notable examples of this practice exist. The European Union (EU) has, since 1993, required member states to meet a minimum excise tax incidence of 57%.2–4 The EU has a minimum VAT rate of 15% (13% on a tax inclusive basis) which cannot be levied at a reduced rate on cigarettes. The minimum total tax incidence is therefore effectively 70%. However some countries, like the UK with an excise tax incidence of 63% and a total tax incidence of 76%, set their taxes above this tax incidence benchmark.5 Another example is South Africa, albeit one that does not meet the two-thirds criteria, where a total tax incidence of 50% was required between 1994 and 2004 and 52% since 2004 (Van Walbeek, unpublished, 2005).

More recently, a growing literature considers the affordability of cigarettes.6–9 The concept of affordability is useful since it considers the simultaneous influence of price and income on cigarette demand. Generally, demand is considered ceterus paribus (all else held constant) with the impact of prices and incomes considered in isolation. Affordability is becoming increasingly important as consumption shifts from the high-income countries (HICs) to LMICs. In HICs slower economic growth allows advocates to focus on raising prices in order to reduce consumption. This ‘price benchmarking’ is appropriate in contexts where growth in prices will exceed the growth in income. However, in LMICs, many of which are experiencing rapid economic growth, focusing on price alone ignores rising incomes.6 Thus even increasing real prices may not reduce consumption since the growth in income may outweigh the growth in real prices.

A critique of tax incidence benchmarking

Using tax incidence as a benchmark brings about a number of problems. Political will is required to raise cigarette taxes, especially in LMICs where the tobacco industry may be particularly influential and a tax incidence benchmark may therefore be difficult to change once attained or established. Furthermore, recent WHO data show that the two-thirds to four-fifths target is rarely reached with a median excise tax incidence of 57% recorded in HICs (max 69%, SD 20%, n=37) and 35% in LMICs (max 79%, SD 19%, n=99) in 2007.5

Benchmarking tax incidence raises the question of whether one should target simply the excise tax or the total tax incidence. This one-size-fits-all approach does pose difficulties since different countries have vastly different tax regimes and uses for those taxes.

The setting of tax incidence benchmarks ultimately provides greater ability for the tobacco industry to set retail prices. Once a target is set, excise taxes need to be reviewed on a regular basis to ensure that the target continues to be met. If the tobacco industry chooses to raise industry/base/net-of-tax prices, excise taxes would have to be increased to ensure the tax incidence benchmark is maintained. Conversely, if the tobacco industry chooses to reduce industry/base/net-of-tax prices, the excise tax may (depending on whether the excise tax is specific or ad valorem) have to be reduced in order to maintain the tax incidence benchmark. (This point may seem trivial since most regimes set a tax incidence benchmark as a floor and thus a decline in the industry/base/net-of-tax price would not require specific excise taxes to be reduced to maintain the benchmark but rather leave the actual tax incidence above the benchmark. However, if an ad valorem tax is used a decline in the industry/base/net-of-tax price may result in a decline in excise while tax incidence remains unchanged.) The tobacco industry's pricing decision is likely to be based on a number of factors including the market structure of the sector, the maturity of the market, the affordability of the product and the structure of excise taxes (ie, specific versus ad valorem). Thus, once the tax incidence benchmark is attained the tobacco industry's pricing strategy will become the deciding factor in influencing retail prices since even specific taxes can then be treated as ad valorem taxes. This leads to the removal of pricing as a public health tool and grants the tobacco industry the de facto ability to set the public health agenda.

Finally, a high tax incidence benchmark does not necessarily result in high prices. Some countries already have a high tax incidence but still have cheap and affordable cigarettes. Figure 1 depicts the total tax incidence and retail price of cigarettes (in US dollars) for a number of countries.

