Article Text

Abstract

Objectives: Several states, including California, have implemented large cigarette excise tax increases, which may encourage smokers to purchase their cigarettes in other lower taxed states, or from other lower or non-taxed sources. Such tax evasion thwarts tobacco control objectives and may cost the state substantial tax revenues. Thus, this study investigates the extent of tax evasion in the 6–12 months after the implementation of California's $0.50/pack excise tax increase.

Design and setting: Retrospective data analysis from the 1999 California Tobacco Surveys (CTS), a random digit dialled telephone survey of California households.

Main outcome measures: Sources of cigarettes, average daily cigarette consumption, and reported price paid.

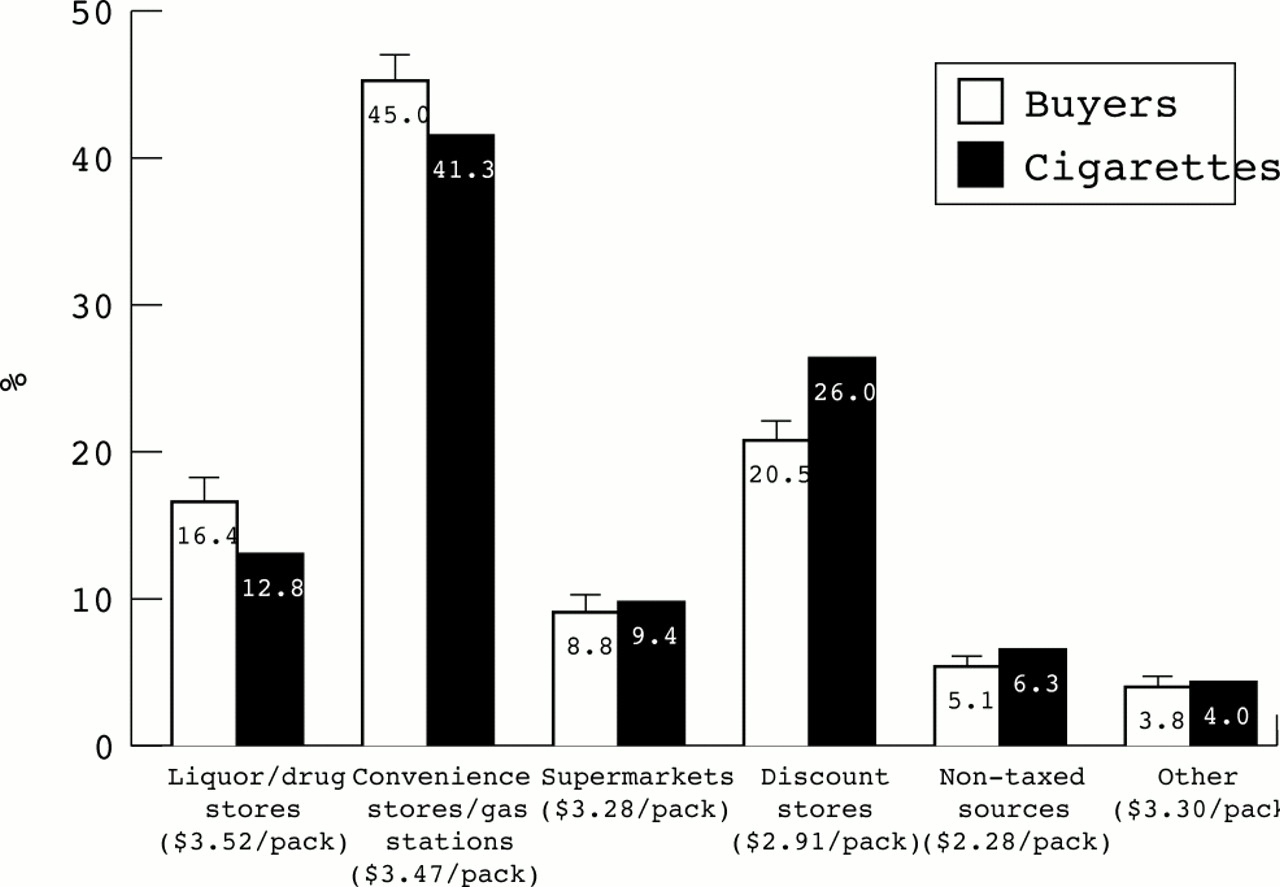

Results: Very few (5.1 (0.7)% (±95% confidence limits)) of California smokers avoided the excise tax by usually purchasing cigarettes from non- or lower taxed sources, such as out-of-state outlets, military commissaries, or the internet. The vast majority of smokers purchased their cigarettes from the most convenient and expensive sources: convenience stores/gas (petrol) stations (45.0 (1.9)%), liquor/drug stores (16.4 (1.6)%), and supermarkets (8.8 (1.2)%).

