Article Text

Abstract

Objective To analyse trends in cigarette brand preference among Mexican smokers during the implementation period of key WHO’s Framework Convention on Tobacco Control recommendations.

Methods Data came from two nationally representative, comparable surveys, namely the Global Adult Tobacco Survey 2009 and 2015 and the National Survey on Addictions 2011 and 2016. Logistic models were used to estimate the adjusted prevalence of each brand purchased, as well as individual correlates of purchasing the single brand with a large growth over the study period. Multiple linear regressions were also employed to analyse cigarette prices across brands.

Results Six brand families accounted for about 90% of the cigarette market, with Marlboro clearly dominating all brands at 54%–61%. Only the share of Pall Mall brand, however, registered a rapid increase over the period—from 1% in 2009 to 14% in 2016. Women and younger smokers (15–24 years) were more likely to prefer Pall Mall over other brands. While the typical price segmentation between international (premium) brands and national (discount) brands was observed, the price of Pall Mall is within the range of the latter. Importantly, most varieties of this brand include flavour capsule varieties (FCVs).

Conclusions This study suggests that the strong campaign of brand migration, the pricing strategy and the aggressive introduction of FCVs expanded Pall Mall in the Mexican cigarette market. Therefore, better control policies of cigarette contents and taxes that reduce price differentials across brands should be encouraged to promote public health.

- low-/middle-income country

- packaging and labelling

- price

- priority/special populations

Data availability statement

Data are available in a public, open access repository. Data of the Global Adult Tobacco Survey Mexico 2009 and 2015 are available from CDCs GTSS Data website and data of the National Survey on Adiccions 2011 and 2016 are available from https://encuestas.insp.mx/ena/

Statistics from Altmetric.com

Introduction

For more than a decade, the WHO’s Framework Convention on Tobacco Control (FCTC) has spurred the rapid adoption of tobacco control policies around the world.1 In this context, the fastest growing segment of the combustible cigarette market has been for cigarettes with flavour capsules in the filter.2 Consumers can flavour the cigarette smoke by crushing the capsule, which come in flavours ranging from variations of mint (eg, wild mint, strawberry mint) to fruits (eg, orange peel, grape, mango, cucumber) and beverages (eg, green tea, whiskey, mojito).3 Cigarettes may contain up to three capsules and packs may have up to five flavours in total. Despite their relatively recent introduction, flavour capsule varieties (FCVs) comprise more than 10% of the combustible market in some European countries (UK, Hungary, Ireland, Poland) and South Korea, although FCVs comprise the highest market share in a number of Latin American countries (ie, top five countries in 2017: Argentina=17%; Mexico=21.5%; Guatemala=32.1%; Peru=34.2%; Chile=36.1%).4 5 To increase understanding of the evolution of the combustible cigarette market in the FCTC era, this study assessed trends, correlates and prices of cigarette brands among current smokers in Mexico from 2009 to 2016, which covers the period when key FCTC-recommended policies were implemented and when FCVs came into the market and became increasingly popular.

Since Mexico ratified the FCTC in 2004,6 regulations have banned tobacco product advertising through most traditional media (except adult-oriented magazines and points of sale),7 mandated prominent, pictorial health warnings on cigarette packaging8 and successively increased cigarette taxes.9 Early tax increases appear to have accelerated the polarisation of the Mexican market, which has been underway since the mid-1990s.10 As Philip Morris International and British American Tobacco (BAT) came to dominate the market, the premium segment was occupied by international brands (eg, Marlboro, Benson & Hedges, Camel) while the national brands (eg, Delicados, Faros) were located in the low-cost (discount) segment.11