Using a Spearman rank correlation statistic, the correlation between total tax incidence and price is −0.04 (n=25) for HICs and 0.26 (n=38) for LMICs (neither of which are statistically significant at the 5% level). This indicates no relation between price and total tax incidence. Figure 1 shows that HICs generally have a high total tax incidence while prices vary significantly, and LMICs have large variation in total tax incidence with relatively low prices. Figure 2 depicts the total tax incidence and the affordability of cigarettes as measured by the relative income price (RIP) for the same group of countries (see the next section for an explanation and discussion of the RIP measure). The Spearman rank correlation between total tax incidence and affordability is 0.25 (n=25) in HICs and −0.14 (n=38) in LMICs (neither of which are statistically significant at the 5% level). Again this indicates no relation between total tax incidence and affordability.

The affordabilty benchmark

The literature suggests two measures of affordability using narrow7 8 and broad measures of income.6 9 A broad measure of income differs from a narrow measure in that it values non-money income like the provision of public goods and services. I will use a broad measure of income (per capita GDP) as the base for our consideration of affordability since such a measure is more practical in the context of LMICs. In LMICs large portions of the population are dependent on the state provision of goods, services and grants. Narrow measures of income such as money income or wages do not adequately consider the provision of public goods such as education, medical and security services. Furthermore, the broad measure of income can be used in almost all countries on an annual basis while the narrow measures are only available in smaller isolated samples and often in a low-frequency series.6 I use the RIP measure of affordability developed by Blecher and van Walbeek6 9 which is defined as the percentage of annual per capita GDP required to purchase 100 packs of cigarettes. Affordability is expressed as a percentage where higher percentages indicate less affordable cigarettes. An increase in the RIP means that a greater proportion of income is required to purchase cigarettes and hence cigarettes have become less affordable. A decrease in the RIP means that a smaller proportion of income is required to purchase cigarettes and hence cigarettes have become more affordable. An increase in the price decreases affordability as does a decrease in income. Affordability is a purely relative concept and has no absolute meaning so cigarettes cannot be considered affordable or unaffordable unless it is compared to another country, time period, or product.

A country may benchmark affordability in one of two ways, first by committing to maintaining the level of affordability or second by committing to decrease the level of affordability over time. The first would involve increasing the excise tax in such a way that ensures prices rise by the combination of inflation and growth in per capita GDP. The second would involve increasing the excise tax in such a way that ensures the price increases by the combination of inflation and growth in per capita GDP plus a premium. Given the effects of compounding, a small premium can result in a significant change in affordability over several years. It must be noted that tax increases have a small inflationary impact since cigarettes are almost always part of the basket of goods and services used to calculate inflation (tobacco contributes 2.3% to the total consumer price index in South Africa10).

A further consideration is that if an affordability benchmark becomes established and the tobacco industry has significant market power they could increase the retail price in such a way as to take all the ‘rents’. This would occur if the industry preempted an excise tax increase by raising the retail price in such a way that the excise tax increase would no longer be required to meet the rule. In such a case an excise tax increase would not be required in order to make cigarettes less affordable and the state's revenue from cigarettes would decline. Although this is not explicitly a public health concern, much of the popularity of excise tax policy comes about from its revenue generating ability. In a competitive market this is unlikely to occur since manufacturers would want to keep prices as low as possible in order to maintain market share.

South Africa—the current system

Prior to 1993 South Africa had no tobacco control strategy as a result of particularly close links between the state and the tobacco industry. Inflation was allowed to destroy the value of the specific excise tax in real terms over a number of years. The total tax incidence fell from a peak of over 52% in 1972 to a low of 29% in 1992 (see figure 3). In 1994, the new African National Congress government proposed that excise taxes should amount to 50% of the retail price of cigarettes, implying a total tax incidence of nearly 63% (Van Walbeek, unpublished, 2005). (VAT of 14% is applied on the sum of the industry/base/net-of-tax price as well as the excise tax and is levied on most goods and services in South Africa.) This was phased in over a number of years through consistent increases in excise taxes.11

Total tax incidence and excise tax in South Africa. Source: CP Van Walbeek, unpublished, 2005. Note: Data until 2004 were obtained from the source while subsequent years were obtained directly from the author. Tax incidence is read off the secondary Y axis.