Conclusions: Despite the potential savings, tax evasion by individual smokers does not appear to pose a serious threat to California's excise tax revenues or its tobacco control objectives.

- California cigarette excise tax

- tax revenues

- price sensitivity

Statistics from Altmetric.com

By the 1990s, economists had largely established that higher cigarette prices were associated with lower smoking prevalence and reduced consumption.1, 2 Since then, cigarette excise taxes have been widely proposed as a tobacco control policy tool, to encourage quitting, reduce consumption among remaining smokers, and decrease smoking initiation. This policy tool, however, included a caveat: raising cigarette prices above those from out-of-state sources creates an incentive for individual smokers to purchase cigarettes from lower or non-taxed sources—that is, individual tax avoidance3, 4—and also introduces the potential for increased crime as a result of organised smuggling. If a cigarette excise tax increase stimulates casual and organised smuggling activities, states may lose tax revenues without necessarily reducing smoking.

In 1999, California became a high profile testing ground for these potentially conflicting effects when it implemented a $0.50/pack voter approved cigarette tax increase, which was associated with a corresponding retail price increase that made the price of cigarettes significantly higher in California than in the bordering states. At about the same time as the excise tax increase in California, all states experienced an additional industry driven retail cigarette price increase of approximately $0.70/pack in 1999 because of the Master Settlement Agreement. Together the excise tax and the industry driven price increase resulted in a retail price increase of $1.20/pack in California.

Six months after the 1999 tax and price increases, per capita taxed cigarette consumption had decreased by 30% in California.5 While reduced smoking likely explained a large portion of this decline, tax evasion could have accounted for another substantial part. California smokers had a number of options to avoid the state tax, including internet cigarette vendors, military commissaries, and neighbouring states, as well as the Mexican state of Baja California, all of which offer lower priced, often tax-free American cigarettes. In November 1999, the retail price of cigarettes in California averaged $3.51/pack, compared to the following prices in neighbouring states: $3.17 in Arizona, $3.03 in Nevada, and $3.24 in Oregon.6 In Mexico, the average price for a carton of US manufactured cigarettes was approximately $137; military commissaries charge neither the federal ($0.32/pack) nor the state excise tax, resulting in a potential savings of $1.19/pack, compared to other California retailers. Although cigarettes purchased from Indian reservations are exempt from federal excise taxes, in California the state excise tax is paid before distribution to the reservations. Thus, the lower prices typically observed at casinos located on Indian reservations in California do not represent lost state excise tax revenues.

It is difficult to estimate the magnitude of organised smuggling. The State Board of Equalization estimated that, together, organised and casual smuggling (more accurately, individual tax avoidance purchases) may have cost the state as much as $80 million in unpaid excise tax revenues in 1999,8 and California was cited on the US Senate floor as an example of the high cost of cigarette tax evasion.9 The Board of Equalization's estimates were based on techniques originally used by the Advisory Commissions on Intergovernmental Relations, which concluded in 1975 that governments suffered significant revenue losses because of organised cigarette smuggling and individual tax avoidance, but subsequently updated their results in 1985, finding that smuggling was not an important source of lost tax revenues. Others have also produced conflicting results. For example, Sung and colleagues found significant short distance smuggling (individual tax avoidance)10 between 1967 and 1990 in 11 western states, but Fleenor11 concluded that despite evidence of significant organised cigarette smuggling and individual tax avoidance, the individual tax avoidance purchases from military bases and Indian reservations were insignificant. Most recently, Yurekli and Zhang estimated that interstate cigarette sales (individual tax avoidance) were responsible for $400 million in revenue losses in the USA,12 which would translate to approximately $30 million for California, given that California represents roughly 7.5% of cigarette sales in the USA. Each of the previous studies, however, based their findings on assumptions about population distributions and the fraction of total cigarettes sold that may have been transported across state lines, legally or illegally. In this paper, we investigate the extent of tax evasion from individual tax avoidance by analysing where Californians bought their cigarettes after the tax increase, and how much they usually paid per pack.