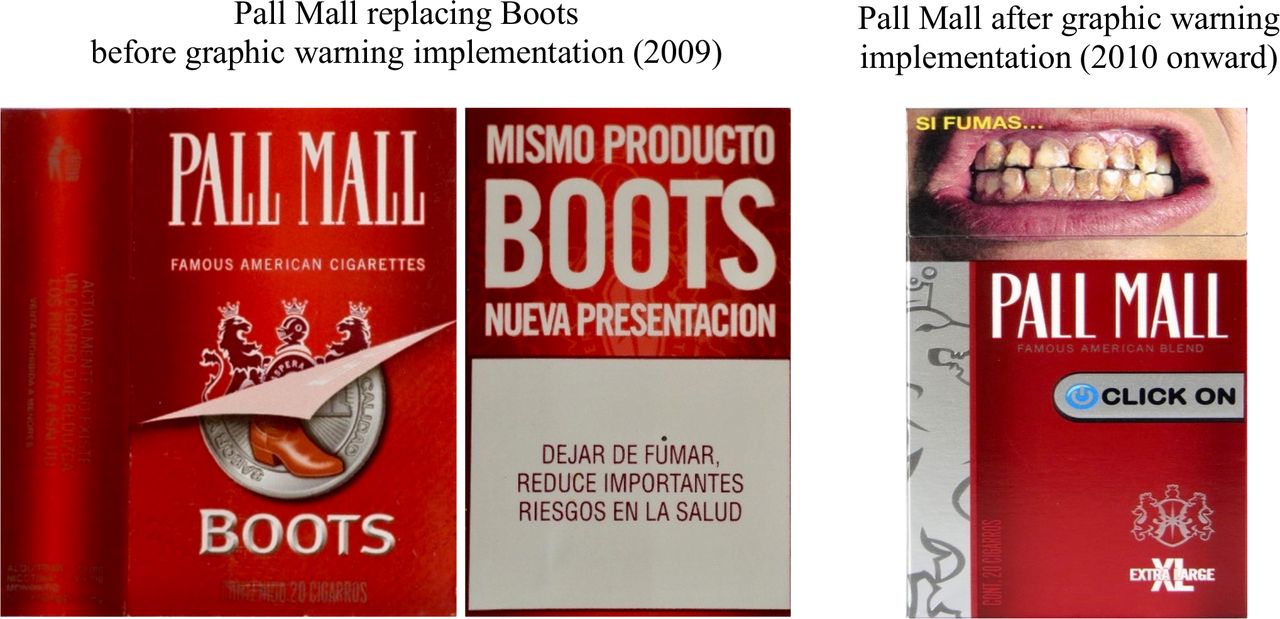

After the last specific tax increase in 2011, the price gap between the premium and discount segments was reduced.12 Therefore, the tobacco industry (TI) focused on the migration of consumers from brands with poor performance (mid-price) to Global Drive Brands.13 In 2009, the Mexican brand Boots migrated to Pall Mall (the leading GBD of BAT) adding international prestige and highlighting its value-for-money features while maintaining its low cost (figure 1). Shortly after Marlboro introduced FCVs in 2011, Camel and Pall Mall did, too, with Pall Mall introducing an increasingly broad range of FCVs flavours, including in longer cigarettes (100 mm), with very few non-FCVs staying on the market.14 FCVs smokers, particularly those who smoked Pall Mall, perceived their brand as more stylish, smoother and less harmful compared with smokers who preferred non-FCVs.15 Aside from industry reports,4 5 examinations of the early impact of the 2011 tax,11 12 and studies of convenience samples,15 no research has evaluated further the evolution of brand preferences in Mexico.

International brand Pall Mall replaced national brand Boots. Mexico 2009. The image on the left shows that in 2009 cigarette packs of Boots could have a double cover to portray both the colours and symbols of Boots brand and the new features of Pall Mall brand. These packs included the legend ‘same product, new presentation’.

This study uses nationally representative data from 2009 to 2016, which covers the period of Mexico’s most extensive tobacco control policy implementation, in order to (1) assess trends in preferences for the most popular cigarette brands; (2) compare prices for the most popular brands and (3) evaluate the characteristics of smokers who prefer the brand with the greatest growth during this period.