The higher excise taxes resulted in significantly higher real prices which in turn led to sharp declines in aggregate and per capita consumption. Higher prices also resulted in a higher RIP until 1999 indicating a sharp decline in the affordability of cigarettes (figure 4) as economic growth was slow. Since 1999, however, the affordability of cigarettes has remained relatively unchanged and, unsurprisingly, per capita consumption has remained flat (see figure 4). The lack of change in affordability is attributable both to stronger economic growth (per capita GDP growth averaged 0.6% between 1994 and 1999 and 2.6% between 2000 and 200712) and less aggressive tax increases. Even though the tax incidence benchmark was originally set as an excise tax incidence benchmark, the National Treasury has interpreted the benchmark as 50% total tax incidence (representing an excise tax incidence of 38% when VAT is excluded) (Van Walbeek, unpublished, 2005) This benchmark would have been reached in 2006, but in 2004 it was adjusted upwards to 52% total tax incidence for a three-year period and in 2007 excise taxes rose by their smallest amount since the introduction of the tax incidence benchmark.

Affordability and per capita consumption in South Africa. Source: CP Van Walbeek, unpublished, 2005, SARB12 and Actuarial Society of South Africa. Note: The RIP is defined as the percentage of per capita GDP required to purchase 100 packs of cigarettes. An increase in the RIP means that a greater proportion of income is required to purchase cigarettes and hence cigarettes have become less affordable. A decrease in the RIP means that a smaller proportion of income is required to purchase cigarettes and hence cigarettes have become more affordable. The normal convention of using the adult population of 15 years and older in calculating per capita consumption is followed. We use the Actuarial Society of South Africa population estimates since they also provide a population forecast which is used later on. The source only provides estimates from 1985 onwards.

Van Walbeek (unpublished, 2005) notes that the National Treasury claimed to have reached the total tax incidence target of 50% in 1997 although he indicates this to be ‘more illusory than real’. Confusion over whether the target has been met or not most likely results from a timing issue. National Treasury does not set excise taxes in a forward looking manner in that they do not forecast the impact of inflation and industry reaction when setting the excise tax for the year to come. However, prices rise as a consequence of inflation thereby eroding the excise tax increase. Furthermore, the industry may choose to adjust retail prices as a result of the change in excise. Historically, this has involved passing the entire tax onto consumers as well as raising the industry/base/net-of-tax price resulting in a lower than expected total tax incidence (Van Walbeek, unpublished, 2005) The net result is that the actual/current total tax incidence is 51%, lower than the target of 52%.

South Africa—simulating alternatives

From a tobacco control tax policy perspective one of two options is required in South Africa in order to see continuing declines in tobacco consumption. Either the tax incidence benchmark needs to be increased or an alternative strategy needs to be proposed. The proposal of a higher tax incidence benchmark will only be a temporary solution since at some point it will be achieved after which the same stagnation will likely be seen again. The particular concern is the lag between reaching of the target and implementation of an alternative strategy. The last increase in the tax incidence benchmark in South Africa occurred in 2004 when the total tax incidence benchmark was raised to 52% for a three-year period—since 2007 there has been no change in the benchmark. During this period the decline in consumption has ended. An alternative benchmark based on affordability will see a permanent and dynamic solution that results in an affordability target being met on an ongoing basis and the affordability target adjusting dynamically to ensure declining consumption. The principle of an affordability benchmark is that excise taxes should be increased on an annual basis to always ensure that affordability is at least being maintained or reduced.

