Article Text

Abstract

Background In Colombia, smoking is the second leading modifiable risk factor for premature mortality. In December 2016, Colombia passed a major tax increase on tobacco products in an effort to decrease smoking and improve population health. While tobacco taxes are known to be highly effective in reducing the prevalence of smoking, they are often criticised as being regressive in consumption. This analysis attempts to assess the distributional impact (across socioeconomic groups) of the new tax on selected health and financial outcomes.

Methods This study builds on extended cost-effectiveness analysis methods to study the new tobacco tax in Colombia, and estimates, over a time period of 20 years and across income quintiles of the current urban population (80% of the country population), the years of life gained with smoking cessation and the increased tax revenues, all associated with a 70% relative price increase of the pack of cigarettes. Where possible, we use parameters that vary by income quintile, including price elasticity of demand for cigarettes (average of −0.44 estimated from household survey data).

Findings Over 20 years, the tax increase would lead to an estimated 191 000 years of life gained among Colombia’s current urban population, with the largest gains among the bottom two income quintiles. The additional annual tax revenues raised would amount to about 2%–4% of Colombia’s annual government health expenditure, with the poorest quintiles bearing the smallest tax burden increase.

Conclusions The tobacco tax increase passed by Colombia has substantial implications for the country’s population health and financial well-being, with large benefits likely to accrue to the two poorest quintiles of the population.

- smoking caused disease

- taxation

- socioeconomic status

- disparities

- economics

Statistics from Altmetric.com

Introduction

Like many South American countries, Colombia faces a high burden of non-communicable diseases (NCDs). WHO estimates that in Colombia NCDs accounted for 73% of total deaths in 2015.1 As a middle-income country with a multipayer health system that provides universal healthcare, Colombia is struggling with the financial implications tied to increasing demand for health services, driven in part by the management of NCDs.2

In 2013, the Colombian government committed to substantially decrease the burden of NCDs, of which a key stated target was to reduce the prevalence of smoking to 10% from 13% among those aged 18–69 years between 2012 and 2021.3 Colombia also committed to the Sustainable Development Goals (SDGs), which, under SDG3 calls for ‘healthy lives for all people’ by 2030.4 Part of this goal is the reduction of premature mortality by one-third, which smoking cessation and prevention will help Colombia to achieve. With around 3 million urban smokers, about 12% of the urban population between the ages of 10 and 79 years, smoking is the second leading risk factor for mortality.5 6 Estimates from 2013 indicate that treating tobacco-related illnesses cost an estimated 4 230 000 million Colombian pesos (COP) annually, or almost US$2.1 billion, equivalent to about 0.6% of the country’s gross domestic product (GDP).7–10 As such, decreasing smoking prevalence in Colombia holds promise in decreasing NCDs and with it the financial burden of treating smoking-related diseases.3

In 2008, Colombia ratified WHO’s Framework Convention on Tobacco Control (FCTC), thereby making a legal commitment to implement strong tobacco control policies. Colombia has implemented several FCTC recommendations for reducing tobacco consumption, including national smoke-free areas and advertising and promotion bans.10