Methods

Data source

Data for the current study came from two comparable and nationally representative surveys conducted in Mexico from March 2009 to October 2016: the 2009 and 2015 Global Adult Tobacco Survey (GATS) and the 2011 and 2016 administrations of the National Survey on Addictions (NSA). Both surveys used a multi-stage sampling scheme to select households for in-person surveys (see methodological details in technical reports16–19), with response rates over 70% (82.5% in 2009, 73.3% in 2011, 82.7% in 2015 and 73.64% in 2016). The analytic sample for this study consisted of the 12 692 current smokers (2009 n=1619, 2011 n=2306, 2015 n=1632, 2016 n=7135) aged 15–65 who reported the last cigarette brand they purchased (missing covariate data=2.5% of all current smokers, 15–65 years old).

Measurements

Smoking behaviour

Current smokers were identified using the responses to the questions: Do you currently smoke tobacco on a daily basis, less than daily, or not at all? (GATS 2009 and 2015, NSA 2016) and How often are you currently smoking? Daily, less than daily or do not smoke currently (NSA 2011). Smokers were classified into three groups: non-daily smokers; light daily smokers of up to five cigarettes per day (CPD) and heavy daily smokers of more than 5 CPD.

Cigarette brand of the last purchase

Current smokers were asked to report the brand they last purchased. Interviewers selected the brand from a pre-defined list, and if the brand was not on the list, the interviewer wrote down the brand name provided. Of the top 10 for any survey year, six brands accounted for approximately 90% of the brand preferences over the entire study period. Our analysis is limited to these brands, with another category for ‘others’, as the surveys do not gather more specific information on brand variants within brand families.

Type of cigarette purchase

Current smokers were asked: The last time you bought cigarettes for yourself, how many cigarettes did you buy? As more than 99% of the sample indicated having purchased packs or single cigarettes (GATS 2009 99.6% and 2015 99.7%, NSA 2011 99.4% and 2016 99.3%), analyses that included the type of cigarette purchase excluded those who purchased cartons.

Self-reported cigarette price

Price per cigarette at last purchase was calculated using the response to the question on last purchase and querying how much they paid for this purchase. The average price per single cigarette was obtained by dividing the reported cost by the number of cigarettes purchased (eg, 20 cigarettes/pack). Prices were adjusted for inflation using the general price index from the Bank of Mexico; all prices are reported in Mexican pesos (MX$) of January 2017 (exchange rate: 21.38 MX$ per US dollar (US$)).

Covariates

Standard sociodemographic variables were queried, such as sex (female vs male), age group (15–24, 25–44 and 45–65 years), residence (rural vs urban) and highest educational attainment (primary or less, middle school, high school and university or more).

Analysis

All analyses were adjusted for sampling weights and the survey design to make the estimates representative of the population. Descriptive statistics (prevalence) were used to compare sociodemographic characteristics and smoking behaviour across surveys and to characterise trends in purchasing cigarette brands. Logistic models20 were used to estimate the prevalence of purchasing each brand (eg, Marlboro vs each of the remaining brands) stratified according to the type of purchase (single cigarettes vs packs) and adjusted by sex, age group, residence, highest educational attainment, smoking pattern and price per cigarette. The year of the survey was included as a categorical variable to assess the change over time. After identifying the brand with the greatest growth over the study period, we estimated a logistic regression model regressing the purchase of this brand versus all other brands on the same individual characteristics described above and stratified by the type of last cigarette purchase (single cigarettes vs packs). Finally, a multiple linear regression model was estimated to analyse cigarette prices per brand, stratified by the type of last cigarette purchase, using the year of survey and cigarette brand as main regressors. Prices were estimated using 2011 as a point of reference. The statistical software Stata V.15 was used for all the analyses.

Results

Sample characteristics

Sample sociodemographic characteristics were relatively consistent over time: 7 out of 10 smokers were men, the majority lived in urban communities (>84%), and almost half (46%–48%) were between 25 and 44 years old (table 1). However, current smokers surveyed in 2016 had higher educational attainment than those in 2009 (high school or more: 30% in 2009 to 37% in 2016, p<0.05). The proportion of heavy daily smokers (>5 CPD) decreased over time (25% in 2009 to 18% in 2016, p<0.001) and this change was accompanied by the subsequent increase in the proportion of non-daily smokers (52% in 2009 to 61% in 2016, p<0.001). Among current smokers, the proportion who reported buying single cigarettes (vs packs) increased from 2009 to 2016 (40% to 48%, p<0.001).