METHODS

Data sources

The methods for the California Tobacco Surveys (CTS) are reported elsewhere.13 Briefly, random digit dialled telephone interviews were used to obtain smoking data from the California population. A five minute screener survey enumerated all adults in the household, and an extended 25 minute interview was conducted on a subsample where the probability of selection was greater for those who had smoked within the past five years, compared with never smokers or longtime quitters. The 1999 CTS was conducted between August and December 1999, and included 5215 adult smokers, who were the subjects of this paper.

Definition of smokers

Smokers were identified as those who responded “some days” or “every day” to the question “Do you smoke cigarettes every day, some days or not at all?”, and who had smoked at least 100 cigarettes in their lifetime. The majority of smokers were male, non-Hispanic white, high school graduates, who smoked daily. Table 1 provides detailed demographic characteristics of the smokers who responded to the 1999 CTS. All smokers were asked how many cigarettes they smoked per day on average.

Demographic characteristics of smokers in 1999 California Tobacco Survey (n=5215)

Sources and prices of cigarettes

All smokers were asked where they usually buy their cigarettes: in state, out of state, or over the internet. In addition, smokers who reported they usually purchased cigarettes in California were asked to specify the type of store where they usually buy cigarettes: convenience stores/gas (petrol) stations; supermarkets; liquor/drug stores (pharmacies); tobacco discount stores; other discount stores, such as Wal-Mart; Indian reservations; military commissaries; or other types of stores, specified by the respondent. Smokers were also asked:

-

what brand they usually smoke

-

whether they usually buy cigarettes by the pack or carton

-

how much they usually pay for a pack or carton.

Using this information, we could calculate the average price paid per pack for those who purchased by the pack or by the carton, as well as variations in prices by brand and by outlet type.

Statistics

Estimates were calculated so that they were representative of the California population at the time of the survey. Base weights were computed, which took into account a respondent's probability of being interviewed, and then ratio adjusted using the population totals for demographic subgroups based on education, race/ethnicity, and sex. All analyses were performed with the WesVarPC statistical package,14 which takes into account the sample design and uses a jackknife procedure for variance estimation and tests of significance.15

RESULTS

Source of cigarettes

Figure 1 shows that more than seven months after the implementation of the new excise tax, only 5.1 (0.7)% (±95% confidence limits) of California smokers usually avoided the state excise tax by usually purchasing cigarettes over the internet (0.3 (0.2)%), at military commissaries (1.7 (0.5)%), or out of state (3.1 (0.5)%). In fact, over 70% of smokers usually purchased their cigarettes from the most convenient and most expensive retail sources: convenience stores/gas stations, or liquor/drug stores, and supermarkets. Only one in five smokers usually purchased their cigarettes at discount stores, such as a tobacco discount store or a general discount store, like Wal-Mart.

Comparison of cigarette purchase sites and buyers after implementation of the new California excise tax (1999 California Tobacco Survey, n = 5215 smokers).

Combining the information on usual source of cigarettes with smokers' self reported average daily consumption, we calculated the proportion of total reported cigarette consumption accounted for by each source. The solid bars in fig 1 show that the volume of cigarette purchases is nearly proportional to the percentage of buyers at each type of outlet. Discount stores account for a slightly higher percentage of the total volume of cigarettes sold than cigarette buyers (26.0% v 20.5%); liquor/drug stores account for proportionally fewer cigarettes sold than buyers (12.8% v 16.4%).

Analysing the self reported average price/pack by retail source confirmed that the most convenient sources are also the most expensive, that discount retailers were 18% cheaper, and that non-taxed sources were the cheapest, at 33% less. These price differences largely reflect differences in patterns of buying by the pack versus by the carton, and by brand choice. Overall, 71.3 (1.6)% of smokers reported they usually bought their cigarettes by the pack, as opposed to by the carton. Table 2 shows that nearly 90% of smokers who reported they usually bought their cigarettes from convenience stores or liquor/drug stores also reported that they usually bought by the pack. Just over 60% of smokers who usually bought their cigarettes at grocery stores usually bought by the pack. Of those who usually purchased cigarettes at discount stores, less than one third usually bought by the pack; and of those who usually purchased from sources that did not charge the California excise tax, approximately one in four usually bought by the pack.