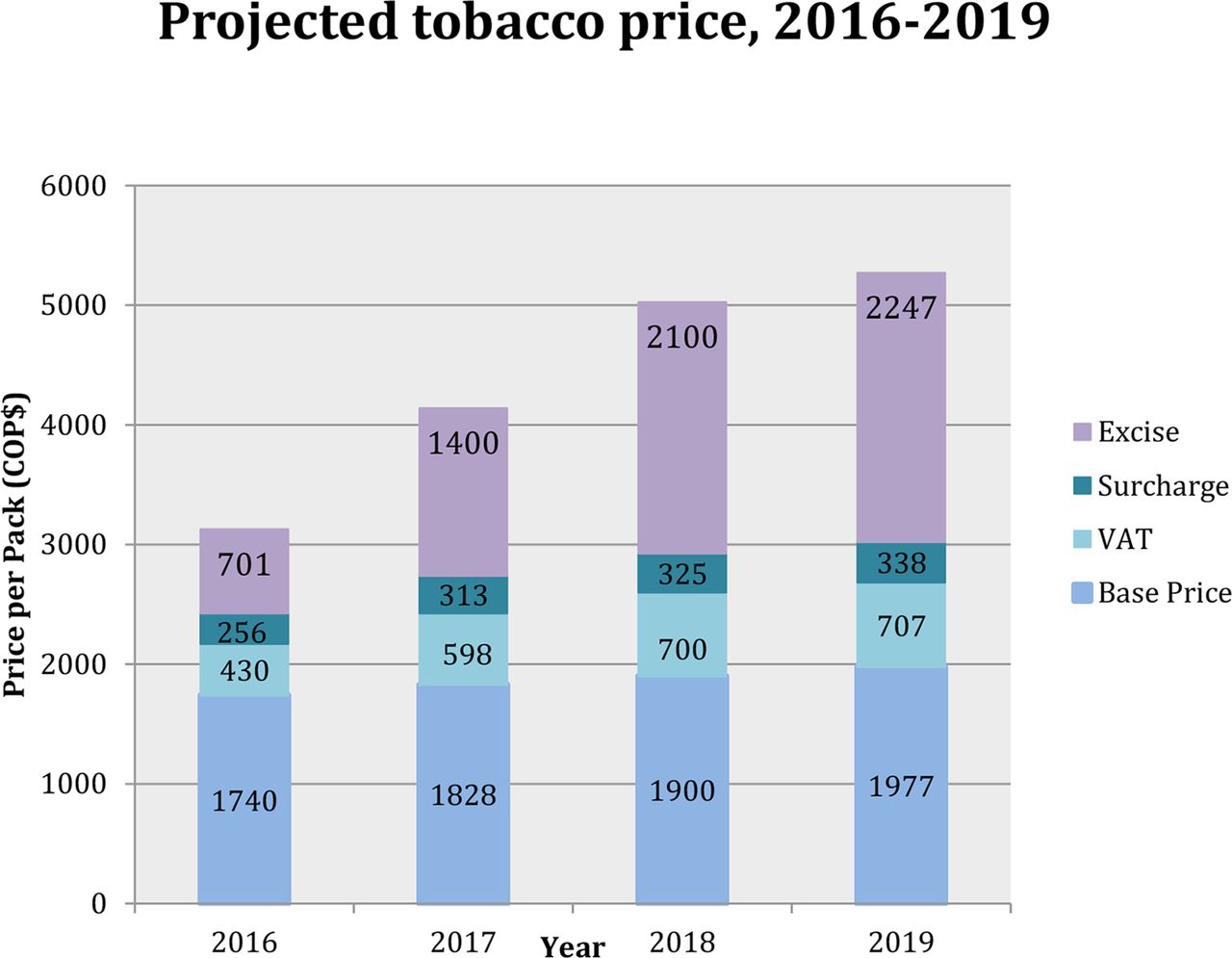

In December 2016, Colombia legislated an increase in both excise taxes and value-added taxes (VAT) of tobacco products in the context of a general tax reform.11 Indeed, WHO recommends that excise taxes should be at least 70% of the retail price of cigarettes to maximise the effect against smoking.12 13 Prior to the tobacco tax reform, Colombia fell short of this benchmark, as the former (pre-2017) tax on the most sold brand pack of cigarettes was <50% of the retail price, with excise taxes constituting only about 30% (22% specific, ie, defined amount per pack; 8% ad valorem, ie, defined percentage per pack value) of the retail price14 15 (figure 1). From 2017 onwards, the reform doubles the specific excise tax to COP$1400 (2017), triples it to COP$2100 (2018), and subsequently (2019 and beyond) increases the price of cigarettes by the country’s annual rate of inflation plus four percentage points.11 15 The legislation also increases the VAT from 16% to 19% of the base price of a cigarette pack in 2017. The new taxes (post-2019) will constitute about 62% of the retail price with specific excise taxes making up roughly 43% of the retail price, still falling short of WHO’s 70% benchmark.