Demographic characteristics and smoking behaviour of current smokers 15–65 years, Mexico 2009–2016

Trends in cigarette brand purchase

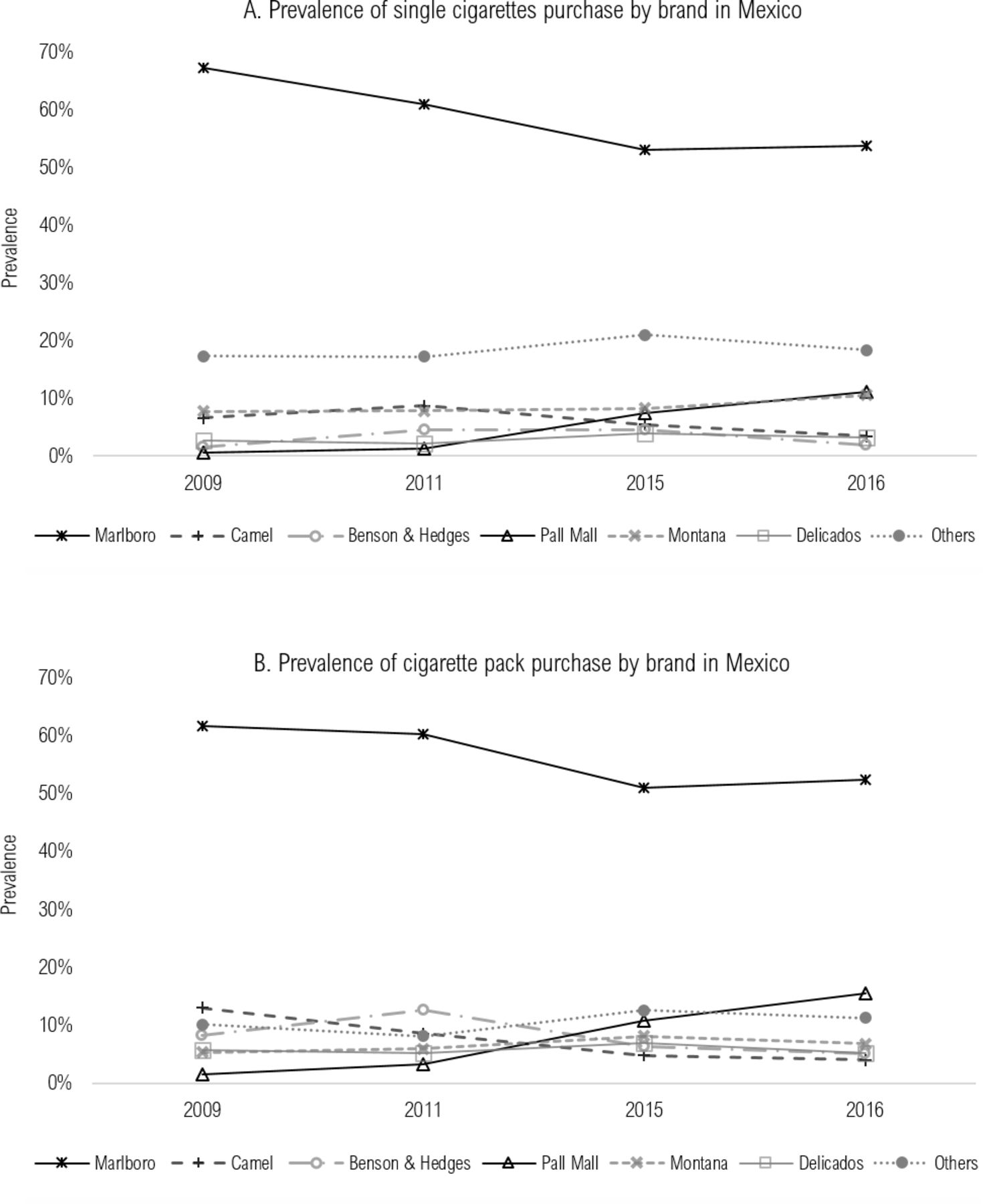

Six brand families accounted for 88%–91% of the study sample. The most often purchase brand was Marlboro, dominating all brands at 54%–61% over the market. The most important changes were observed in Camel and Pall Mall brands. The proportion of Camel smokers had a significant decrease from 9% in 2009 to 4% in 2016 (p<0.001). In contrast, the prevalence of Pall Mall purchase increased rapidly from 1% in 2009 to 14% in 2016 (p<0.001). The rest of the brands (Montana, Benson & Hedges, Delicados and Others) had minor fluctuations over the study period (table 1).

Figure 2 shows the prevalence for each major brand purchased, stratified by type of purchase and adjusted by year, sociodemographic characteristics (sex, age group, education), smoking pattern and cigarette price. Marlboro was the most purchased cigarette brand every year. However, its adjusted prevalence trended downward, independent of the type of purchase (single cigarette: 67.4% in 2009, 53.8% in 2016, p<0.001; pack 61.7% in 2009, 52.5% in 2016, p<0.05). The same pattern was observed for Camel (single cigarette: 6.6% in 2009 to 3.5% in 2016, p<0.05; pack: 13% in 2009 to 4% in 2016, p<0.001). By contrast, purchases of Pall Mall increased for both types of purchase, although the greatest growth was observed among those who bought packs between 2011 and 2016 (3.2% to 15.5%, p<0.001).

{kind=link}

{kind=link}

Adjusted prevalence of cigarette purchase by brand and type of purchase. Mexico 2009–2016. Logistic regression models were adjusted independently for each brand (eg Marlboro vs each of the remaining brands) and stratified by type of purchase: (A) single versus (B) pack. Adjustment variables were the survey year (2009 as the reference), sex, age group, residence, education, smoking pattern and price per cigarette (log-transformed).