The important consideration is what will occur in the future if the tax incidence benchmark is maintained at 52% total tax incidence. This paper simulates the effect on per capita consumption of maintaining the tax incidence benchmark (‘a’ in figure 5) as well as four alternative proposals. First, maintaining affordability (‘b’ in figure 5), by increasing excise in such a way as to maintain the level of affordability which existed in 2008. Second, reducing affordability (‘c’ in figure 5), by promoting a continuously rising RIP (ie, making cigarettes continuously less affordable) by increasing excise by 2 percentage points more each year relative to maintaining affordability. Third, increasing the total tax incidence benchmark (‘d’ in figure 5), by 1% annually to examine the impact of regularly adjusting the benchmark upwards. Fourth, benchmarking real excise taxes and prices directly (‘e’ in figure 5), following the UK example in the late 1990s whereby excise taxes increased by at least 5% in real terms annually.13 14 For the purposes of the simulation a price elasticity of demand of −0.6 and an income elasticity of demand of 1.0 is assumed, both of which are consistent with the estimations of Van Walbeek (unpublished, 2005) and other estimates in South Africa.15–17 Furthermore an annual rate of per capita GDP growth of 2.5% is assumed which is consistent with the recent past (per capita GDP growth averaged 2.6% between 2000 and 200712). It is also assumed that the industry passes on the entire tax to the consumer. Historically, the industry has passed on the entire tax to the consumer as well as increasing the industry/base/net-of-tax price (Van Walbeek, unpublished, 2005).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

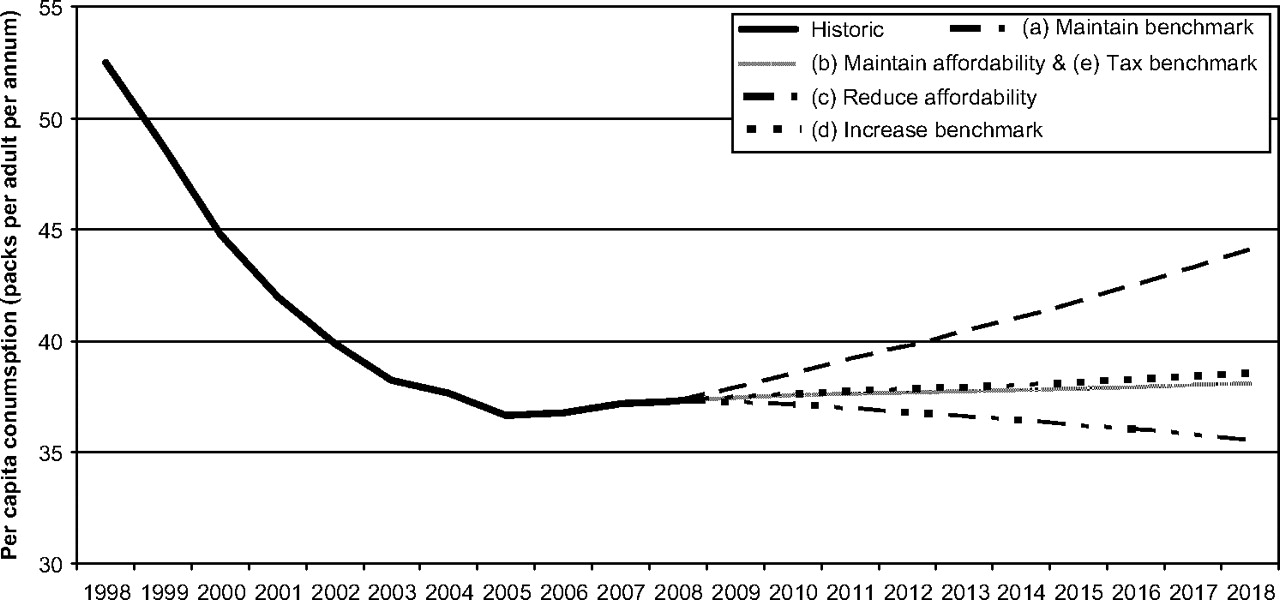

Simulated per capita consumption in South Africa. Note: Even though the two series (b) Maintain affordability and (e) Real excise tax benchmark use different assumptions the outcomes are the same and thus they share the same line on the graph.

Figure 5 shows the simulated impact of the five scenarios on per capita cigarette consumption. The simulation is run on an annual basis and displays estimates until 2018 as well as the historical series since 1998.