{kind=link}

Projected tobacco price, 2016–2019, following Colombia’s tax policy. Prior to the tobacco tax reform (2016), specific excise taxes (COP$701) would represent about 22% of the retail price of cigarettes; while they would represent 34% (COP$1400), 42% (COP$2100) and 43% (COP$2247) of the retail price in 2017, 2018 and 2019, respectively. Overall, the retail price will have risen by 69% over 2016–2019. Source: Llorente.15 COP, Colombian pesos; VAT, value-added taxes.

Nevertheless, tripling the specific excise tax15 is expected to substantially decrease tobacco consumption in Colombia. Most evidence supports the use of large price increases to decrease tobacco consumption16–19: it discourages non-smokers (eg, the young) from beginning smoking; it pushes smokers to quit or to decrease their smoking; and it discourages former smokers from resuming smoking. Additionally, the young appear to be more price responsive than the old, which has the potential for large future gains in terms of decreasing tobacco use and associated mortality and morbidity.19–21 The poor also seem to be more price responsive than the rich,19 20 22 23 which is important since much of the controversy around raising tobacco taxes is consumption regressivity. Despite differing tax structures for tobacco products, increasing specific excise taxes remains one of the most effective means of decreasing tobacco consumption.14 19 Uniform specific excise taxes equalise the price of all tobacco products by narrowing the price gaps between cheaper and more expensive cigarettes, and therefore can prevent tobacco users from potential product substitution and switching to consuming cheaper cigarette brands.18 19 In this paper, we examine the potential impact of Colombia’s new tobacco tax increase, and draw from extended cost-effectiveness analysis (ECEA) methods24 25 to model the impact of the tax on selected health and financial outcomes across socioeconomic groups in Colombia.

Methods

Modelling approach

We build on ECEA methods24 25 to examine the potential distributional consequences of increasing tobacco taxes on Colombia’s health and finances. ECEA was designed to study the impact of policy along three dimensions: health benefits, out-of-pocket (OOP) expenditure ‘crowded out’ for households and individuals with the associated financial risk protection provided (eg, cases of catastrophic health expenditure averted) and distributional consequences (eg, across socioeconomic groups, geographical settings). ECEA has been previously applied to examine the distributional impact of tobacco tax policy in China,26 27 Lebanon22 and Armenia,23 while the distributional incidence of tobacco taxes has also been previously studied in Chile.28 Here, we draw from a previously published ECEA tobacco tax model26 27 to study impact on: the years of life gained (YLG) associated with smoking cessation; the change in tobacco tax burden and the change in cigarette expenditure.

Our study uses varying inputs across urban income quintiles and age groups (table 1) to estimate the hypothetical tax policy impact among the current urban population (77% of the country population as of 20169). The population is divided into seven age groups (<15, 15–24, 25–49, 50–64, 65–69, 70–74 and 75–79 years) further disaggregated by income quintile. As data on smoking prevalence by age group and income quintile were only available for Colombia’s urban population,6 we restricted our analysis to the urban population under age 80 years, implying that our results capture a lower bound of the potential policy impact since it excludes the rural population. Therefore, we use age-specific smoking prevalence data and further distribute it across income quintiles using quintile-specific smoking prevalence data to obtain the number of current smokers per age group and income quintile. To account for the fact that households in lower-income quintiles have more children, we further adjust the population size of ‘future smokers’ (age <15 years) by modifying the distribution of those future smokers per quintile. Furthermore, consistent with findings from the literature, the model assumes that, for all smokers (young and old), the participation elasticity is half the total price elasticity, implying that increased prices affect the smoking participation by half and the other half affects the consumption of cigarettes among those who do not quit.19 Younger (aged <20 years) smokers are also assumed to be twice as responsive as older smokers (aged >35 years), consistent with reviews,19 with a linear increase in price elasticity modifier (from 1 to 2) from age 35 to age 20 years (over age groups 20–24, 25–29 and 30–34 years).