Purchase patterns: carton versus pack, and brand choice, by cigarette outlet type

Some of the variation in prices across outlet types may also be caused by differences in brand choices (premium v generic). Despite the differences in brand choice across store types, Marlboro was clearly the dominant brand, regardless of where it was purchased. Table 2 shows that close to 80% of smokers who usually buy their cigarettes at convenience stores/gas stations or liquor/drug stores smoke premium brands. This percentage decreased slightly to 70–75% for smokers who usually bought their cigarettes at supermarkets, discount stores, or lower or non-taxed sources.

Excise tax revenues

Using our estimates of the number of packs purchased per month from both California excise taxed and non-excise taxed sources, we calculated that after the implementation of the $0.50/pack excise tax increase in 1999, the state's annual revenue from taxed sales of cigarettes was approximately $761 million. Of that total revenue, the 1999 excise tax increase accounted for approximately $468 million. Our calculations suggest that the state may have lost as much as $51 million of excise tax revenues from cigarette purchases from sources that did not charge the California excise tax.

DISCUSSION

Our data showed that despite the potential savings, tax evasion by individual smokers in California did not appear to pose a serious threat to the state's excise tax revenues or its tobacco control objectives in 1999. Indeed, the majority of California smokers did not appear to place a high priority on minimising the price they pay for cigarettes. A very small fraction (5.1%) of California smokers reported that they usually bought their cigarettes from internet sources, military commissaries, or out-of-state vendors, which did not charge the state excise tax.

Our calculations were based on smokers' reports of where they usually bought their cigarettes. The data did not allow us to determine the extent to which smokers who usually purchased from sources that charged the state excise tax also occasionally purchased cigarettes from other sources, some of which may have been non-taxed sources. Conversely, however, smokers who reported they usually purchased cigarettes from non-state taxed sources may have occasionally purchased cigarettes from sources that charged the state excise tax. Nonetheless, a conservative interpretation of our results would suggest that our estimates may be lower than the actual proportion of cigarettes bought from non-state taxed sources.

We were surprised at the very low volume of internet cigarette purchases since a carton of Marlboro's on the internet averages $25 or $2.50/pack, compared to over $3.50–$4.00/pack in California retail outlets. It is possible that smokers underreported internet cigarette purchases because of concerns about the legality of this form of tax avoidance. While internet vendors are required to report out-of-state sales, only 5% of online cigarette vendors from outside California do so.16 Perhaps more importantly, most internet cigarette vendors require a minimum purchase of 2–5 cartons in order to avoid significant shipping and handling fees, and smokers must wait several days for their order to be delivered. Less than a third of California smokers reported that they usually buy cigarettes by the carton from any source; therefore, meeting this large minimum purchase requirement would represent a substantial change in consumer behaviour. Furthermore, given that the average daily consumption for California smokers has decreased notably in recent years,17 our findings suggest that it is unlikely that the market for internet cigarettes will grow significantly in California. However, it is conceivable that in places with high concentrations of heavy smokers, who routinely buy cigarettes by the carton, these governments may lose substantial revenue because of non-state taxed internet cigarette sales.

Not all sources of cigarettes are subject to the state excise tax. Military personnel and their families can purchase cigarettes from the commissary, and smokers may purchase cigarettes for their own use when they are travelling out of state. While many smokers may do this on rare occasions, when it is convenient, few appear to do so routinely.