From a tobacco control perspective this is a concerning picture. Maintaining the current tax incidence benchmark (‘a’ in figure 5) will result in per capita consumption rising aggressively by 18% in total between 2008 and 2018, driven by the rising affordability of cigarettes. The application of an affordability benchmark to maintain affordability at its current level (‘b’ in figure 5) will require excise taxes to increase at 5% per annum and result in per capita consumption rising by a significantly smaller 2% in total. (Superficially one would expect constant affordability to result in constant consumption but this is not the case. For every 1% increase in income experienced there is a 1% increase in consumption. However, in order to maintain affordability prices must also increase by 1%, which results in a 0.6% decline in consumption. The net effect is a rise in consumption even though affordability remains unchanged.) Using the affordability benchmark to reduce affordability (the application of a 2% premium to the annual growth in excise taxes) results in a decline in per capita consumption of 4.7% over the 10 years while the RIP will increase from 3.6% to 4.2% (‘c’ in figure 5). The third option, of increasing the tax incidence benchmark by 1% per year to 61% in 2018 (note that the benchmark is applied in a backward looking manner and total tax incidence was 51% in 2008) results in an outcome similar to maintaining affordability and per capita consumption is expected to rise by 3% over the 10 years (‘d’ in figure 5). The application of the tax/price benchmark increasing excise taxes 5% annually provides the same results as maintenance of affordability (this is simply coincidental) (‘e’ in figure 5).

Maintenance of the current tax incidence benchmark in South Africa will clearly result in a large public health failure while maintaining affordability or even increasing the tax incidence benchmark annually will also result in increases in per capita consumption. The application of a rule directly applied to excise also results in increasing consumption. This strategy would only reduce consumption if the annual increase in excise were higher or economic growth slower. The disadvantage relative to the affordability benchmark is that the affordability rule allows the annual increase in excise to vary according to the economic conditions experienced in the country. The only scenario under which per capita consumption will fall over the next 10 years is one where affordability will decline.

Conclusion

The benefits of an affordability benchmark are clear and easy to understand in this context. The affordability benchmark is promoted not because tax incidence benchmarking does not work but because the affordability benchmark provides a clear and easy to understand dynamic benchmark. This is particularly important in many LMICs which are experiencing rapid economic growth where following a tax incidence benchmark may result in cigarettes becoming rapidly more affordable. The case of South Africa has been used to argue in favour of an affordability benchmark where maintenance of the current tax incidence benchmark will result in a public health failure. An affordability benchmark will not only consolidate the public health gains made since 1994 but will provide a lasting legacy of declining tobacco consumption. The affordability benchmark is not proposed to replace a tax incidence benchmark in all cases but in those cases where tax incidence benchmarking is struggling in the face of rapidly growing incomes.

There are however some caveats to this approach. The current global economic crisis exposes a weakness of the concept since declining incomes would require cuts in excise taxes in order to maintain affordability. This is clearly unsustainable and not in the interests of public health or fiscal policy. Cigarette excise taxes are an especially important source of revenue in times when other tax sources are declining. Evidence of this are the large number of US states that have raised excise taxes during the current economic crisis. Thus I propose that the rule seeks only to raise excise taxes and to not allow them to decline in nominal or real terms even if incomes are falling. Second, this rule is designed specifically for countries which are experiencing rapid economic growth where growth in incomes are making cigarettes more affordable. This rule may not be relevant or appropriate in countries which have mature markets and in which income growth does not undermine tobacco control efforts.

What this paper adds

This paper introduces an alternative tax policy rule using affordability rather than tax incidence. It shows how a tax incidence benchmark rule is not an optimal policy tool in rapidly growing low-income and middle-income countries and how an affordability benchmark may be more effective in reducing tobacco consumption.

Acknowledgments

I thank Corné van Walbeek, Hana Ross, Anna Gilmore, Frank Chaloupka, Emmanuel Guindon and an anonymous reviewer for their useful comments and suggestions and Erik Nesson for research assistance. All other errors and omissions remain mine exclusively.

Footnotes

Competing interests None.

Provenance and peer review Not commissioned; externally peer reviewed.