Inputs and corresponding sources used in the analysis of the distributional impact of increased tobacco taxes among Colombia’s urban population on years of life gained, tax revenues and cigarette expenditure

We examine hypothetical impact over a time period of 20 years in three ways. First, we estimate the number of YLG among those quitting smoking as a result of increased prices. We assume no health gains for those who do not quit but reduce smoking consumption. The YLGs depend on age at quitting: there is an inverse relationship between YLG and age at smoking cessation: quitting at age 30, 40, 50 or 60 years, leads to gains of about 10, 9, 6 or 3 years of life, respectively.18 29 Using the product of the participation elasticity, the change in price, and such estimated age-specific YLG among quitters, we obtain the YLG due to increased prices for those who would have died prematurely over the next 20 years (see online supplementary appendix, section 1, for further detail).

Supplemental material

Second, we calculate tax revenues before and after the tax increase and the change in revenues borne by each income quintile. We use estimated baseline cigarette consumption by quintile (from 5.7 cigarettes per day among the poorest to 10.1 among the richest) and the average tax per cigarette pack (COP$1389) to calculate revenues before tax increase. We then estimate post-tax increase revenues by income quintile and compare them with the pre-tax increase revenues to examine the change in revenues.

Third, to generate estimates of expenditure on cigarettes by quintile we use the estimated number of smokers by income quintile after the tax increase and the projected price per pack of cigarettes. We then compare these new estimates under the post-tax scenario to the pre-tax scenario to quantify the change in consumption and hence expenditure on cigarettes by quintile.

While the tax is designed to increase the average price of cigarettes three times, we only report aggregate findings, and assume no change in household income and socioeconomic status over time.

Model inputs

We use parameters that vary by income quintile where possible in order to capture the distributional impact of the tax (table 1). Average price and taxes per cigarette pack were sourced from a recently published report15 (figure 1). The report used the median cigarette price obtained from the Departamento Administrativo Nacional de Estadística to calculate the total taxes per pack. Then taxes were added to the base price as outlined in the December 2016 law to obtain the predicted prices over 2017–2019.

We assume the tax is completely passed onto the consumer .15 In a sensitivity analysis, we also modelled the outcomes using the price of a premium pack of cigarettes (Marlboro Red) with a tax inclusive retail price in 2016 of COP$3772.14

One of the most important inputs is the price elasticity of demand for cigarettes. We used the Encuesta Nacional de Calidad de Vida (ENCV) household surveys30 combined with the Encuesta Anual Manufacturera (EAM) reporting cigarette sales31 for the years 2003, 2010, 2011 and 2014 (we had four price values), to derive an estimated average price elasticity of −0.44 for Colombia (further detail is provided in the online supplementary appendix, section 2.1), consistent with previous average estimates of about −0.40.19 As price elasticity estimates per income quintile were not available for Colombia, we identified 11 other studies from Latin American countries with price elasticity estimates ranging from −0.85 to −0.22 (online supplementary appendix, section 2.2). Subsequently, we distributed the variation in these 11 estimates (IQR 0.42) across our average price elasticity of −0.44 to derive a price elasticity per income quintile (table 2; online supplementary appendix, section 2.2) assuming the poor have a greater price elasticity than the rich, consistent with previous studies.19 20 22 23 We also proceeded to sensitivity analyses using two alternative flat price elasticities across income quintiles to better understand the distributional impact of the tax: −0.40 as indicated by WHO19; and −0.78 as recently estimated by Maldonado et al for Colombia.32

Assumed price elasticity of demand for cigarettes by income quintile and age group

Sensitivity analyses

We pursued five univariate sensitivity analyses for the legislated tax increase: (i) where the price elasticity was set flat to −0.40 across income quintiles; (ii) where the price elasticity was set flat to −0.78 across income quintiles; (iii) where the youth elasticity modifier was set to 1 instead of 2 (the young would be as price elastic as adults); (iv) where the mean price of a pack of cigarettes was set to COP$3772 and (v) where the baseline cigarette consumption was set flat to an average eight cigarettes per day across income quintiles. The first three sensitivity analyses attempt to address the uncertainty underlying estimates of price elasticity, a key input in tax policy impact. The last two sensitivity analyses aim to address the lack of evidence in the distribution in the price and consumption of the different cigarette brands.