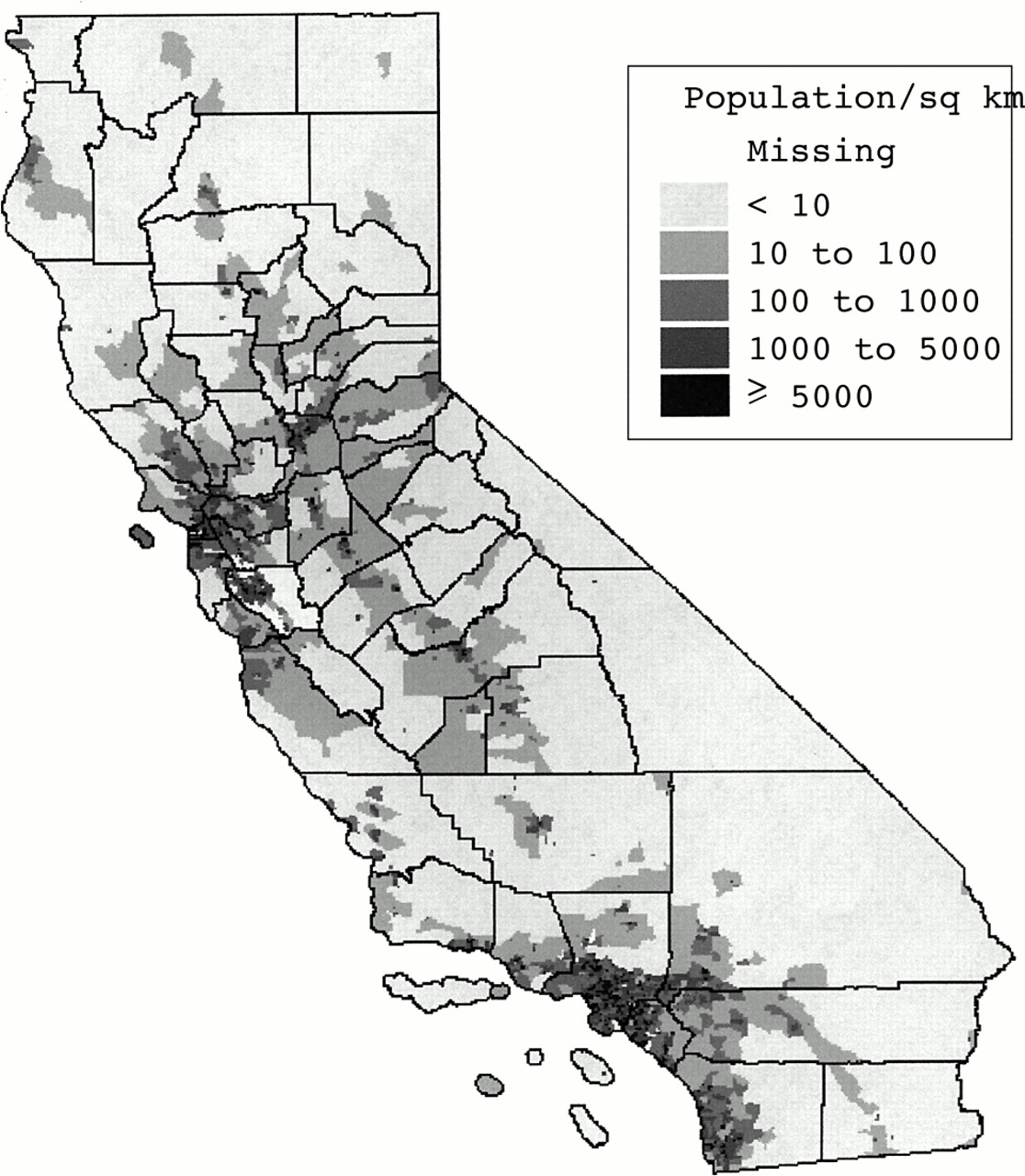

Cigarette excise taxes and retail prices were lower in each of California's bordering states in 1999, including the state of Baja California, Mexico. Figure 2 shows that the most densely populated areas in the state are along the coast. Thus, if they wanted to avoid the state's cigarette excise tax, the vast majority of Californians would need to drive several hours, fly, or leave the country to avoid the state's cigarette excise tax. Although the Mexican border is very close to a large population centre in San Diego, crossing the border nearly always involves a wait of well over 30 minutes and a customs check on return to the USA—a significant deterrent to routinely shopping in Mexico. Therefore, while there may have been some under reporting of non-taxed cigarette purchases because of fears about their legality, it is unlikely that this under reporting was sufficiently prevalent to change our results substantially. These results may not be generalisable to other environments, where the state border is more easily and frequently traversed. For example, in Boston, Massachusetts, which is very close to the New Hampshire border, smokers can easily cross the state line to buy lower taxed cigarettes.