Finally, stable patterns were found for Delicados (p>0.05 for both single cigarette and pack purchases; 2.6%–3.3% (n=162) and 5.8%–5.2% (n=387), respectively) and Montana (p>0.05 for both single cigarette and pack purchases; 7.8%–10.6% (n=368) and 5.4%–6.9% (n=436), respectively), while the prevalence of purchasing Benson & Hedges exhibited a U-shaped pattern (single cigarette: 1.6% in 2009, 4.6% in 2011/2015 and 1.8% in 2016 (n=195); pack: 8.2% in 2009, 12.6% in 2011, 6.4% in 2015 and 5.2% in 2016 (n=367)).

Cigarette prices across brands

The analysis of prices was conducted separately for cigarettes bought as a single and cigarettes bought in packs, as the former are generally much more expensive (eg, MX$4.37 vs MX$2.03 in 2016, respectively) and present greater variance (eg, SE=3.96 vs SE=0.81 in 2016, respectively). While cigarette taxes were only increased in 2009–2011, self-reported average prices increased over the whole study period: from MX$2.59 (95% CI=2.45 to 2.72) in 2009 to MX$2.83 (95% CI=2.75 to 2.91) in 2011, MX$3.13 (95% CI=2.99 to 3.28) in 2015 and MX$3.24 (95% CI=3.17 to 3.31) in 2016.

In general, the price segmentation described in previous studies was observed.12 International brands such as Marlboro, Benson & Hedges and Camel have similar average prices, independently of the type of purchase (eg, difference for Camel with respect to Marlboro=0.11 for packs (p=0.1) and 0.09 for singles (p=0.5); table 2). On the other hand, national brands such as Delicados and Montana are cheaper, although the difference is clearer for cigarettes bought in packs (eg, difference for Delicados with respect to Marlboro=−0.43 for packs, p<0.001, n=387; table 2). Interestingly, the price of Pall Mall is within the range of the latter, which is again clearer for cigarettes bought in packs (difference for Pall Mall with respect to Marlboro=−0.34 for packs, p<0.001, n=814; table 2). We also tested brand-year interactions (not shown), but unlike previous studies12 no statistical differences in average prices by specific brand over time were found.