Furthermore, since Colombia’s legislated specific excise tax increases remain below WHO recommendations, we provide estimates for two additional specific excise tax increase scenarios that would hypothetically take place in 2020. The first scenario raises specific excise taxes to make up 50% of the retail price of cigarettes, representing a 18% increase compared with the 2019 retail price; the second increases them to 70% of the retail price, corresponding to a 97% increase compared with the 2019 retail price (see online supplementary appendix, section 3).

Results

For the current urban population, with a cumulative 69% price increase in an average pack of cigarettes spread out over three consecutive tax increases (figure 1), we would expect about 191 000 YLG over 20 years (table 3). About 50% of these YLG would come from the two poorest income quintiles while the smallest proportion (28%) would come from the two richest income quintiles.

Summary findings for the distributional health and financial consequences of increased tobacco taxes among Colombia’s current urban population, across income quintiles, over 20 years

Furthermore, the net annual gains in tax revenues compared with pre-increase (2016) would be of roughly COP$700 000 million (year 1 after tax increases), COP$790 000 million (year 10 after increases) and COP$1 260 000 million (year 20 after increases) (table 3). Since the richest income quintile is assumed to be more inelastic with respect to price, it would have the highest number of people who continue smoking so it would shoulder the highest burden of the projected additional tax revenues. We see that the two bottom income quintiles would see about 30% of the additional tax burden, while the top two quintiles would bear about 50% of this burden. The average annual tax revenue gains under the three consecutive tax increases would amount to about 2%–4% of Colombia’s government health expenditure and about 0.1% of its 2016 GDP.

Lastly, we estimate that households in all income quintiles would spend more on cigarettes than before. The net increase in cigarette expenditure compared with pre-increase (2016) would be of roughly COP$660 000 million (year 1 after tax increases), COP$720 000 million (year 10 after increases) and COP$1 050 000 million (year 20 after increases). We would see the greatest net annual increase among the richest quintile (about 31% of the total increase) and the smallest increase among the poorest quintile (about 9%).

In addition, when we hold the price elasticity of demand for cigarettes constant, this would change both absolute and distributional impact of the tax increase (table 4). Under both scenarios, we find the greatest number of YLG from the third income quintile (22%). With fewer people quitting smoking under the lower elasticity scenario, we find a greater increase in tax revenues under the lower elasticity scenario (COP$710 000 million) than under the higher elasticity scenario (COP$490 000 million). Since the price elasticity is set flat under both scenarios, the distributional impact would change: the richest income quintile would have the largest (25%) and the poorest income quintile the smallest (13%) increase in tax revenues and household expenditure on tobacco after the tax increases under both cases. When we simulated a case where the young would not be more price elastic than adults (multiplier of one), we see that the health benefits would remain similar over 20 years (190 000 YLGs), as the cessation or initiation prevention benefits among those aged<35 years today (future YLGs) would not have yet occurred. Likewise, we would find only slight changes in terms of tax revenues and cigarette expenditure.

Summary findings for the sensitivity analyses of the distributional health and financial consequences of increased tobacco taxes among Colombia’s current urban population, across income quintiles, over 20 years

Furthermore, when we used as an alternative the mean price per cigarette pack of the premium brand of cigarettes (retail price of COP$3772 in 2016), the relative price increase would change, leading to fewer YLGs over 20 years than under the base-case (about 178 000). Meanwhile, the tax revenues would be greater than in the base-case (COP$830 000 million in year 1 after increases), with large revenues from the top income quintile (COP$236 000 million or 28% of total revenues). Lastly, when we hold cigarette consumption equal across all income quintiles, this would greatly change the distributional impact, with more of the change in tax revenues borne by the poorest (15%) than under the base-case (11%).