{kind=link}

{kind=link}

Population density in California.

Using the CTS data on self reported cigarette consumption, we estimated that after the $0.50/pack cigarette excise tax increase in 1999, the state received approximately $761 million in annual revenues from taxed cigarette sales. Our data suggest that this figure was approximately $51 million lower than might have been achieved if all the cigarettes purchased by California smokers had been subject to the California excise tax. This $51 million amounted to less than 7% of the total excise tax revenues in 1999. While a potential loss of $51 million in state revenues is not inconsequential, it is far outweighed by the gain of approximately $438 million in revenues (a 57% increase) that resulted from the additional $0.50/pack excise tax increase. Although some of these non-state taxed cigarettes represent individuals' efforts to evade the additional state tax, many such purchases were from sources such as military commissaries, which were available long before the excise tax. Additionally, economic theory suggests that without less expensive alternatives available, some smokers would reduce their level of consumption or quit altogether.1, 3, 18 In this case, the smaller total increase in cigarette tax revenues could not be attributed to tax evasion, but rather to reduced smoking.

The actual 1999 excise tax revenues reported by the California Board of Equalization were $1.12 billion. This represented a 72% increase from 1998 revenues.5 The state's projected $80 million loss from evasion amounted to 7.1% of the actual collected revenues, which is comparable to our estimate and is outweighed by the large increase in tax revenues. Our estimates of collected and potentially evaded excise tax revenues were approximately one third lower than the state's estimates. This discrepancy is consistent with the literature comparing self reported consumption with sales data, and may result from smokers' preference to report consumption in units of half a pack of cigarettes, systematically rounding down.2

Our data do not include questions about coupon use or the frequency with which smokers take advantage of pricing promotions, such as buy-one-get-one-free offers. While retail prices for cigarettes increased by a factor of over 50% between 1998 and 1999, the tobacco industry also increased its overall expenditures on advertising and promotions by over 20%, to $8.24 billion in the USA as a whole; we estimate that this translates to at least $824 million in California alone. At the same time, its budget for coupons and retail value added programmes increased by over 40%, to $3.09 billion in the USA, or approximately $300 million in California.19 Thus, many of the smokers who reported in the 1999 CTS that they usually purchased their cigarettes from convenience stores/gas stations or liquor/drug stores may have frequently taken advantage of value added programmes, and therefore paid less per pack on average than they reported.

What this paper adds

Little is known about tax evasion behaviour of smokers in states with relatively high cigarette excise taxes. Some estimates of revenue lost to smuggling are available from state boards of equalisation, but these data cannot separate out organised smuggling from tax evasion behaviour by individual smokers. Findings from the 1999 California Tobacco Survey indicate that despite the high average cost of cigarettes in California ($3.51/pack), few smokers (5%) usually buy their cigarettes from non- or lower taxed sources such as neighbouring states/countries, Indian reservations, military commissaries or over the internet. Instead, most (70%) buy from convenient (and expensive) sources: convenience stores/gas stations, liquor/drug stores, and supermarkets. Thus, tax evasion by individual smokers does not seriously threaten revenue nor undermine the potential impact of price on consumption.

We were unable to determine whether the purchase patterns we report for 1999 represent a shift in behaviour because the comparable data did not exist from earlier CTS surveys. We were also unable to comment on organised smuggling in California. Regardless, in 1999, in the setting of a large cigarette excise tax, our data suggest that casual tax evasion was not prevalent among California smokers. Thus, the excise tax increase achieved the goal of raising revenues without compromising the public health objective of also reducing smoking.

Acknowledgments

Preparation of this article was supported by the Tobacco Related Disease Research Program grant 9RT-0036 from the University of California. Data for the California Tobacco Surveys were collected under Contract 98-15657 from the California Department of Health Services, Tobacco Control Section, Sacramento, California. We would also like to thank John Cromartie of the US Department of Agriculture, for assistance with our map of California.

Footnotes

-

↵* This work was completed while Sherry Emery was at the Cancer Prevention and Control Program, University of California, San Diego. She is currently at the Health Research and Policy Centers, University of Illinois at Chicago.