Multivariate lineal regression model for adjusted cigarette price at last purchase

Correlates of Pall Mall purchase

Bivariate logistic regression models indicate that those who purchased Pall Mall singles or packs were more likely to be female, younger (15–24 years), have middle educational attainment and have a non-daily smoking pattern of consumption (table 3). In adjusted logistic regression models, the likelihood of Pall Mall purchase remained higher for women independent of the type of purchase (ORsingle cigarettes=2.21, 95% CI 1.60 to 3.05; ORpack=1.99, 95% CI 1.53 to 2.60). Among those who bought single cigarettes, the likelihood of Pall Mall purchase was negatively associated with age (OR25–44 vs 15–24=0.46, 95% CI 0.33 to 0.63, OR45–65 vs 15–24=0.31, 95% CI 0.19 to 0.51) and with heavy daily smoking pattern (ORdaily>5 CPD vs non-daily=0.47, 95% CI 0.24 to 0.90). Interactions between sex and age (not shown) were not statistically significant. Among those who bought their cigarettes by pack, the likelihood of Pall Mall purchase was positively associated with education (ORhigh school vs primary or less=1.59, 95% CI 1.03 to 2.45).

Demographic characteristics and smoking behaviour of Pall Mall smokers 15–65 years. Mexico 2009–2016

Discussion

This study found that cigarette brand preferences in Mexico have shifted over the last years with a sharp increase in preferences for purchasing Pall Mall, and a corresponding decrease in purchasing brands like Camel and the dominant brand in Mexico, Marlboro. The adjusted prevalence of Pall Mall in 2016 was 475% higher (p<0.001) compared with 2011 and 1100% compared with 2009 (p<0.001). These results are consistent with the 2016 BAT annual report of the volume growth of Pall Mall in markets of Europe (Romania, the Netherlands and Poland), Asia-Pacific (Pakistan and Philippines) and the Americas (Canada, Mexico and Venezuela).21 In the USA, Sharma et al analysed trends in the market share of the leading cigarette brands between 2002 and 2013 and observed a 400% growth in the Pall Mall brand after a major recession and the increase in the federal excise tax of 2009.22 In a subsequent analysis, this group found that Pall Mall smokers shared characteristics of premium cigarette brands smokers: young age (26–34 years), higher income and lower cigarette dependence.23

The increase in preference for Pall Mall among Mexican smokers is likely explained by two factors. First, the strong campaign to migrate the national Boots brand to a low-cost international Pall Mall brand, presented as a new value-for-money brand like in Denmark, the Netherlands and Pakistan.13 21 Consistent with the US experience, the lower price and attractive pack design were associated with a rapid increase in market share.22 Second, Pall Mall aggressively introduced FCVs in 2011–2012, accelerating the rapid growth in market share.15 In 2013, a tobacco pack surveillance study found that 16 out of 20 varieties of Pall Mall were FCVs while other brands had fewer variants (eg Marlboro 2 of 19, Camel 5 of 26).14 Consistent with prior research on FCVs preferences among Mexican smokers,15 we found that women and younger smokers were more likely to prefer Pall Mall over other brands. Although the current study is nationally representative, we were not able to analyse brand preferences among smokers under 15 years because one of the surveys (GATS) did not sample this age group. Future studies should monitor the potential effect of FCVs on cigarette consumption among adolescents, as the novel and fashionable appearance of these products may encourage them to experiment with smoking.24 Indeed, urban adolescents (11–16 years) surveyed in 2015 in three largest cities in Mexico reported higher interest in trying FCVs, compared with non-FCVs cigarettes, with at least some of this interest due to the attractiveness of FCVs packaging.25