In the future, if Colombia were to increase specific excise taxes to 50% of the retail price after 2019, 245 000 YLG would occur over 20 years (table 5). This represents an additional 54 000 YLG above the base-case. If the specific excise tax rises to 70% of the price, we would expect 479 000 YLG, which is an additional 288 000 YLG above the base-case. The distribution of YLG by income quintile would however remain similar. Additional tax revenues under the 50% scenario would be of about COP$930 000 million. A 70% specific excise tax would lead to an estimated additional revenue increase of COP$1 060 000 million, which while in line with the base-case changes the distribution of the tax burden by income quintile. Indeed, the richest quintile would now carry 46% of the tax burden while the poorest quintile would only carry 1% of the increased tax burden. Estimates for household expenditure on cigarettes would follow a similar pattern: households would spend an estimated annual COP$ 610 000 million expenditure on cigarettes

Summary findings of the distributional health and financial consequences of future increases in tobacco specific excise taxes among Colombia’s current urban population, across income quintiles, over 20 years

Discussion

In 2016 through legislation Colombia decided on substantially increasing its tobacco taxes, tripling the specific excise tax over 2 years and increasing the VAT by three percentage points. These measures are expected to result in a roughly 70% relative price increase over 3 years (figure 1). This large and swift increase in the price of cigarettes would have substantial impacts on reducing the number of smokers, decreasing the premature deaths attributable to tobacco and its associated years of life lost, and increasing government revenues. Our analysis of the potential impact of the tax policy demonstrates considerable benefits to poor segments of the Colombian population.

We find the greatest health benefits and the smallest net change in the tax burden among the bottom income quintile, with a gradient showing the number of YLG decreasing and the net change in tax burden increasing as we switch from the bottom to the top income quintile. These findings point to the potentially pro-poor dimensions of the legislated increases in tobacco taxes in Colombia. In addition, our two simulated specific excise tax increase scenarios provide evidence supporting the large benefits of maintaining high levels of taxes into the future. In particular, when the specific excise tax is set to 70% of the retail price of cigarettes, representing a further substantial relative price increase (97% compared with 2019 prices), as expected the health gains would become far greater.

Nevertheless, our analysis presents a number of limitations, primarily related to the model inputs. First, we derived price elasticity of demand for cigarettes by income quintile based on household survey data and a review of the literature from Latin American countries. In particular, our average price elasticity of demand was estimated using only four price data points, which might introduce the possibility of confounding by variations in tobacco control policy over time. However, our derived price elasticity estimates are consistent with previously published evidence,19 including studies reporting on price elasticity across income quintiles. For example, a Korean study found a price elasticity among the poor of −0.81 vs −0.32 among the rich33; a study in Moldova found a price elasticity of −0.51 among the poor vs −0.26 among the rich34; an ECEA of tobacco tax in Lebanon estimated a price elasticity of −0.32 among the poor vs −0.22 among the rich22 and Postolovska et al estimated a price elasticity of −0.74 among the poor vs −0.28 among the rich in the Kyrgyz Republic.23 We also ran two sensitivity analyses with alternative values for price elasticity (−0.40 and −0.78)19 32 to understand the impact this parameter would have on our findings. Second, we relied on household surveys to estimate the prevalence of smoking and the number of cigarettes smoked per day. However, we used average price of cigarettes to determine cigarette consumption from weekly household cigarette expenditure using the ENCV30 and EAM,31 even though the price per pack of cigarettes could range depending on various factors. Therefore, we pursued two sensitivity analyses in varying price per pack and cigarette consumption. Third, we did not have the prevalence of smokers in rural areas, which prevented us from producing estimates for Colombia’s whole population (both urban and rural), implying that our estimates would represent a lower bound of the potential tax policy impact. Fourth, we used a static model focusing on the current population and did not examine the evolution of health and financial benefits far into the future (beyond 20 years). Indeed, the health benefits and YLG will likely be greater as younger age groups quit smoking and/or are prevented from smoking initiation, thus yielding even greater health benefits in the longer 30–50 years time horizon. Fifth, we assumed fixed household income trajectories in the future, meaning we did not allow for social mobility across income quintiles over time. Sixth, our model did not take cigarette smuggling into account (except under the −0.78 price elasticity scenario as reported by Maldonado et al 32), which might increase in response to tax increases and bring cheaper cigarettes onto the market, undercutting the health benefits of the tax.35 However, studies show that even with smuggling, tobacco tax increases still largely reduce smoking prevalence.36 Finally, our findings should be interpreted with caution as they are largely dependent on the utilisation of many different data sources with varying underlying assumptions, due to data limitations. Our focus on urban smokers overlooks benefits accruing to the rural population. While less is known about smokers and cigarette markets in rural areas, our model likely underestimates the national benefits of tax increases.

It is critical that Colombia keeps raising taxes as incomes grow and cigarettes become relatively cheaper. Evidence from France with raising cigarette prices through tax increases indicates that once prices stabilise, cigarette sales no longer decrease and smoking rates remain unchanged.17 Our analysis shows that the 70% increase in the average price per cigarette pack would put Colombia closer to meeting its commitments of decreasing smoking rates and the prevalence of NCDs. The tax increase will also help Colombia deal with the increasing financial strain that the growing burden of NCDs places on the health system, while addressing health and economic inequalities overall.

What this paper adds

What is already known on this subject

WHO estimates that tobacco kills about 7 million people per year. Tobacco taxes are among the most effective policy tools to discourage smoking.

A few extended cost-effectiveness analysis (ECEA) studies modelled the distributional impact of increased tobacco taxes in low-income and middle-income countries on populations’ health and finances.

What important gaps in knowledge exist on this topic

We built on ECEA to estimate the distributional benefits, years of life gained with smoking cessation and additional tax revenues raised, associated with increased tobacco taxes among Colombia’s urban population following the country’s tax policy legislation passed in December 2016.

What this study adds

Our study generates evidence on the potential household health and financial consequences of increased tobacco taxes in Colombia and illustrates how tobacco control policies can be pro-poor.

References

Footnotes

Contributors EKJ conceived the analyses, collected the data, conducted the research, and wrote the first draft of the manuscript. SV designed and supervised the study. MVU collected survey data and conducted preliminary analyses. All authors contributed to drafting and critical revision of the manuscript and have approved the final article.

Funding Funding for this study was provided by the World Bank and the World Bank’s Global Tobacco Program, co-financed by the Bill & Melinda Gates Foundation and the Bloomberg Foundation. An earlier version of this paper was published as a World Bank working paper (James, Saxena, Franco Restrepo, et al. World Bank, Washington, DC 2017: https://openknowledge.worldbank.org/handle/10986/28598. License: CC BY 3.0 IGO) and was presented during seminars at the Ministry of Health and Social Protection and the Ministry of Finance and Public Credit, Colombia, and at the Harvard T H Chan School of Public Health, where we received valuable comments from seminar participants as well as from Andres Escobar, Alan Fuchs, Alejandro Gaviria, Patricio Marquez, Margaret McConnell, Francisco Meneses, Ece Özçelik, Michael Reich and Juanita Carolina Bodmer Rico. The findings, interpretations, and conclusions in this article are entirely those of the authors. Responsibility for the views and opinions expressed rests solely with the authors; they are not endorsed by any member institution of the World Bank Group, its Executive Directors, or the countries they represent.

Competing interests None declared.

Patient consent Not required.

Provenance and peer review Not commissioned; externally peer reviewed.