This study also portrays the price segmentation of the Mexican cigarette market, with international brands (eg, Marlboro, Benson & Hedges) more expensive than national brands (Montana and Delicados). As mentioned before, the only notable exception is Pall Mall, an international brand that combines a relatively low price and premium traits. Previous studies based on the International Tobacco Control (ITC) Mexico Survey,12 a cohort of smokers conducted in six main cities in the country, showed that the 2011 specific tax increase raised the price of national brands relative to international brands. We also found that self-reported average prices increased importantly after the 2011 tax increase; however, we found no evidence of heterogeneous increases in prices across brands over the study period. This may be related to the lower precision of self-reported price information collected with national surveys such as GATS and NSA. In particular, the variance of self-reported prices from national surveys is much larger compared with ITC Mexico Survey data (eg, overall mean price=1.93 with SE=0.72 for cigarettes bought in packs according to NSA 2011 versus overall mean price=2.25 and SE=0.01 according to ITC Mexico Survey 2011; the difference in SE is much larger for singles). While this is a limitation of the data employed in this study and suggests that the price analyses should take advantage of different available data sources, our main results are consistent with these trends.

Another limitation of this study is that the surveys employed did not ask questions about the use of FCVs cigarettes. Therefore, we were not able to estimate specifically preferences for FCVs, which are increasingly found in all brand families, neither the correlates of use (age, gender, education, type of purchase). However, results from an online convenience survey conducted in 2018 in Mexico showed that 94% of Pall Mall smokers (18 years and over) prefer FCVs.26 These findings highlight the urgent need to adopt the guidelines for the implementation of Articles 9 and 10 of the FCTC27 to regulate, by prohibiting or restricting, those ingredients that may increase the palatability or reduce the harshness of tobacco products (eg, sweeteners, benzaldehyde, maltol, menthol and vanillin) which are present in these FCVs28 and contributes to promoting and sustaining tobacco use.

This study is the first in Latin America to find that the growth of Pall Mall is not exclusive to high-income countries. In fact, this seems to be the result of a global strategy of the TI to cover the value-per-money segment through the positioning of Pall Mall. There are some similarities to the USA case, namely advertising and marketing of Pall Mall as a premium brand with a relatively low price, but the main difference is that the USA Pall Mall brand does not include FCVs. Our results may generalise to other countries in the Latin American region, especially those where FCV cigarettes have reached a high market share (eg, Chile, Peru and Guatemala).5

What this paper adds

Previous studies for high-income countries (HICs), especially the USA, have found that the Pall Mall brand has significantly increased its market share in recent years, mainly due to the market strategy that has positioned it as a premium brand with a relatively low price. At the same time, a growing set of studies indicate that cigarette brands with flavour capsule varieties (FCVs) have gained the highest market share in several Latin American countries, including Mexico.

The analysis of trends and correlates of cigarette brand preferences during the implementation of WHO Framework Convention on Tobacco Control-recommended policies in Mexico is scarce. That period coincides with the expansion of FCVs market segment. Unlike the USA, most of Pall Mall variants have capsules in Mexico.

This study shows that the rise in Pall Mall brand is not exclusive to HICs. Pall Mall is the only brand that registered a rapid increase over the past decade in Mexico, very likely due to the pricing strategy and the aggressive introduction of FCVs. These findings may generalise to other countries in the Latin American region, especially those where FCVs cigarettes have a higher market share.

Data availability statement

Data are available in a public, open access repository. Data of the Global Adult Tobacco Survey Mexico 2009 and 2015 are available from CDCs GTSS Data website and data of the National Survey on Adiccions 2011 and 2016 are available from https://encuestas.insp.mx/ena/

Footnotes

Contributors LZ-A conceived the research. DSG-T conducted the statistical analyses and wrote the manuscript. BSdM-J assisted with price analyses and interpretation of the data, as well as in the drafting. LMR-S and JT assisted with data interpretation and critically revised the article. All authors approved the final version for publication.

Funding This manuscript was granted by the Mérida Initiative (project number SINLEC17CA2011) and the National Commission against Addictions (CONADIC) through the project "Strengthening the policy framework to reduce the gap with WHO FCTC in Mexico" supported with funding from Bloomberg Initiative to Reduce Tobacco Use (www.bloomberg.org).

Competing interests None declared.

Provenance and peer review Not commissioned; externally peer reviewed.